Pathogens are a global threat to the swine industry. They arise from bacterial, viral, fungal, and parasitic sources. Numerous and often prone to mutation, with a tendency to become immune to treatment efforts over time.

Production flows within the North American swine industry routinely face challenges from multiple pathogens, and a resultant annual cost to the North American swine industry estimated in the billion-dollar range; with PRRS estimated at $664 million alone (AASV 2011 Position Statement on PRRS elimination). This suggests the swine industry would benefit from animals that have a higher capacity to survive health challenges.

An animal’s ability to withstand a disease challenge can be defined in many ways. Resistance, Resilience, Tolerance, and Robustness are all relevant descriptors. Genetic selection for each concept is uniquely defined, distinctively implemented, and depending on the circumstances, it can be beneficial under differing situations. Genetic selection for disease resistance seems optimal, as an animal resistant to a disease would appear to have an advantage over an animal that is not able to control a disease challenge; however, targeting a specific pathogen requires a considerable amount of upfront investment. Adding to that, the earlier-mentioned fact that there are numerous pathogens presents a real challenge to become resistant to them all. Viruses also tend to mutate, which can lead to low-rewarding efforts should the targeted pathogen suddenly transform and become re-infective to the population.

Selection for disease tolerance instead of resistance recognizes that an animal can still perform under the burden of varying disease levels. However, selection for disease tolerance requires simultaneous measurements on both performance and the levels of infection. Another downside to genetic selection for resistance or tolerance is the challenge of acquiring continuous records of the pathogen burden. The burden levels will likely vary over time, yet are required for genetic selection in both instances (Doeschl-Wilson et al., 2012).

A final hurdle is that pathogen burdens do not exist within high-health nucleus herd environments that the pork industry demands. Therefore, an alternative approach is warranted.

The concept of disease resilience offers the aforementioned alternative. It is a combination of resistance and tolerance and is defined as the ability of an animal to maintain performance across environments when exposed to pathogen challenges (Albers et al., 1987). Disease resilience is unique in that selection in favor of does not require specific knowledge of any certain pathogen or level of challenge. The resilience phenotype can, therefore, be considered robust across stressors, both health-related and non-health-related, and more practical for selection on the population’s future fitness when considering there will be new pathogens that arise for which we are currently unaware.

Selection for disease resilience targets those genes that allow an animal to have a tolerating consequence, or quicker recovery in their performance when challenged (Figure 1). Instead of targeted gene discovery for a single pathogen, the selection is placed on a multigenic scale within the genome, using quantitative and molecular tools inside our genetic toolkit. The Genesus answer to healthier pigs lies within genetic selection for disease resilience phenotypes.

Genesus has been involved in funding disease research for over 10 years. Several useful tools have been discovered from genome-wide association analyses and incorporated into the Genesus toolkit.

We have uncovered genomic regions that we place under selection to improve resilience to Porcine Reproductive and Respiratory Syndrome Virus (PRRSV).

We are monitoring genomic regions found to affect susceptibility to Porcine Circovirus Associated Disease (PCVAD).

Genesus is staying abreast of outside research and benefiting from our relationships within academia to improve our population’s resilience to E.Coli challenges.

Furthermore, disease resilience traits have more recently been identified, which will aid in filling the previously empty, phenotype void. These phenotypes are necessary for selection purposes, and Genesus is now able to key in on those specific attributes to identify more disease resilient animals.

The trek is not finished, however. Active research continues, and more tools continue to unfold for use in genetic selection for improved health. Diseases are becoming more numerous and geographically spread. For this reason, selection for disease resilience must continue to be a key component inside the genetic selection programs of swine.

Genesus continues its involvement in disease research and is working to actively combine genomics and disease resilience phenotypes in the selection for higher-health animals. In the forthcoming months, we will share more of the breakthrough discoveries from our involvement in major research projects involving Genome Canada, Genome Alberta, PigGen Canada, USDA National Institute of Food and Agriculture (NIFA) and the Alberta Meat and Livestock Agency. Through Genesus and these funding agencies, collaboration with projects and researchers at several major Universities around the world (e.g. University of Alberta, University of Saskatchewan, University of Guelph, Iowa State University, Kansas State University and University of Edinburgh) has transpired over the past decade.

We look forward to sharing in more detail what implementation has occurred inside of Genesus from our collaboration with researchers at these organizations, and our involvement in utilizing these resources.

Source:

Albers, G. A. A., G. D. Gray, L. R. Piper, J. S. F. Barker, L. F. Lejambre, and I. A. Barger. 1987. The genetics of resistance and resilience to Haemonchus contortus infection in young Merino sheep. Int. J. Parasitol. 17:1355–1363.

Doeschl-Wilson, A. B., B. Villanueva, and I. Kyriazakis. 2012. The first step towards genetic selection for host tolerance to infectious pathogens: Obtaining the tolerance phenotype through group estimates. Front. Genet. 3:265.

Pork Commentary, June 22nd, 2020 Jim Long, President-CEO, Genesus Inc.

Last week the U.S. hog market harvest reached 2,587,000, about 130,000 more than a week ago and a year ago. Packers are obviously getting more hogs killed as they navigate coronavirus issues including having enough employees at work. Packers have great motivation as the DTN Gross Packer Margins calculation is $53 per head, a year ago it was around $20 per head. We expect U.S. Packers to continue to ramp up production, motivated by excellent gross packer margins.

U.S. hog market weights continue to decline. The first four days last week had everyday weights about 1.5 lbs. lower than the same day the week before. Weights last week on the National Base were also over 1 lb. lighter than a year ago.

Some claim 4-7 million hogs backed up due to plant closings and shutdowns but we have a hard time, right or wrong, getting to that number with weights having dropped 10 lbs. liveweight since the first part of May. Also, we hear from the field a number of our Genetic customers are not backed up. Many are selling ahead in case of plant closures. The last week we heard of plants in the Eastern Corn Belt calling looking for hogs. The customers we do have backed up are in the Quad state corner of Nebraska-South Dakota-Minnesota-Iowa. There it is real. The multi-plant closures in that area have caused real problems.

We also know there has been ongoing euthanization of market hogs and smaller pigs. How many is anyone’s guess but it has and is happening.

Usually, this time of year is near maximum finishing capacity as all pigs to be harvested from now to January are in inventory. Question if the market thinks there 4-7 million hogs backed up what will market do if inventory is less than this? Should there not be upside? If you’re a pork buyer whether domestic or foreign, you all have the same news. All these hogs backed up, why would you want to be an aggressive pork buyer when this expected supply is coming? Bottom line we don’t believe 4-7 million hogs backed up. June 1 U.S. Hogs and Pigs Report will tell us the story.

Sow Harvest continues to be aggressive the latest weekly was 69,000+, last year’s average 57,500. It appears to us last quarters sow harvest was about 100,000 more than the same quarter a year ago. We also believe many poor skinny sows of little value (Hello world’s largest genetic company) that would normally go to slaughter are now being put down and not in sow slaughter count.

We expect U.S. breeding herd is down at least 150,000 in the quarter and would not be surprised if it’s down 200,000 or more. Whatever the number, the U.S. production capacity continues to contract.

SummaryThe June 1st Hogs and Pigs Report, in our opinion, has the makings to be a major market mover to the positive. For us producers let’s hope so.

Pork Commentary, June 15th, 2020 Jim Long, President-CEO, Genesus Inc.

For the second week in a row, U.S. market hog harvest was higher than a year ago. 2,457,000 vs. 2,439,000. We can only hope that U.S. plants can continue to ramp up production. Strong Gross Packer Margins certainly give an incentive.

Daily National Base Lean Hog Carcass weights continue to decline. The first four days of last week averaged 213.88 lbs; four weeks ago averaged 220.17 lbs. No doubt weights have come off the extreme highs. We certainly have a hard time fathoming how some can claim 4-7 million hogs backed up due to earlier plant slowdowns. In context, a week before averaged 215.51 and a year ago 214.58.

There is no way in our mind that hogs can be backed up to the extremes some are stating when we see average weights continuing to decline each and every week. We expect some producers are backed up while others have pulled hogs ahead. Depends on where in USA, which plant, fear of plant closing, feed ration management, etc. Many dynamics in play.

Question is how sow herd liquidation has happened. Last quarter December to February the USDA inventory indicated a 96,000 decrease. In that quarter U.S. sow slaughter was up 34,000 from the year before. When we look at the second quarter it appears to us that the U.S. sow slaughter will be up about 100,000 when final data is put together. We expect when combined with lower gilt retention and ongoing sow mortality the U.S. sow herd will decline in a range of 150-250,000. We realize this is a wide estimate.

We expect whatever it ends up on June 1st liquidation, currently cash isoweans and feeders at next to nothing and market hogs with a $40 loss per head is grinding the business to death. If it continues without profits more and more liquidation will happen. It’s hurting Big and Small. Some benefit from ownership in packing plants or percentage of gross packer margin but many do not.

Depending on the length and depth of the liquidation of the sow herd, packer capacity issues will not be a factor as millions of hog production disappear. Some call this Destructive Capitalism. Others destroying people’s livelihood and dreams.

Many of us have been in this business a long time. We remember the low prices of 1993-94 which ended most if not all the field farrowing – outside operations (now they would get premium). At the same time, there was the rise of Murphy Farm, Carrolls, Heartland Pork, Premium Standard Farm, Feed Company pig production in Purina. The low prices of 1998-99 hit and many of the organizations if not all ended up with restructured ownership due to the massive financial losses. Too big to fail was not true.

Over the last twenty years, there have been the issues of the hog cycle which continued to lead to further consolidation. 2019-2020 we have hit another big hog price issue. We have had Black Swan events related to ASF, Trade, and Coronavirus issues. Wham, Wham, Wham. It’s a big challenge. The word Force Majeure seems to have become as common as pigs per sow per year contracts of many types have been evolved. (nice word for broken). As a friend of ours says “no one goes broke if they can help it.”

By nature we are optimistic. Much as anyone in this industry needs to be. The upside we are producing a product that is the most consumed meat in the world. We know overtime the countries with the most competitive cost of production and access to markets will win. We also know that Darwinian Capitalism (hog cycle) will lead to higher prices from lower supply. It’s about capital and courage to get to the other side.

Pork Commentary, June 8th, 2020 Jim Long, President-CEO, Genesus Inc.

After several weeks of hog harvests significantly below a year ago, this past week the U.S. got to 2,452,000, up 42,000 from the same week a year ago. Certainly a positive sign that U.S. plants are getting closer to the new normal in the coronavirus situation and packers certainly have the incentive to push harvest numbers, the latest DTN Gross Packer Margin calculation is $70.

Harvest numbers have recovered faster than many predicted, obviously phenomenal profit margin motivated packers to get things going. What’s the saying “Follow the money!”

There are information services that charge for their astute knowledge of the Meat Industry. One of them last week wrote the following “We estimate there are 4-7 million hogs which have been backed up and ready to go to slaughter.”

Let’s consider this 4-7 million number of backed-up hogs. Some Farmer Arithmetic.

4 million hogs divided by 2.5 million hogs harvest a week is about 11 days of hog production;

7 million hogs divided by 2.5 million hogs harvest a week is about 17 days of hog production.

Let’s assume an indicator of hogs being backed up would be slaughter weights.

National Daily Lean Hog Carcass

Week Of

Avg. Carcass Weight

May 8, 2020

220.43

May 29, 2020

217.25

June 5, 2020 (Mon-Thursday avg.)

214.95

June 7, 2019

215.66

Hogs were 220.43 lb. carcass the first week of May indicating hogs were backed up for sure. Since then we have dropped at least 5 lbs. and now weights are in line with a year ago. It’s hard for us to fathom that any feed adjustments can back up 4-7 million market hogs (11-17 days) while weights have dropped continually the last four weeks.

We don’t believe numbers of 4-7 million hogs backed-up. Why?

Weights same or lower than a year ago;

The idea that there are 4-7 million more spaces for hogs is beyond comprehension of barn infrastructure.

We believe there are backed up hogs but they are mostly in the Southwest Minnesota-South Dakota-Northwest Iowa-Nebraska region. The closure in that area of Smithfield Sioux Falls, JBS Worthington, and Tyson plants for the length of time they were, backed up hogs there.

In other areas producers going to other plants are current with some more than current. Due to the coronavirus issues producers continually jammed as many hogs as possible in case their plant shut. Some producers are under 210 lb. carcass weight.

Probably hogs are not backed up as much as some speculate is because alternate harvesting happened with small plants and on-farm sales ramping up. Hogs moved all over the country as low hog prices and high pork prices created opportunities for some. Also, there has been euthanasia of market hogs and other weights. How much euthanasia is purely speculative, but we believe it has been significant enough to cut hog numbers.

Last week we wrote, watch the weights for the next two weeks. Last week we dropped couple lbs. If we continue this trend this week it will indicate to us that we are closer to current hog inventory.

Ramifications – we believe Lean Hog Future experts have bought into the 4-7 million hog back-up. Lean Hog Futures are terrible. If we suddenly discover that there are fewer hogs than the experts predict, there could be a sudden surge in hog prices as the market finds a big surprise. We will know soon enough; slaughter and their weight numbers don’t lie.

China

The below table shows the changes of market hogs produced by leading Chinese Public Companies for the four-month period January-April 2019 and 2020. As you can see, there was a significant drop overall in market hogs produced. It appears to us the reality of China’s lower hog production due to ASF is far from over. This in itself should continue to support Global Hog Prices.

We expect China will be back in U.S. market stronger now that Pork Cut-outs have declined from being over $1.20 lb.

Pork Commentary, June 1st, 2020 Jim Long, President-CEO, Genesus Inc.

Last week we observed that U.S. harvest weights were decreasing. This totally baffles us. There is no doubt the official USDA slaughter numbers have been significantly lower for the last six weeks compared to expectations or last year.

Last week we would have expected hog weights to hold or increase due to Monday being Memorial Day and Plants were closed. Instead, Tuesday-Wednesday-Thursday averaged 217.03 lb. carcass weight. The week before average was 217.20 lb. and a year ago 215.54 lbs. Three weeks ago U.S. lean hog weights were over 221 lbs.

It’s hard to believe hogs are backed up 5 million as some have stated. That is almost 3 weeks of U.S. weekly slaughter. Weight difference week over week and compared to last year don’t indicate anything close to this high a number.

In our opinion watch the next two weeks’ slaughter. We expect with current packer margins and plant productivity, weekly slaughters will be over 2.3 million head, watch the weights if they continue to decline it could be a strong indication that we are more current for various reasons (euthanization, non-major packer slaughter) then many expect. If so, we might get a nice bump in hog prices. We can hope.

Sow Slaughter

The latest weekly sow slaughter was 69,753 the week before over 70,000. Last year’s weekly sow slaughter averaged 57,500. From Dec 1st to Feb 29th the USDA Hogs and Pigs Report indicated the U.S. sow slaughter was 35,000 higher than a year ago. In March-April this year U.S. sow slaughter per week so far higher than March-April last year (up 36,000 total).

We sell breeding stock at Genesus. There is no doubt gilt sales have declined. Not only for us but for the whole genetic industry. Producers are protecting cash flow and concerned about the future. Lower replacements cut the breeding herd.

Our farmer arithmetic on this. Looking at breeding herd decline from Dec to June 1st (6 months).

Dec-Feb = 96,000 USDA report

March-May = 180,000 (low side estimate 14,000 a week avg.) or 260,000 (high side estimate 20,000 a week avg.)

Potential loss of Pig Production = 5-7 million head a year.

Wherever it ends up there are fewer hogs coming and we expect breeding herd liquidation will not stop June 1st. Could end up with breeding herd down 500,000 before all the dust settles.

U.S. Pork Export

It’s not hard to imagine that U.S. Pork Exports would drop when hog slaughter numbers have declined significantly over the last six weeks. Less Pork – less to Export. Also, the huge jump in Pork cut-outs that got over $1.20 lb. would have foreign buyers to take pause.

The good news, it appears exports continue to run about 12-15,000 tonnes a week higher than a year ago (about 120-150,000 market hog equivalent). These types of numbers if they continue will support Pork cut-outs and hog prices as plants come into fuller harvest production.

Genesus and The National Hog Farmer collaborate annually to survey the Global Swine Industry. The result is the Global Mega Producer Report which identifies the companies with over 100,000 sows.

The 2020 list identifies 34 Global Mega Producers that together own more than 11.5 million sows, adding more than 2.5 million sows to global production. These companies are located in 9 different countries respectively.

Click below for the listing and brief description of each company.

Editor’s note: Jo-Ann McArthur is the President and Founding Partner of Nourish, a marketing agency that specializes in field-to-fork food and beverage, working across all aspects of the food ecosystem. Clients include producers, processors, retailers, manufacturers, food service and restaurants. Jo-Ann can be contacted at j@nourish.marketing. Sign-up for the agency’s monthly newsletter at www.nourish.marketing.

I always like to say that Nourish is an agency that knows a lot about a little. We have the dual privileges of specializing in the food industry and working across its entire ecosystem. As a result, we are often able to connect dots that others may not.

We publish an annual Trend Report, now in its fourth year. And by trends, I mean cultural forces and shifts, not fads. Fads are like a one-time volcanic eruption: they are briefly hot before they cool and then disappear. Trends are the tectonic plates that move beneath us and reshape the landscape. New food systems, as well as product development, take time, so we need to make sure we are looking at a longer-term horizon.

When we look at trends, we are not passing judgement or making value statements. We are just reporting what we see coming. Looking back, we are happy to say that all the trends we have covered since 2017 are still actively reshaping the food industry and providing opportunities for producers, manufacturers, retailers and food service providers.

Here are some of the trends that could affect you most in 2020 – both positively and negatively.

Make way, Millennials: Gen Z is on the rise

In our 2019 Nourish Trend Report, we identified a shift from Millennials to Generation Z as one of the top eight trends to watch in the food industry. Gen Z members today are roughly between the ages of four- and 24-years-old. They comprise a quarter of the current population, which makes Gen Z more numerous than both Baby Boomers and Millennials. Over the next few years, that figure will balloon to 33 per cent.

Remarkably, while they are still establishing behaviours, even the youngest are already influencing their parents’ and grandparents’ buying decisions. What we are learning is that they are markedly different from previous generations, especially when it comes to the way they view meat.

Gen Z is engaged, aware and optimistic about their ability to effect change. Almost half of all surveyed said they believe they can make the world a better place. Importantly, they have grown up in a digital world where no question cannot be answered with their mobile device, so they expect radical transparency. And they want proof – a claim without evidence (or a picture) is just noise.

We call this “Made Matters.” It is shorthand for things consumers care about: quality, ingredients, health, animal welfare, environmental and labour concerns. They want to know how and where food was grown or raised. Both Gen Z and Millennials are more likely to purchase animal-welfare-certified products.

The “Eating Clean” definition is expanding to include not just what is in food but the entire journey, from how it was raised and by whom, to the treatment of workers, animals and the environment. All these factors are growing in importance and are top-of-mind with younger consumers.

Canadians have a lot to learn about farming

Social licence still matters for producers.

Unfortunately, while Canadian consumers trust Canadian farmers, they do not fully trust our food system. The Canadian Centre for Food Integrity’s 2019 Public Trust Research demonstrated a dangerous disconnect between consumer perception of the food system and reality that needs to be addressed. Consistent with last year’s data, it shows that only one in three Canadian consumers believes Canada’s food system is on the correct course. Fortunately, those who feel the food system is going in the right direction outnumber those who think it is headed down the wrong track.

The same research shows that 91 per cent of Canadians know little or nothing about modern farming practices, but 60 per cent of Canadians are interested in knowing more – a trend we reviewed in the 2020 Nourish Trend Report. The disparity between consumer beliefs and on-farm practices must be addressed. As insiders, you and I know Canadian agriculture has world-class standards, but consumers are less clear on that fact.

Eating meat is no longer a black-and-white issue

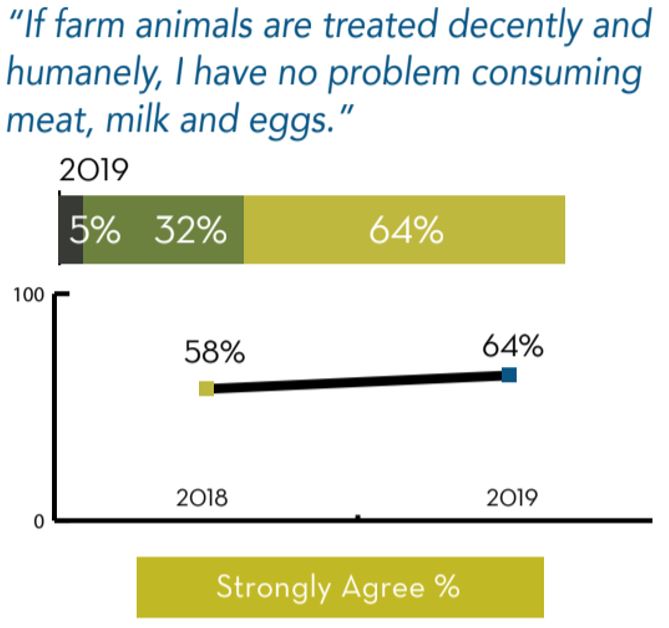

The number of Canadians who identify as vegan or vegetarian is on the rise. Still, 64 per cent of consumers said they had no issue consuming meat “if farm animals are treated decently and humanely.” Consumers are looking for reassurance about how the animals were treated, backed by audits and robust standards. Producers have an opportunity here to share their best practices and excellent records on animal welfare.

In the 2018 Nourish Trend Report, the rise of “plant-based” eating was one of the disruptive trends we shone a light on. More Canadians across cultures and generations are reducing their meat intake and adopting a flexitarian lifestyle to support animal welfare, the environment and their health – the top three reasons cited in a Dalhousie University study. People under the age of 35 are three times more likely to consider themselves vegetarians or vegans than people 49 or older.

In 2020, attitudes towards sustainable consumption are reaching a crucial tipping point away from aspiration and toward necessity. Research conducted with online Canadian members of the Angus Reid Forum (on behalf of The Meatless Farm), found that 77 per cent of consumers say they understand the damaging environmental impact of eating red meat, and 74 per cent believe it is important to reduce their carbon footprint. Yet, only 38 per cent of Canadians reduced their meat consumption to do so.

Will we see the emergence of a “climatarian” diet, where consumers start making food choices not based on food preferences or values but instead based on carbon footprint and environmental impact?

The plant-based trend is here, and it is not leaving

Maple Leaf Foods’ plant-based Lightlife product line is an example of how traditional meat companies are diversifying and rebranding as “protein” companies.

Blended or hybrid products (such as mixed plant and dairy, or plant and meat) are starting to emerge as an easier way for consumers to moderate their carbon footprint without giving up their preferred taste for animal products. Rather than doing flexitarian as an “either/or,” it can be done as an “and.” Blended protein is an old concept that recent economic prosperity has taken us away from. During the Second World War period, there were Victory posters in Canada about protein rationing. Boomers grew up with mothers who mixed ground meat with oats to make the grocery money extend further. What is old is new again!

In the U.S., Tyson Foods recently launched Raised & Rooted, a blended meat and pea-based protein, shortly after selling its share in Beyond Meat, a totally plant-based processed meat substitute. Perdue, a major chicken processing company, offers a Chicken Plus line of products combining chicken and vegetables.

These products leverage the technology necessary to make plant-based products stable but incorporate real meat to deliver the taste and texture consumers crave. Given that plant-based ingredients are in short supply, this may soon be the only way new players can enter the market while staying competitive.

In Canada, Maple Leaf Foods, shifted its vision to focus on becoming “the most sustainable protein company on Earth.” (Note the exclusion of the word “meat.”) It has positioned itself for the future by creating a separate plant-based division and building a $300 million facility in Indiana to support growth.

We have seen rapid changes in consumer behaviour with the COVID-19 crisis. Some of that behaviour will have a legacy effect on our food system. We have already seen a shift-in-stomach from food service to grocery as more people cook at home. Consumers will want to support their communities and neighbours, so we should also see an even more significant move to locally- and Canadian-grown food.

Editor’s note: Bijon Brown is the Production Economist for Alberta Pork. He is currently working on a cost of production study for producers, to use as a benchmark for comparing profits across the value chain. He can be contacted at bijon.brown@albertapork.com.

Hog production differs regionally not only by the feed inputs used but also by the pork markets served. Looking at the current trends in the Alberta pork export market, we can examine the difference between Alberta exports and exports from the rest the country. By acknowledging those differences, we can begin to understand where Alberta producers sit relative to producers in other key provinces.

U.S. share of Canadian pork export market on the decline

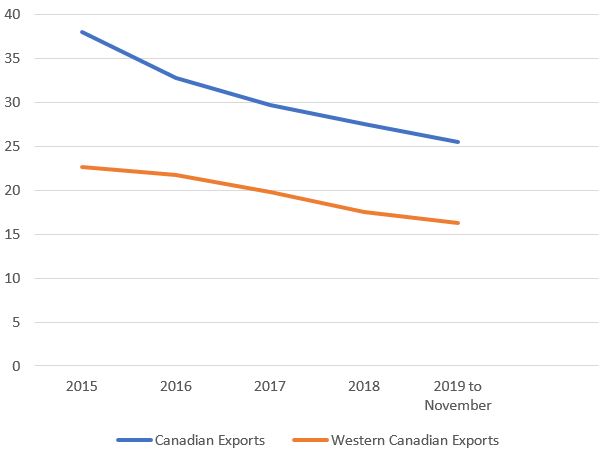

U.S. share of western Canadian and all Canadian exports. Source: Statistics Canada, Prepared by AAFC/MISB/AID/Market Information Section

Although the Canadian export market is largely dominated by shipments destined for the U.S., its relative share of the Canadian export market has declined over the past five years. From January to November 2019, roughly a quarter of all Canadian pork exports went to the U.S., down from about to 40 per cent in 2015. Meanwhile, the share of exports destined for Asia trended up to 21 per cent from 18.5 percent in 2015. The largest export market for central Canada continues to be the U.S., but Japan is the largest export market for western Canada.

From January to November 2019, western Canadian pork export volumes were about 440,000 tonnes, close to 2015 levels, but about 14 per cent below the five-year peak in 2017. Manitoba and Alberta accounted for most of the pork exports. Alberta exported more than 110,000 tonnes of pork products, down roughly 10 per cent from the corresponding period in 2018. This largely reflected a 29 per cent drop in exports to the U.S. and was partially offset by increased exports to Japan and Mexico. The decline in pork exports to the U.S. has resulted in the share of total Alberta pork exports dipping from 25 per cent in 2015 to 20 per cent in 2019. In the meantime, the Japanese share of the export market rose from 35 per cent in 2015 to 42 per cent in 2019.

Alberta exports fetch a premium in Asian markets

Canadian and Albertan pork export price to select destinations. Source: Statistics Canada, Prepared by AAFC/MISB/AID/Market Information Section

The shift towards Asian markets and away from the U.S. market has been mainly driven by economic incentives. Over the past five years, Canadian exports to Japan have attracted a premium over U.S. exports, averaging almost $1.20 per kilogram, with the Alberta export price premium averaging $1.80 per kilogram. Over the past two years, Alberta export prices for shipments to the U.S. dipped below $3.10 per kilogram from a five-year high in 2017 of around $3.50 per kilogram. Meanwhile, the average export price at the national level was $0.40 per kilogram higher, indicating that Alberta pork is being discounted in the U.S. market relative to pork shipped from other provinces. In contrast, Alberta pork shipments to Asia received a higher price than pork shipped from other provinces.

Alberta producers paid less for hogs

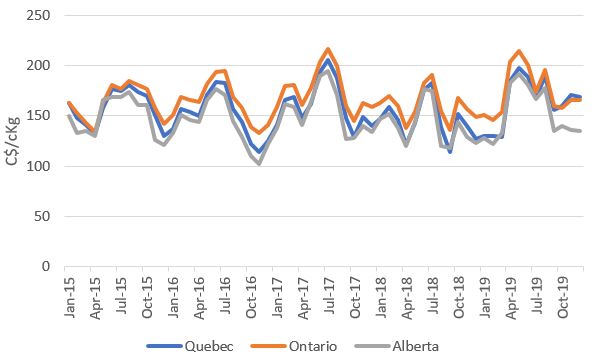

Monthly hog base prices in select provinces. Source: Statistics Canada-Table: 32-10-0077-01.

Despite the shift to higher valued export markets, the value of Alberta pork exports eased 13 per cent over the past five years, largely reflecting a 24 per cent decline in overall exports. In a region that exports over 40 per cent of its pork to markets paying a premium, it appears the price signals to Alberta producers have become distorted.

While Alberta pork attracts a premium, Alberta producers have seen base prices that were $0.08-0.20 less per kilogram for their hogs compared to producers in Ontario and Quebec. Currently, producers are paid a price that is derived from U.S. markets, which represents less than 20 per cent of wholesale export value. The economic realities in the U.S. market are no longer consistent with a significant portion of western Canadian wholesale pricing; it ignores the preferential premiums accessed in Asian markets.

Accordingly, farmers face lower prices, and these lower prices disincentivize investment and production. Lower prices signal that Alberta producers should reduce pork supply, which would reduce pork processed, marketed and, ultimately, exported. All this, even though there is increased demand through higher price signals coming from Asian trading partners. Prices to producers must more accurately depict prices earned downstream in the value chain. Otherwise, the inability to clearly send price signals through the value chain will leave money on the table for the entire industry, not just producers.

Pork Commentary, May 25th, 2020 Jim Long, President-CEO, Genesus Inc

About a month ago President Trump and Ag Secretary Perdue announced the Coronavirus Food Assistant Program (CFAP). At the end of last week some more details were announced re hogs.

Hogs Eligible

Unit of Measure

ACT 1 Payment

Act 2 Payment

Pigs < 120 lbs.

Head

$28.00

$17.00

Hogs > 120 lbs.

Head

$18.00

$17.00

Producers must provide the following information for CFAP:

Total sales of eligible livestock, between January 15 to April 15, 2020, of owned inventory as of January 15, 2020, including any offspring from the inventory (Act 1);

Highest inventory of eligible livestock, by species and class, between April 16, 2020, and May 14, 2020 (Act 2).

A single payment for livestock will be calculated the sum of the producer’s number of livestock sold between January 15 and April 15, 2020, multiplied by the payment rates per head, and the highest inventory number of livestock between April 16 and May 14, 2020, multiplied by the payment rate per head.

CFAP payments are subject to a per person and legal entity payment limitation of $250,000. This limitation applies to the total amount of CFAP payments made with respect to all eligible commodities.

Participants that are corporations, limited liability companies, and limited partnerships these corporate entities may receive up to $750,000 based upon the number of shareholders who contribute at least 400 hours of active person management or personal active labour.

Observation

U.S. hog producers have been hit hard by Coronavirus implications. It is good the U.S. government is providing significant money to fill back some of the losses. It will not make most producers whole but it will help.

Sow Slaughter

The latest sow slaughter data for the week ending May 9 was just over 70,000. The largest we can remember in a long time. In 2020 the average weekly sow slaughter was 57,500. There is no doubt the U.S. sow herd is rapidly declining.

This is Interesting

The general premise in the industry is that hogs are backed up due to lack of harvesting related to Coronavirus issues. Below is some data that baffles us.

The week of May 15 the average carcass weight on the National Daily Base Slaughter Data was 220.17 lbs. avg carcass data. Last week the average weight in same database was from Monday-Thursday 217.5 lbs. (Same week a year ago 214.19)

That’s a drop of 2.6 lbs last week from the week before. How can we explain weight dropping so significantly when hogs are supposed to be backed up? It hasn’t been hot? Harvest numbers are still below a year ago? Has euthanasia been that large? Have feed adjustments pulled down weights? Have open plants have producers pushing hogs in? Are meat lockers and on-farm selling? We are baffled! It will be interesting to see what weights do this week. Could this be a factual signal hogs are not backed up as most believe? Crazy business.

Other Markets

We know the U.S. hog market has been miserable for most. It appears also some other countries have seen decline with most attributing to Coronavirus issues including decrease demand from lower incomes due to unemployment, restaurant usage decline, currency fluctuation and lower economic robustness.

March 26

May 20

China

2.32

1.92

Russia

54.23

55.58

Spain

75.51

62.91

Brazil

50.17

35.46

Mexico

53.68

34.41

Every country is down significantly except Russia which has an internal market without significant imports or exports. The other countries have seen declines between $30 to $100 per head in the last two months. Not a positive picture of demand as we know supply has not changed significantly.

Pork Commentary, May 19th, 2020 Jim Long, President-CEO, Genesus Inc.

Last week U.S. Pork Packers started to recover some production capacity lost to Coronavirus plant issues.

Weekly Harvests totals:

Week of May 1st – 1.553 million

Week of May 8th – 1.775 million

Week of May 15th – 2.103 million

Last Year May 15th – 2.352 million

It’s good to see a 500,000 head improvement in the last two weeks.

Observations

Packers have worked to get Plants operational and to greater capacity. Great efforts have been made to put in place enhanced employee safety measures to protect workers from Coronavirus.

With U.S. pork cut-outs Friday closing $1.10 lb. the Gross Packer margin for Packers reaching over $100 per head. This in itself is a huge incentive to harvest as many hogs as possible. From what we know the current gross packer margins are at record levels. For Plants not at capacity, it is a lost opportunity in these highly profitable times. There must be big pressure to get fully operational.

There is no doubt market hogs are backed up. We have read reports that some claim up to 10 million. We expect it’s currently give or take 2 million. It’s a lot and a big challenge to get current. We hope this next week increased packer capacity might get us to the same weekly harvest as a year ago.

There are efforts to get compensation for market hogs being euthanized. As far as we know that hasn’t happened. Some market hogs are getting euthanized how many is mostly a guess. No one wants to publicize this grim reality. In the meantime, sow herd liquidation is ongoing. It’s across the specter of the industry with some Pork Powerhouses being involved.

The USDA announced April 17th a Coronavirus compensation program for ag and hog production. No real details have been released; it is supposed to be soon. There is no doubt hog producers have suffered due to Coronavirus. Dirt cheap pigs and hogs have been crushing to most swine producers.

Summary

We need to keep seeing increased hog harvesting. Up 500,000 head a week in last two weeks is right direction. Packers have huge financial incentive to get hogs through their plants with record Gross Packer Margins. We hope and are optimistic that harvesting numbers will continue to increase.

Register today for the Global Hog Industry Virtual Conference

What pork companies made the 2020 Global Mega Producer list? National Hog Farmer Content Director, Ann Hess, unveils this year’s top companies. Plus, Jim Long of Genesus, along with Tom Stein of Maximus Systems/Maximus Ag Technologies, provide insight as to the market trends shaping the global hog industry in 2020.

Speakers:

Max Amstrong, This Week in Agribusiness host (moderator) Ann Hess, Editor, National Hog Farmer Jim Long, President and CEO, Genesus Tom Stein, Senior Strategic Adviser, Maximus Systems/ Maximum Ag Technologies

Biosecurity protocols, including signage, are a reality of modern, commercial hog production.

Effective biosecurity management is key component of a successful hog operation. Proper biosecurity protects both herds and humans from disease incursions that can affect animal welfare, staff health and business continuity.

Over time, the pork industry has been compelled to adapt biosecurity practices to fit the evolving reality of production, which means fewer but larger farms, workers travelling overseas, imported feed and equipment and other considerations that challenge the disease-free status of a farm.

Dr. John Harding, Professor, Western College of Veterinary Medicine, University of Saskatchewan, acknowledges that biosecurity remains the number one defence against disease: “We have a very complex animal health intensive livestock sector now involving multiple sites and large airspaces, with pigs being transported great distances,” he said in an interview with Farmscape. “We also have emergence of diseases or new viruses, new pathogens, emergence of antimicrobial resistance, potential zoonotic diseases – so there’s a lot of change that’s happened over the years.”

For producers, it is a constant battle to establish a biosecurity culture within a farm. Biosecurity is demanding, and most would sooner ignore it, if that was a reasonable choice. Ideally, biosecurity principles are backed by formal, written documentation, such as on-farm protocols. After that, discipline and conscientiousness must take over.

Standards demonstrate producer commitments

Alberta Pork’s cost of production study, launched in January 2020, is seeking to better understand producers’ on-farm costs.

In January 2010, based on recommendations of the former Canadian Swine Health Board Biosecurity Advisory Committee, a first draft of the National Swine Farm-Level Biosecurity Standard was created. This voluntary standard is a tool for producers and industry stakeholders to tailor biosecurity measures to individual farm needs and provincial regulations.

The adaptable biosecurity standard addresses various planning considerations, direct and indirect routes of potential contamination and on-farm animal health. Underscoring these considerations are routine veterinarian check-ups, the use of medicines and many material costs including disposable gloves, masks and booties, plus disinfectants, degreasers and other products that are required for an effective program. All of these considerations come with a price tag, and those costs are often buried or overlooked, which is why further efforts are being made in some provinces and nationally to understand exactly what producers are paying when it comes to biosecurity.

The dilemma for producers is understanding and appreciating the importance of these practices while having little or no money to cover them. With that hit to producers’ pocketbooks constantly hammering away at already meagre farm incomes, it adds to the list of stresses that have producers reconsidering their hog operations altogether.

Every little bit adds up over time, creating a “death by a thousand cuts” scenario. When producers look across the table and see processors’ profits continuing to roll in, they are left wondering what value there is to their additional efforts.

Cleanliness does not come cheap

Blue Water Wash in Red Deer, Alberta features 20 wash bays and Canada’s first industrial-strength drying and baking bay for livestock trailers, but this level of clean comes with a cost.

From one producer to the next, the realistic implementation of biosecurity protocols differs. Implementing biosecurity protocols extends beyond putting words to paper. Words require action, and action requires paying the running tab of costs associated with cleanliness. One of the most critical precautions and significant costs is truck washing.

In Alberta, nearly half of all pigs are self-hauled, while the other half are hauled commercially. In either situation, thorough cleaning is required after each load is delivered to the plant. The price to thoroughly wash and bake a livestock trailer commonly reaches into the hundreds of dollars.

Specifically, a proper truck-and-trailer cleaning job often costs no less than $1 per pig for a load of 200 pigs. This adds insult to injury after already having shipped a full load at a loss of several hundred dollars, with no direct financial incentive to reinforce the good behaviour. For many producers, the cost raises a series of questions: Do I wash with detergent, rinse with water, bake and disinfect? Or do I just wash and rinse? If no-one notices, can I get away with only rinsing?

Sadly, this process of rationalization is well-known. Experts agree, and most stakeholders in the value chain are aware, that enhanced biosecurity requires extra attention to detail and a concerted effort. But if the money is not there, is it surprising that any person in this situation might consider cutting corners? It is a dire prospect. In a world where several hundred dollars can put food on a family’s table for a matter of weeks, a truck wash might, unfortunately, not look like the best investment, even if it is critically important.

While all transport trucks are required to be clean before arriving on-farm, for a very small minority of producers who self-haul pigs, on-farm wash bays are an enhanced biosecurity feature used before the truck leaves the farm, which helps further eliminate potential biosecurity gaps. What does not change, no matter the producer, is that making use of appropriate post-delivery truck washing services means paying for the service each and every time he ships pigs, usually weekly… unless he decides not to, due to the prohibitive cost. That decision fundamentally challenges the quality assurance guarantees that processors rely on to influence consumers’ perceptions of food safety further down the line, which demands the implementation of additional best practices at the processing and retail levels.

Quality assurance depends on producer action

All commercial pork producers in Canada – those that sell their pigs to federally inspected slaughter facilities – are certified under the Canadian Quality Assurance (CQA) program or the new Canadian Pork Excellence (CPE) program. Quality assurance covers biosecurity at the farm and plant level, but these conditions inform mostly food safety, not farm management, in the strictest sense.

In 2019, the CPE program was launched with the intention of phasing out and modernizing CQA, which was first implemented in 1998. While CPE program adherence varies across Canada, the number of certified producers is steadily growing. In Alberta, objections to the cost of CPE have stalled the implementation of the program.

CPE includes 10 modules, including one for biosecurity. Under the biosecurity module, there are recommendations for feed and water, proper handling of live animals, pest control techniques, equipment maintenance and more. Program recommendations are consistent for all producers, but it is left up to producers to make choices that fit their individual operations. Almost universally, these choices are driven by financial impact. Whatever choices are made must be deemed acceptable by program validators, which is a measure of the program’s integrity. Individual producer choice does play a role in keeping costs down, but across the country, in most jurisdictions where pigs are raised, options are often limited.

Disease-free pigs translate into safe food

Food safety in Canada continues to evolve. In January 2019, the Canadian Food Inspection Agency (CFIA) released its latest food regulations.

The challenge of maintaining strict biosecurity is compounded by the increasing costs producers must pay to meet quality assurance demands, which, for processors, are the basis on which their brands’ reputations are built.

For producers, the decision whether or not to embrace quality assurance places them between a rock and a hard place: pay for the program and sell to federal packers, or choose not to, and rely on other outlets such as provincially inspected plants or other marketing routes, which are few. Most often, this kind of decision would completely change the nature of an operation. For large-scale producers who raise the vast majority of hogs across the country, supplying our largest processors, it would be unconscionable.

A safe food system is paramount for Canadians and our international export partners. If food safety cannot be guaranteed, everyone in the value chain suffers. Food safety starts with proper biosecurity undertaken by producers and continues with further proper handling by processors and retailers. Food service establishments and consumers too have a role to play when preparing food in restaurant kitchens and at home.

While producers are more than willing to take seriously the demands of biosecurity, shrewd business considerations can undermine proper procedure, begging the question: if producers are not reasonably able to cover biosecurity costs, who will be left to produce the safe food that is generating record-setting revenues for some in the supply chain while taking every last penny from others? In the end, biosecurity on-farm and food safety in the plant, grocery store and at home are only as strong as the weakest link. For our part, as an industry, that means sharing the burden fairly.

The Path to Genetically Healthier Pigs

by: Chad Bierman, Ph.D., Geneticist, Genesus Inc

Pathogens are a global threat to the swine industry. They arise from bacterial, viral, fungal, and parasitic sources. Numerous and often prone to mutation, with a tendency to become immune to treatment efforts over time.

Production flows within the North American swine industry routinely face challenges from multiple pathogens, and a resultant annual cost to the North American swine industry estimated in the billion-dollar range; with PRRS estimated at $664 million alone (AASV 2011 Position Statement on PRRS elimination). This suggests the swine industry would benefit from animals that have a higher capacity to survive health challenges.

An animal’s ability to withstand a disease challenge can be defined in many ways. Resistance, Resilience, Tolerance, and Robustness are all relevant descriptors. Genetic selection for each concept is uniquely defined, distinctively implemented, and depending on the circumstances, it can be beneficial under differing situations. Genetic selection for disease resistance seems optimal, as an animal resistant to a disease would appear to have an advantage over an animal that is not able to control a disease challenge; however, targeting a specific pathogen requires a considerable amount of upfront investment. Adding to that, the earlier-mentioned fact that there are numerous pathogens presents a real challenge to become resistant to them all. Viruses also tend to mutate, which can lead to low-rewarding efforts should the targeted pathogen suddenly transform and become re-infective to the population.

Selection for disease tolerance instead of resistance recognizes that an animal can still perform under the burden of varying disease levels. However, selection for disease tolerance requires simultaneous measurements on both performance and the levels of infection. Another downside to genetic selection for resistance or tolerance is the challenge of acquiring continuous records of the pathogen burden. The burden levels will likely vary over time, yet are required for genetic selection in both instances (Doeschl-Wilson et al., 2012).

A final hurdle is that pathogen burdens do not exist within high-health nucleus herd environments that the pork industry demands. Therefore, an alternative approach is warranted.

The concept of disease resilience offers the aforementioned alternative. It is a combination of resistance and tolerance and is defined as the ability of an animal to maintain performance across environments when exposed to pathogen challenges (Albers et al., 1987). Disease resilience is unique in that selection in favor of does not require specific knowledge of any certain pathogen or level of challenge. The resilience phenotype can, therefore, be considered robust across stressors, both health-related and non-health-related, and more practical for selection on the population’s future fitness when considering there will be new pathogens that arise for which we are currently unaware.

Selection for disease resilience targets those genes that allow an animal to have a tolerating consequence, or quicker recovery in their performance when challenged (Figure 1). Instead of targeted gene discovery for a single pathogen, the selection is placed on a multigenic scale within the genome, using quantitative and molecular tools inside our genetic toolkit. The Genesus answer to healthier pigs lies within genetic selection for disease resilience phenotypes.

Genesus has been involved in funding disease research for over 10 years. Several useful tools have been discovered from genome-wide association analyses and incorporated into the Genesus toolkit.

Furthermore, disease resilience traits have more recently been identified, which will aid in filling the previously empty, phenotype void. These phenotypes are necessary for selection purposes, and Genesus is now able to key in on those specific attributes to identify more disease resilient animals.

The trek is not finished, however. Active research continues, and more tools continue to unfold for use in genetic selection for improved health. Diseases are becoming more numerous and geographically spread. For this reason, selection for disease resilience must continue to be a key component inside the genetic selection programs of swine.

Genesus continues its involvement in disease research and is working to actively combine genomics and disease resilience phenotypes in the selection for higher-health animals. In the forthcoming months, we will share more of the breakthrough discoveries from our involvement in major research projects involving Genome Canada, Genome Alberta, PigGen Canada, USDA National Institute of Food and Agriculture (NIFA) and the Alberta Meat and Livestock Agency. Through Genesus and these funding agencies, collaboration with projects and researchers at several major Universities around the world (e.g. University of Alberta, University of Saskatchewan, University of Guelph, Iowa State University, Kansas State University and University of Edinburgh) has transpired over the past decade.

We look forward to sharing in more detail what implementation has occurred inside of Genesus from our collaboration with researchers at these organizations, and our involvement in utilizing these resources.

Source:

Albers, G. A. A., G. D. Gray, L. R. Piper, J. S. F. Barker, L. F. Lejambre, and I. A. Barger. 1987. The genetics of resistance and resilience to Haemonchus contortus infection in young Merino sheep. Int. J. Parasitol. 17:1355–1363.

Doeschl-Wilson, A. B., B. Villanueva, and I. Kyriazakis. 2012. The first step towards genetic selection for host tolerance to infectious pathogens: Obtaining the tolerance phenotype through group estimates. Front. Genet. 3:265.