Editor’s note: Lauren Martin is Senior Director, Government Relations and Policy, Canadian Meat Council (CMC). She can be contacted at lauren@cmc-cvc.com.

By bringing together producers and packers, Canada Pork continues to build bridges across the value chain, supporting markets here in Canada and all over the world.

Canada Pork’s 2023 Annual Conference was held in Toronto in early February, inviting participants to learn more about the organization’s accomplishments for the past year and challenges facing the industry today, along with its priorities and an overview of its strategic direction for domestic and global markets.

Since 1991, Canada Pork has brought together representatives from the Canadian Pork Council (CPC) – including provincial pork producer organizations – and the Canadian Meat Council (CMC) – including federally inspected meatpackers – to create a definitive link in the pork value chain.

Canada Pork’s Annual Conference was another opportunity for these stakeholders to share the same space and rub elbows with individuals from across the sector and country. As a first-time attendee, representing CMC, I found the information sessions and networking opportunities very useful, as someone who is learning more about the pork sector and how we all collaborate.

Conference participants were able to hear from a lineup of guest speakers, including Brett Stuart of Global AgriTrends, who provided a global economic outlook for pork, and Sylvain Charlebois of Dalhousie University, who gave us his perspective on the challenges facing Canadian agri-food and pork’s place in the equation.

Surveying the global pork landscape

Considering Canada exports approximately 70 per cent of its pork production, our reliance on trade and foreign markets cannot be understated. Stuart provided a high-level summary of global economic trends from the context our industry is operating in. His presentation also touched on some government regulations driven by environmentally focused or animal-welfare agendas that will impact our industry, including Prop 12 in California, the European Union’s (E.U.) climate and welfare policies that are restricting pork production across the pond, and federal emissions reduction targets here at home.

Stuart’s presentation fit nicely within the conference program, as Canada Pork staff took to the stage later in the day to discuss how they are addressing these market conditions, to help facilitate pork exports. Of note in the year ahead, Canada Pork said they will look to take advantage of the newly reinstated access to China and the Government of Canada’s Indo-Pacific Strategy.

Providing a pork perspective closer to home

Sylvain Charlebois, the ‘Food Professor,’ is often asked by national news media outlets to speak about food issues for the public. His presence on social media has also sparked intense debate and opened eyes to agri-food system challenges.

Charlebois, popularly known as the ‘Food Professor’ on social media, can be quite the lightning rod for a range of opinions online, and in person, he may be even more compelling when not restricted to just 280 characters to explain his perspectives on the Canadian agri-food system.

One of the main subjects Charlebois covered was the price of food these days, especially protein, as many Canadians have voiced their concerns over inflation. He framed pork as the most affordable protein, even following it up by sharing a few social media examples showcasing some of the conversations he’s had.

Despite the consumer price advantage of pork, Charlebois believes Canadians haven’t yet flocked to pork as the saviour to the protein unaffordability dilemma.

Preparing for what’s to come

Ongoing threats to the Canadian pork industry continue to linger. Stuart described African Swine Fever (ASF) as the ‘wild card’ with any global pork trends, and how its presence anywhere impacts access to foreign markets.

For Canada to have a chance at weathering ASF, should it arrive here, we will need the domestic market to absorb as much of the excess pork it can. While it might be an easy ask to get Canadians to do their duty and eat more bacon, all cuts will need an increase in consumption if the worst should come to pass. My key takeaway from this situation is to consider our industry’s role in promoting domestic pork consumption, leveraging current affordability concerns and favourable supply, in the event borders close to trade.

From CMC’s point-of-view, we ask, what can pork processors do to remain competitive within international markets, while also offering innovative products that are desirable and on-trend with today’s domestic consumer? This is a critical component to the industry’s ASF preparedness efforts. As they say, an ounce of prevention is worth a pound of cure.

Pork Commentary Jim Long President – CEO Genesus Inc. May 30, 2023

Every day we hear of different entities deciding to cut sow production. To say it’s major seems to us an understatement. The industry financial losses are significant. It’s not just what has happened the last few months but a continuation from the Covid price collapse, high feed prices and continued increase in other costs (labor, utilities) that has pounded the industry. You only need to look at financial results of public swine companies to see the reality of the economics.

Much of the sow liquidation information is anecdotal. The only public announcements of sow liquidation have come from Smithfield Foods and Olymel in Canada. The only definitive number are from Olymel announcing, who last week announced liquidation of 17,000 sows.

We are hearing daily of individuals or corporations cutting back. It is at a level as great or greater we have ever heard.

How great will be the sow liquidation has yet to be determined. The longer losses continue the greater the liquidation. We believe at this point at least 300,000 sows of liquidation have been put in motion in USA, Canada, Mexico combined. Every week losses continue at current levels; we expect to add 15 – 20,000 more sows a week to the 300,000.

Other Observations

As we go forward not only will there be empty sow units going forward but empty finishers. 300,000 sows gone means 3 million empty finishing spaces.

Will productivity gains make up the sow herd liquidation. PigCHAMP a major U.S. pig production database has data on that.

PigCHAMP Average Annual Summary Results

2018

2022

Pigs Weaned per Sow/Annual

24.11

23.98

Sow Mortality

11.68%

14.54%

Data shows no productivity gain per sow. At the same time U.S. wean to finish mortality continues to climb. Our calculation 300,000 sows will be roughly 5.5 – 6 million fewer market hogs per year. The 3% increase in sow mortality costs $1,000 sow loss opportunity per head is about $1.8 billion per year to industry vs. 2018. Real Money. Good idea to have sows that live.

Prop 12 – recently talking to a group that just built a Prop 12 farm. They estimated farrow to wean cost vs. standard sow unit was $1,000 a sow more. Couple with lower farrowing rate and smaller litter size means. Certainly, magnified cost of production.

The extra cost to renovate old facilities to meet Prop 12 or others will also lead to fewer sows. Many producers in their 60’s, many asking why to invest into a money losing industry. What’s the end game?

Current Hog Price in Spain is 99¢ U.S. lb. liveweight. U.S. hog price is 61¢ lb. liveweight. 280 lb. lb. hog x 38¢ lb. difference = $106 per head. Big Money difference.

Little wonder U.S. pork exports to Asia are going up. Arbitrage.

The Spain (Europe) price is a result of huge liquidation in Europe of at least 1 million sows.

The liquidation in North America will result in higher prices in late 2023 into 2024 if not sooner.

Reports from China continue to indicate major liquidation. One company capacity 100,000 sows now have 75,000. Another company now 250,000 sows capacity 400,000. Lots of empty barns and lower sow inventories in others. ASF and continued losses of $50-60 per head is cutting sow herd. When the dog hits the end of chain (we expect this summer) the China price will explode.

To use the cliché “The Elephant in the Room.” Lean Hog Futures continued to trend lower last week. May Cash hogs at least $15 per head now higher than June Futures. Not sure lean hog futures can be explained they are quite low. Let’s hope lean hog futures are totally wrong relative to market direction.

Iowa – S. Minnesota cash hogs were 67.44¢ on April 24th. Last Friday (May 19) they were 87.73¢ lb. A 20¢ lb. gain in 3 weeks or up over $40 per head. Still a price that leads to losing money but certainly going in the right direction at a rapid rate.

The wizards who play with lean hog futures see it different. Since April’s June high of 91¢ lb. the June futures closed at 83¢ lb. last Friday. Bizarre. Cash hogs now almost 88¢ lb. while the wizards think June will be 83¢ lb. The trajectory of cash hogs is higher. We are not sure if ever June cash hogs ended lower than mid May’s prices.

The Wizard’s first rule: People are stupid. – Terry Goodkind

Observations

U.S. Pork Exports continue to run higher at 36,000 Tonnes a week compared to 30,000. The extra 6,000 Tonnes is about equivalent to 100,000 extra hogs gone from domestic market.

We all see the Corn – Soybean price declining. A welcome sign of relief for a beleaguered swine industry. U.S. average Corn price per bushel last Friday $5.88. It was $6.85 in April. A decline of almost $1.00 a bushel cutting cost of production of a hog by $10 per head. September Corn Futures closed Friday at $4.94 bushel, reflecting the good start to U.S. planting season, plentiful Brazil crop and low corn exports. China continues to cancel Corn orders. Maybe you don’t need Corn for a decimated hog herd from ASF disease. Soybean Meal has also declined October $380 ton. Down from the high of this year of $438 ton in March.

U.S. hog slaughter last week 2,408,00 the same as last year. It appears to us U.S. hog weights are declining rapidly as packers chase hogs to maintain plant capacity. Last Thursday the National Daily Direct Slaughter of 235,470 head average 281.43 lbs. It hasn’t been hot, so we don’t think these weights which are low for May are heat affected. Where are we going to end up when we get hot weather? Lower weights for sure? Lower hog numbers to slaughter? We expect both. Dynamics to push hog price higher. Always have – Always will.

Prop 12 – lots of scrambling as industry sorts out next moves. What is supply of Prop 12 pigs? That’s the big question. Not sure anybody really knows.

Prop 12 – it’s a loss in our mind for our industry but a win for Genesus. The Genesus female handles group pen gestation in our opinion better than all our competitors with superior leg and feet structure and a temperament conducive to mixing in pens. Our sow mortality and attrition are significantly lower than our competitors and in Prop 12 pens the difference becomes even greater.

We understand that the National Pork Board has done substantial studies on pork demand. We are glad they have. Not sure anybody hears much about this effort. We understand their surveys say Taste is the main driver for consumers. Not a surprise. Maybe we should do something about it. Our industry is languishing with no movement higher in per capita consumption for a generation. This while total meat consumption has increased 20% per capita. We are losing money as an industry. Selling the same crap isn’t working.

Taste is combination of marbling, juiciness and texture. Ask yourself, are you proud of the taste of the pork you produce? Do you order Beef when you are at a restaurant?

European hog prices near record highs – prices on lower supply supporting U.S. pork export increase.

Feed prices declining if cost of production could decrease $20 per head plus this fall from April costs.

Genesus China team just participated in Trade Show in Chengdu, China. The stories of herd liquidation from ASF are rampant. The liquidation will lead to rapid price increase in early summer. China is the world’s largest importer of Pork will need more Pork.

From industry info we believe that the U.S. will liquidate 300,000 sows plus over the coming months. This will cut production significantly. Higher prices will reflect the lower supply late fall into 2024.

The surest cure to low prices is low prices – Hogs

The surest cure to high prices is high prices – Corn

Editor’s note: Katerina Kolemishevska is Director of Policy Development, Canadian Pork Council (CPC). She can be contacted at kolemishevska@cpc-ccp.com.

The federal government’s sustainability push for agriculture is not bad, but it misses the target when it comes to convincing producers, who are the ones it impacts most.

Earlier this spring, the federal government published a discussion paper covering its ‘Sustainable Agriculture Strategy,’ which describes a proposed approach for improving sustainable agriculture practices in Canada.

The discussion paper is part of a larger government initiative to build a national plan for sustainable agriculture, which will establish a unified direction for collective action to improve long-term environmental performance in the sector, support producers’ livelihoods and promote the Canadian agriculture industry’s business competitiveness.

Responding to environmental problems and catalyzing the solutions into profitable and sustainable production practices can be challenging. There are many barriers to reaching sustainability, not only at the farm level, but also within the value chain. In most cases, these new practices would require significant changes in how we produce and consume our products.

One of the biggest challenges to transitioning is the economic pressure and the high cost of implementing sustainable practices. The pork industry is subject to a great deal of volatility, with a lot of attention on profit margins, making it difficult for producers to invest in new technologies or methods that do not guarantee financial returns.

With primary production comes supply chain incompatibility. The pork industry is part of a complex network of several inter-related operations, ranging from crop production, transportation, processing and retail. Changes in one area could have unintended effects in another. Without a whole-system approach, it would be impossible to reach the goals currently outlined in the government’s sustainability strategy.

Lack of data fuels speculation over facts

The Canadian Pork Council (CPC) is currently surveying producers about their use of sustainable practices, to benchmark where we are and consider where we can get to.

The lack of data is a considerable challenge holding back the necessary funding allocation and investments into many of the solutions that would make agriculture more environmentally friendly. Evaluating the success of sustainable agriculture methods and analyzing their actual benefits to the environment cannot be achieved without accurate and reliable data. What’s more, producers may be unwilling to implement sustainable methods in the absence of credible data demonstrating their advantages.

In addition to data, the lack of uniformity in environmental performance indicators can lead to confusion among producers and consumers, making evaluating the sustainability of different practices challenging. Consequently, it can foster a lack of trust in sustainable initiatives and hinder their effectiveness in promoting sustainable practices. Achieving sustainability requires sound collaboration and coordination among producers, governments, different agri-food sectors, researchers and consumers. Yet, there seems to be a lack of cooperation among these stakeholders, making developing and implementing effective policies and practices difficult.

Benefits of sustainability could eventually be realized

Despite the challenges, there are some benefits to embracing sustainable agriculture practices. New common knowledge is evolving, promising the ultimate synthesis of environmental and economic objectives. With this new way of thinking, both industry and the planet may prevail. Being ecologically responsible is no longer a cost of doing business; rather, it is a driver of innovation, an opener of market expansion and a generator of growth.

Sustainable agriculture practices can provide several benefits for producers, including increased profitability and fewer inputs. The main bonus is improved value. For example, feed, manure and soil management practices can result in lower costs and higher yields, leading to increased profitability. Additionally, practices such as water-efficient irrigation and renewable energy sources can help reduce utility costs, resulting in lower operating expenses.

As the world shifts towards eco-conscious living, this means creating and accessing new markets. Currently, there is a lack of access to markets that reward sustainable practices. Many traditional markets do not offer a premium for food produced sustainably, making it difficult for producers to rationalize and recover the associated expenses.

However, consumers are becoming more interested in pork that is produced sustainably, and producers who demonstrate sustainable methods may gain access to new markets and better pricing for their products. Various countries and regions are already vigorously promoting products with claims relating to reduced carbon footprints, organic and antibiotic-free production, and fair-trade practices. These products are often sold at a premium, providing an opportunity for producers to earn more money when selling their pigs to processors who make these claims – hypothetically, at least.

When producers are paid better for their pigs, this encourages and enables them to cover the costs of becoming more sustainable while also supporting the trade ambitions of their processing customers, who are increasingly mindful of the requirements for entering markets that appreciate sustainable production. More importantly, sustainability can help producers improve their resilience to climate change and other environmental challenges like drought, floods and pests. Managing weather risks can reduce crop failure, animal mortality and disease incursions, resulting in an improved financial situation.

Overall, by conserving natural resources and decreasing environmental effects, sustainable practices can help assure the long-term viability of pork production in Canada. This can help producers continue to grow and earn a living from their land for future generations.

Major barriers to success still exist

Transitioning to sustainable practices, in some cases, means adopting expensive, complex technologies. Combined heat and power (CHP) units for barns are one example. Producers may require additional support to summit the steep learning curve.

Transitioning to sustainable pork production practices will be a complex process that requires addressing several uncomfortable realities.

Most importantly, producers need access to the necessary knowledge and skills to support a successful transition to best practices. This includes training on sustainable management of feed, water, manure and soil; the environmental impact of pig farms; and the benefits and challenges of transitioning.

With skill-building comes the potential of co-benefits. Measures are often adopted mainly for reasons other than mitigating greenhouse gas (GHG) emission that yield purely win-win outcomes, also known as ’trade-offs.’ Key potentials for trade-offs in the area of manure include limiting fertilizer use, improving soil resilience, and the creation of bioenergy. As such, the trade-off is lower costs while also reducing GHG emissions.

On top of knowledge and skills, producers will require technical means such as adequate equipment, technologies and infrastructure to implement best practices. Some of these may require adjustments to existing systems or the adoption of new ones, such as irrigation, manure spreading or renovations to animal housing.

Beyond the challenges inherent to producer education and retrofitting farms, the steepest obstacle is that environmental stewardship and sustainability can be expensive, going well beyond what many producers can afford, at present.

Producers need sufficient access to loan financing and funding incentives to make the transition possible. In some cases, there may be a need for alternative business models or markets to support sustainable practices, backed by policies that have tangible outcomes for producers. The government needs to put more work into this area to provide a level playing field for producers. This includes measures that support producer-led research and development that fits with unique Canadian pork production conditions, including weather and other factors.

Yet again, we should not forget the crucial component, which is market demand. There needs to be sufficient demand for sustainably produced pork products to provide a market for producers who adopt sustainable practices. This requires raising awareness among consumers about how the pork industry has progressed, which should encourage producers to transition.

Transition requires small steps, not great leaps

Radical, sweeping decisions can have unintended consequences for agriculture. Too much change too quickly could put farmers out-of-business, which is unsustainable regardless of environmental best practices.

Considering everything that is influencing sustainable pork production, it provides the pork industry, including producers, with both challenges and opportunities.

Nonetheless, in the long run, the benefits far outweigh any concerns or inconveniences connected with such challenges. Transformational change toward sustainable pathways requires more than simply scaling up sustainability practices; it requires addressing the collaborative implementation of priority interventions and targeting key points, in hopes of linking existing social, economic and environmental systems.

The federal government’s proposed Sustainable Agriculture Strategy has brought together decision-makers, industry partners, producers, researchers and members of the public to discuss how to bring about pathways to sustainability. Through this initiative, it is imperative that the beliefs behind sustainability are backed up with appropriate support for farmers, which will be key to getting them on board in principle and in practice.

Editor’s note: Karl De Ridder is a swine technician with Cargill Animal Nutrition. He can be contacted at karl_de_ridder@cargill.com.

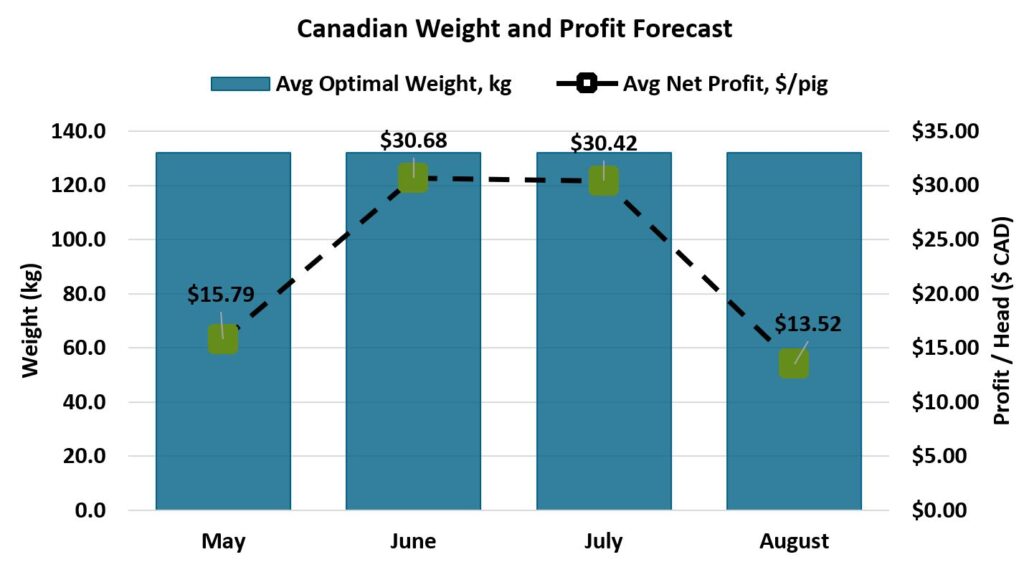

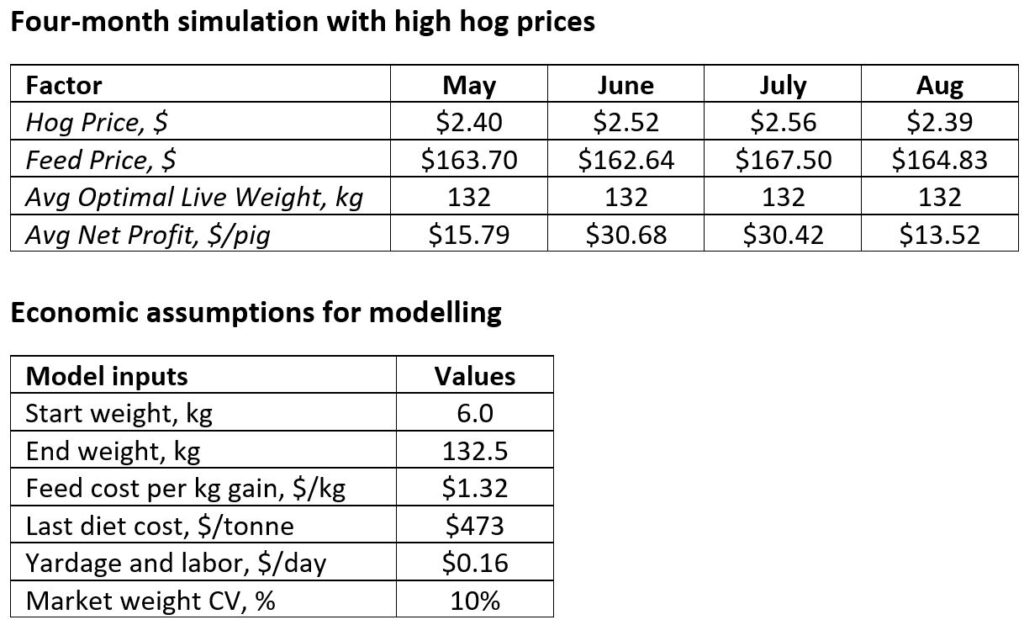

Figure 1Figure 2

The checklist for pork producers on a daily basis is daunting enough before you even take market conditions and production constraints into account. Given the volatile nature of the industry, finding ways to optimize your profitability is no easy feat. A combination of strategic planning, market analysis and effective management practices is crucial.

Optimizing profits starts by connecting ingredient and diet decisions with marketing strategies. Clearly defined end goals are key to identifying those strategies. There are tools and a service in the marketplace that help you make the best decision when it counts, by using your data in real-time to better understand current and future economic considerations, determine optimum weights and first-cut forecasting, and scenario planning for your what-ifs.

Forecasting optimum weights to ship the pigs is one way Cargill’s Producer Profitability tool and exclusively tailored advice from experts can help producers grab a few extra dollars, especially as summer months draw near.

Our four-month forecast (Figure 1) and associated variables (Figure 2) predict increasing market weights by two kilograms will maximize profits for producers from May through August. With a natural reduction in weight gain during summer months of about four-and-a-half kilograms per pig, producers really need to be picking up an extra six-and-a-half kilograms.

Summer strategies shouldn’t be decided on during the summer; now is the time to start talking about which diet strategies will be best for your operation. Digital tools, such as Producer Profitability, are at your fingertips to help you confidently capture every dollar. In an unpredictable industry where margins are narrow, every penny left in your pocket counts. Because nothing else matters, at the end of the day, if you aren’t optimizing profits.

Pork Commentary Jim Long President – CEO Genesus Inc. May 17, 2023

Last week the U.S. Supreme Court ruled that California’s Proposition 12 can proceed. The law means in simple terms sows must be in gestation pens at 24 sq. ft. to have their fresh Pork sold in California.

The ruling is not a win for a Pork Industry facing financial headwinds.

There has already been sow barns built or renovated to meet the Prop 12 rules. Estimates range from 350 – 500,000 sow spaces. We don’t know if this will meet California’s Pork demand.

One of the challenges of Prop 12 is not only the cost of building and equipment but the lower production results due to lower litter size, farrowing rates and the higher sow mortality. There are premiums being offered for Prop 12 pigs which are necessary to cover the increased production costs.

In a selfish note. Genesus sows with a combination of structure and temperament have an edge versus competitors in pen gestation i.e., Prop 12 barns.

Packer Demand

This past week we had several conversations with producers telling us Packers were calling looking for hogs. This is a good sign of increased demand. One producer told us a Packer called they never do business with looking for hogs. My Father used to say, “Who’s calling whom.” He always equated it to a reflection of market direction.

Corn

We all can see corn prices have fallen, at the rate we are going down. Corn under $5 bushel will be happening. Lots of corn in Brazil, U.S. crop getting planted in timely manner with U.S. corn exports continuing to languish (-36% ytd.). Lower feed costs would be beneficial to the Pork Industry.

Liquidation

It appears to be a reality that major sow liquidation is underway. The low price of cull sows indicates their abundance. We expect in U.S. 300,000 sows will be gone. If correct decreasing U.S. hog production by about 6 million head a year.

We expect liquidation in Canada of 50,000 sows or about 1 million pigs disappearing a year.

All supportive for higher hog prices in fourth quarter into 2024.

If Misery Loves Company Department

Reports from China indicates 17 of the 21 listed public companies lost money in the first quarter due to pig production. Wens 2.7 billion RMB ($385 million). New Hope 1.7 billion RMB ($242 million). Muyuan 1.2 billion RMB ($171 million). Zhengbang 1.2 billion RMB ($171 million). The top three companies have losses of at least 400 RMB per head ($57 per head). Some of the main companies have announced plans to decrease production a combined 6 – 9 million pigs per year (similar to what we expect in USA).

If we assume $57 is an average loss per head for the whole industry. China markets about 12 million hogs per week the loss would be $684 million per week. No doubt there is herd liquidation. The loses in China are due to the lower hog price driven by large volumes of ASF infected pigs dumped into market (all weights get sent). We expect sometime in June – July China’s price will move higher as fewer hogs come to market. China is the world’s largest importer of Pork. Less Pork in China will lead to more imports.

Pork Demand

We have been writing about our concern with Pork Demand and prices. A reader sent us the picture below of Ham in a Hy-Vee grocery store. 49¢ lb! Probably at 49¢ it is getting to Dog Food price. We have a real problem in this industry when we are using that as a benchmark.

In our opinion one of the best brands in the U.S. Pork industry is Johnsonville. They make only sausages and only high-quality sausages. They sell for more than other sausages each and every day. They have advertised and developed a brand and backed it up with consistent and predictable quality. In stores Johnsonville sausage is $4.99 lb. – the ham was 49¢ lb? Johnsonville knows what matters BIG TASTE and they advertise to deliver the message.

Johnsonville has got it. TASTE. When are we as an industry make the changes to mirror what Johnsonville has realized and profited from make a brand and product that consumers want and pay for.

Ham at a Hy-Vee grocery store being sold for 49¢ lb.

Pork Commentary Jim Long President – CEO Genesus Inc. May 8, 2023

The U.S. industry continues to struggle. Hog prices below cost of production is putting a major financial stress on much of the Pork sector. There will be significantly fewer pigs year over year by the end of 2023 and even fewer in 2024.

Our Observations

Major sow liquidation is underway which will decrease the U.S. sow herd by 4% – 200,000 – 250,000 sows in our opinion. A reflection of the economic conditions but also the ongoing health issue problems that over and over lead to decreased production and spikes cost of production.

There is a challenge to get sows marketed currently a combination of large numbers and pork market conditions with sow mortality industrywide of 14 -15% slowed gilt placement due to market in itself will cut the sow herd.

We have seen many hog price debacles in the time we have been in business. The scenario today seems somewhat different. Why?

In other price collapses we dealt usually with spiked hog production. Year to date the U.S. has produced 1% more Pork than a year ago. With Beef production down 4.9% year to date total Red Meat production is down 2.0%. Certainly not significantly more Pork and a lot less Beef.

Year to date U.S. Pork exports is up 7% with exports appearing to clearly be climbing. Latest weekly U.S. Pork export sales 49,000 MT, the week before 54,000 MT. Clearly higher than the 31,000 MT average year to date. Greater amounts of Pork exported obviously shorts domestic market and will be supportive for price.

Spain, a major U.S. pork competitor exported 7.4% less Pork year over year in the first quarter. Spain hog price is almost double the U.S. price. Not only has Spain got higher prices but also less Pork to supply (that’s why the hog price is higher). We expect continued increased export sales from the U.S. as arbitrage takes hold.

China seems to be importing more Pork. Year to date U.S. to China exports are up 27%. China has announced they are going to purchase for Government Pork Reserves. Pushing up demand. We expect China’s hog price will take off sometime in June-July as supply tightens from liquidation that has happened due to losing economics and African Swine Fever – PED – PRRS. When that happens there will be even greater amounts of Pork imported. China is the largest importer of Pork globally.

Weights seem to be declining Iowa – S. Minnesota 2.6 lbs. lower than a year ago. We wonder why Saturday slaughter numbers were 136,000 last week. Seems to us that could indicate some sort of good demand that Packers are seeing. We are entering Spring – Summer when hog slaughter declines seasonally significantly.

Friday Beef cut-outs $309.19 lb. Pork cut-outs 81.87¢ lb. A huge difference. You would think that this price spread will narrow. We don’t expect Beef to decline as Beef supply stays low. Pork should go up.

The price spread between Beef and Pork as we all know is mainly due to the consumers preference for the taste of Beef. As we have written about regularly until we improve taste of Pork we will be challenged to compete with Beef.

Summary

There are some factors that in our opinion could really trigger a rapid hog price increase.

Increasing Pork export sales – Europe record hog prices – Arbitrage.

The price spread between Beef and Pork leading to featuring of Pork in domestic retail increasing demand.

Long term price

Ongoing sow herd liquidation will cut Pork supply in late 2023 into 2024.

We expect China supply cut will increase their pork imports from mid 2023 to 2024.

Coronation King Charles III

Last Saturday Charles III was crowned King. We understand there was a lunch at Buckingham Palace and a formal dinner at Windsor Castle.

Maybe you remember our report from a few months ago where British producer Jimmy Butler’s Blythburgh Free Range Pork was supplying Genesus Jersey Red Duroc bred to Genesus Females premium Pork to both Buckingham Palace and Windsor Castle. We don’t know if Genesus Pork was served at the Coronation events.

It appears Genesus Pork “Is fit for a King.” It’s our position that the excellent tasting attributes of Genesus should also be available to each and every consumer. Taste drives demand.

Jim Long of Genesus and Jimmy Butler of Blythburgh Free Range Pork at an outdoor free-range unit

Pork Commentary Jim Long President-CEO Genesus Inc. May 1, 2023

Last week there seemed to be daily news tied to the dire situation in much of the hog sector. Hope isn’t a business plan but at the end of the day, all you need is Hope and Strength. Hope that it will get better and the strength to hold on until it does.

Last week rumor of a major company planning on immediate major sow liquidation of 10’s of thousands of sows.

Leadership coming and going in several major pork-producing companies. Some packing company layoffs announced.

Chapter 11 bankruptcy for the HyLife Foods Packing Company USA related to Windom, Minnesota packing plant.

In Canada, further confirmation of packing house closing, and potential voluntary sow buyout.

Reports of major sow liquidation in Mexico.

Losses in the industry continue to mount not only for producers but also packers. If you are a Packer and own hogs, it’s a double loss.

Not exactly a scenario of positivity, is it?

One positive is June lean hogs gained $5.63 last week. Pork cut-outs closed 81.32¢ Friday. Better but losses continue.

U.S. July Corn closed down 30¢ bushel on the week. Corn in parts of Brazil under $5 bushel putting pressure on U.S. corn exports. Mississippi River flooding will further slow U.S. corn exports as barge traffic slowed or stopped.

China canceled some U.S. corn orders. Some think to buy Brazil corn. Also, might be from decreased demand from the African Swine Fever breaks in China. Dead pigs don’t need feed (corn).

If misery loves company, we only need to look at China’s hog industry. Not only being hit by African Swine Fever issues in a major way but also suffering financial losses. A reflection of this is the financial results of publicly traded swine companies in Quarter 1. Wens lost 2.7 billion RMB ($390 million). New Hope lost 1.7 billion RMB ($246 million). Losses per head are estimated from 169 RMB ($25) to 262 RMB ($40 per head). Industry-wide losses are over $500 million a week. We expect as the liquidation of the pigs sent to market due to ASF slows, China’s hog price will roar higher.

U.S. weekly pork export sales were 54,000 metric tonnes a week ago (exports have been 30,000 YTD a week). The highest week this year. With Europe’s hog price almost double the U.S., it only can be expected that Arbitrage will lead to increased U.S. export sales at the expense of Europe’s. 54,000 tonnes is a strong indicator that Arbitrage is beginning. Any extra pork that leaves the U.S. strengthens U.S. hog prices.

Watching daily slaughter weights, it appears to us weights are coming down. Maybe the first indicator of lower hog numbers as packers pull hogs ahead.

Europe’s hog price is at record highs i.e., Spain at $1.02 U.S. lb. (2.025 Euros/kg). A 280 lb. market hog $282. Makes exports hard to compete with the U.S.

Demand – Sustainability

In the last two weeks, we have written about Pork Demand and the Sustainability of our industry. The feedback we got was large. It seems many see what the problem is – Taste. Consumers will pay almost four times more for Beef than Pork as reflected in U.S. cut-outs. Last Friday Choice Beef $3.11 lb. Pork 81.32¢ lb. As we wrote last week if we got half of the Beef cut-outs i.e., $1.55 lb. we all would be doing cartwheels and congratulating ourselves on our business brilliance. Instead, we are sucking air.

We are challenging the Pork Board to use Checkoff money (i.e., $70 million a year) to push for a better-tasting product. Create demand. If all Americans ate pork one more time a month, it’s equivalent to 7 million more market hogs. Demand drives price. Taste is not a niche but an industry-wide necessity.

The sustainability of our industry won’t be decided by Pork Board bureaucrats discussing animal welfare, the environment, etc. Sustainability isn’t Packers going Chapter 11. It isn’t the industry losing up to $100 million a week. In our opinion, we can’t continue on the path we have been on. It has not been working. We need to have a Taste Revolution to drive demand and secure profitability.Many of life’s failures are people who did not realize how close they were to success when they gave up. – Thomas Edison

Most food categories at retail in Canada have shot up over the past two years. Pork is a notable exception, but many of the same challenges that exist with other products impact the pork value chain just the same.

Canadian consumers are demanding an explanation for the sticker shock they are experiencing at the grocery store.

In July 2022, general inflation in Canada was close to eight per cent – a four-decade high – cooling down to below five per cent in April 2023 and expected to move lower yet heading into 2024. Food price inflation, however, has continued to hover around 10 per cent for about a year. Even as general inflation eases, food price inflation does not appear to have followed suit.

Coincidentally, in the past year, profit margins for Canada’s major grocers were upwards of 10 per cent. Meanwhile, on the side of food production and processing, higher input costs, lower commodity prices and other factors have spelled negative margins for hog farmers and meatpackers.

When it comes to explaining why Canadians’ grocery bills are so steep, little of substance has been provided by those who know why or have the ability to do something about it. Grocery executives continue to pay themselves generously while shoppers watch their weekly bills get bigger. While it is impossible to offer a comprehensive explanation for all food categories, which stakeholders are making the most off struggling consumers?

Producers, processors and retailers are all within their rights to concern themselves with their bottom lines. Capitalism, at the end of the day, still reigns supreme in all parts of the value chain, just as in most sectors of our economy. While profit motive undoubtedly belongs in the equation, it would be inaccurate to suggest all stakeholders have been raking in the dough. The closer you look, the more obvious it becomes.

In the Canadian pork value chain, for years, producers and now processors have seemed to absorb a greater proportion of the mounting costs that retailers are able to recoup simply by charging more for their goods. As Canada’s grocery sector has steadily moved in the direction of oligopoly – with fewer and fewer legitimate choices – has big business finally reached a tipping point when it comes to providing essential food products and services, fairly, for Canadians?

As time goes on, consumers are rapidly losing faith in the belief that the cutthroat practices of large-scale supermarkets are leading to greater purchasing power for them. Certainly, the data – or lack of transparency around it – is making the disparity plain to see.

Grocers garner harsh criticism

Grocery chain bosses were called upon to justify their business practices against growing accusations of profiteering amid soaring food price inflation, sometimes called ‘greedflation.’

Starting from the most visible part of the agri-food value chain, grocery stores were once trusted as ethical, people-minded enterprises that play a crucial role in any community. While at least part of that assumption remains true, skepticism has become a popular perspective.

When COVID-19 struck in early 2020, short-term losses for grocers quickly mounted, in response to gathering restrictions imposed by government and a need for physical distancing, masking and sanitation. As grocery employees were considered essential frontline works, several grocers began offering ‘hero pay’ to recognize and retain employees. At the time, it was surmised these necessary adaptations could account for immediate food price increases. While reasonable-sounding, pandemic living eventually became the norm. With restrictions already well-established, employee incentives were taken away, but prices kept climbing.

Executives from Canada’s three largest grocers – Loblaw Companies Ltd., Empire Company Ltd. and Metro Inc. – were summoned before the House of Commons Standing Committee on Agriculture and Agri-Food in early March to clarify the connection between food prices and corporate profits.

Those questioned included Galen Weston Jr., Chairman & President, Loblaw, with more than 2,400 stores in all provinces, including Real Canadian Superstore, No Frills, Zehrs and Provigo; Michael Medline, President & CEO, Empire, with more than 1,500 stores in all provinces, including Sobeys, Canada Safeway, Thrifty Foods and Longo’s; and Eric La Flèche, President & CEO, Metro, with nearly 1,000 namesake, Super-C, Food Basics and Marché Ami stores in Quebec and Ontario.

The committee wanted to find out whether current grocery prices equitably reflect the supply chain challenges that have cropped up since the start of COVID-19, when inflation and grocery revenue began to grow in step with each other.

When asked about his company, Weston used the example of a $25 grocery spend and suggested that $24 of that total amount represents accumulated supply costs, while only $1 represents profit for Loblaw.

“If we didn’t raise retail prices as costs went up, the companies that we operate would disappear almost instantly,” he said. “A hundred per cent of the profit in the food industry could go into lower food prices, and the price of the basket for that customer would still be 24 dollars.”

When pressed further to elaborate on his reasoning, Weston doubled down on his analogy, effectively silencing any meaningful inquiry.

“This one dollar of the 25 dollars is what we’re focused on, and all of this time, effort and exposition is focused on that amount,” he said. “No matter what is there – and there isn’t anything of significance there – that isn’t going to change the cost of food.”

When asked about Canada’s incoming grocery code of conduct – which is expected to be in place soon – Weston insisted Loblaw already negotiates with suppliers cooperatively, despite instances of “bad judgment on both sides,” referring to his company and manufacturers.

“We believe that we do business in a fair and transparent way 99 per cent of the time… It’s really important that any code or any set of practices that we engage in are properly balanced,” he said.

That one per cent discrepancy may have been a subtle reference to an earlier controversy that many Canadians will remember: in 2015, Loblaw sister company Weston Foods came under investigation by the Competition Bureau of Canada after being accused of colluding with Canada Bread as part of a price-fixing scheme that artificially inflated bread prices at retail for more than a decade. While the allegations were never proven in court, in 2018, Loblaw reacted by offering $25 gift cards for Canadians to use in its stores – a fitting and precedent-setting amount, foreshadowing the latest debacle.

In early April, just a month after the parliamentary hearing, Loblaw announced that Weston would receive a pay raise this year, based on last year’s stellar performance. Not long after, the company announced it would commit $2 billion to open 38 new stores and renovate 600 others. Certainly, expansion, not stability, remains the dominant mindset for Loblaw, as the company battles with only a handful of others like Empire and Metro – not to mention Costco Canada and Walmart – for highly coveted market share.

Suppliers squashed in several ways

Canada’s meatpackers have faced an ongoing list of problems in recent years, most of which are beyond their control. Others stem from unfortunate investments into expanding processing capacity or experimenting with non-meat products.

While grocers continue to triumph, in meatpacking, the situation is far less encouraging for business.

When it comes to pork processing, profits for meatpackers were healthy and improving in the years immediately preceding COVID-19, but since 2021, that relationship has worsened from growth, to stagnation, to deficit.

Factors such as reduced access to high-volume pork markets like China, coupled with difficulties around finding workers, have hammered at the earnings of Canada’s largest pork processors, including Maple Leaf Foods, Olymel and HyLife.

Maple Leaf Foods reported its financials for the fourth quarter of 2022 in early March, including a loss of more than $40 million.

A cyber-attack led the list of problems, along with disruptions to the movement of pork and routinely poorly performing plant-based protein, from which the company has continued to lose money since it began investing in meat alternatives in 2017.

However, between 2021 and 2022, Maple Leaf’s sales increased from $4.5 billion to $4.7 billion total. Adjusted earnings for the company’s real meat category, while consistently positive, dipped from $527 million to $379 million, or by 28 per cent. Plant-based proteins managed to lose 17 per cent less, at only $105 million in the red, compared to $127 million the year prior.

Olymel, on the other hand, has faced a protracted series of disappointments in the past year. In November, the company announced the closure of its slaughter facility in St. Hyacinthe, Quebec. Then, in early February, the company closed two further processing plants in Blaineville and Laval, followed by an additional slaughter facility in Vallée-Jonction, in mid-April.

According to the company, “the decision was necessary to stop losses in the fresh pork sector, which have amounted to more than $400 million over the past two years and are jeopardizing the entire company’s profitability.”

In 2019, Olymel acquired rival brand F. Ménard for a handsome, undisclosed amount, consolidating a good chunk of the province’s hog production, integrated with the company’s existing pork processing capacities and related functions, like feed milling and trucking. It was expected that this decision would eventually pay off, but the unfortunate timing, occurring just prior to COVID-19, has proven daunting.

For HyLife, cracks have begun to show more recently, in early April, as the company has struggled to sell off its slaughter facility in Windom, Minnesota, originally purchased in 2020, right as COVID-19 had taken hold. The plant was acquired to increase overall capacity, in addition to HyLife’s main plant in Neepawa, Manitoba.

A common domestic theme for all meatpackers has been a lengthy list of labour concerns. While HyLife never experienced any plant closures due to workers being infected with COVID-19, Maple Leaf’s plant in Brandon, Manitoba; Olymel’s plant in Red Deer, Alberta; and Conestoga Meats’ producer-owned plant in Breslau, Ontario were all shuttered for several weeks due to outbreaks in 2020 and 2021, resulting in disruptions to the supply of pigs and pork.

During the plant outbreaks, at least one worker died as a direct result of contracting COVID-19, causing a news media stir and adding fuel to the fire for critics of the meat industry. On top of that, as temporary and permanent plant closures across the country have resulted in the laying-off of workers, labour rights advocates and unions have pressured governments to adopt stricter measures to protect workers. While the desire to support workers is entirely justified, there is no question the circumstances surrounding those outcries have had the effect of gradually chipping away at processor margins.

Given the examples of Maple Leaf, Olymel and HyLife, it is clear food suppliers have been under the gun more intensely in recent years. In some cases, companies’ misfortunes have resulted from untimely or misguided business decisions, but in other cases, uncontrollable pandemic-related factors have taken a toll that has been felt at both ends of the value chain.

Pig and pork production absorb heavy blows

Retailers have been taking an increasingly larger share of pork value in the past five decades, while the gap between producers and processors remains relatively consistent, by comparison.

Hogs raised by Canadian producers – processed at facilities like those owned by Maple Leaf Foods, Olymel, HyLife and a few others – are regulated by the Canadian Food Inspection Agency (CFIA), representing upwards of 99 per cent of total production across the country, though this does not translate to the volume that is sold in Canadian grocery stores, which can include cheaper pork of foreign origin.

Hogs procured by CFIA-inspected processors are priced according to market formulas derived from mandatory, daily reports compiled by the U.S. Department of Agriculture (USDA), which reflects aggregated prices paid by processors to producers in the U.S. In Canada, no such reporting mechanism exists, which has been an ongoing problem that provincial pork producer organizations and the Canadian Pork Council (CPC) have been trying to address for years. Political buy-in has been lukewarm, at best.

Between 2000 and 2020, it is estimated that Canada lost more than three-quarters of all independent hog producers, while consistently growing the size of the country’s total pig herd. This phenomenon is not due to a declining interest in raising pigs or selling pork, but profitability barriers that have made modern agriculture inaccessible without sufficient capital. Partly because of this, one approach by processors has been to vertically integrate their hog supplies by either owning barns outright or independently contracting producers as finishers for more of the hogs that end up at their plants.

This suggests that, while we have fewer farmers making a living off commercial hog production, those few have expanded their operations to make up the difference, as global demand for protein continues its bullish trajectory. As the number of hogs produced has levelled off in recent years, and the number of producers continues to drop, it is easy to speculate as to why, given the situation at-hand.

Since the 1970s, data gathered from the USDA suggests the share of value between producers, processors and retailers has not stayed proportional. Extrapolating this data for a Canadian context is not a perfect comparison, but given the inter-connection between our national industries, the relationship is about as close as we can get without better, currently non-existent data.

Canadian market hogs are priced using processor-specific formulas that reference the USDA’s information, as a starting point. From there, hogs are measured against a ‘grid’ that includes a range of weights falling below or above an ideal target, which sets the starting price. Then, carcasses are assessed for indicators of quality – like fat marbling, loin depth and colour – which may be paid out in the form of premiums and bonuses defined by a producer’s contract.

To evaluate hog prices in a general sense, market analysts use a standardized 100-kilogram ‘dressed’ carcass, referring to one that has been slaughtered and has had most of its non-meat features removed. Considering the financial share of that carcass, one that fetches a producer $200 can be sold by a processor for roughly $300 in profit once broken down into ‘primals,’ or large, basic cuts. Most primals are sold to wholesalers internationally or domestically, to perform further processing in any number of ways.

Fresh or frozen cuts like loin chops, racks of ribs, belly portions and shoulder roasts – along with cured products like bacon, deli meats and sausages – are among some of the many options Canadian consumers have when it comes to purchasing pork in-store. While detailed sales data for these items is not publicly known, even taking a low-end estimate of $8 per kilogram – the price of ground pork at Real Canadian Superstore, as of early 2023 – that would mean the full value of the meat from a hog carcass approaches $800 at retail, which is, conservatively, about four times what a producer earns and at least twice what a processor earns.

While the numbers cited here cannot be exact and are highly variable, a picture of proportionality begins to emerge: producers and processors, together, take home only a meagre slice of the total value of the pig, most of which belongs to the retailer and its middlemen. Granted, these middlemen represent additional input costs for retailers, on top of losses attributed to meat that goes unpurchased and is wasted. However, until retailers choose to shed a brighter light on the breakdown of their costs, as a way to rationalize what they charge and justify their margins, consumers and the rest of the pork value chain are left guessing.

Farmers bear the brunt of the burden

The pork value chain can be very complex on certain levels, but it starts with the farm and producers who are committed to animal care, food safety and traceability, backed by quality assurance programs that are validated and audited by veterinary experts.

Consider what it takes to get the pig from farm to fork: from ‘farrowing,’ or birth, the pig is raised to market weight at six-months-old, then hauled to the processing plant, where the next steps take a mere matter of days. From there, its outputs are sold and shipped all around the world to end users who may get weeks or months of shelf life out of the product, depending on how it is prepared or stored.

All in all, while processing and retail are indispensable parts of adding value to the hog carcass, most of the time commitment – and much of the up-front risk – lies with the producer. Producers, being at the beginning of the value chain, have little to no recourse when it comes to affecting the prices paid for their pigs, while facing the same unstable market conditions as processors, with none of the mark-up ability of retailers.

While input costs have increased across the board throughout agri-food, livestock feed, energy costs and insurance rates have gone up faster than hog prices. When looking to re-invest into a hog operation, including modernizing barns for eco-efficiency and animal welfare standards, producers have suffered, as the confidence of lenders has eroded. On top of that, if a producer underperforms in another area of his total farm operation, such as reduced crop yields during an off-year, government-funded business risk management (BRM) programs are often insufficient to balance out total losses.

With everything considered, it is hardly short of miraculous that many of Canada’s food producers are able to stay afloat at all.

Market downturns make it tougher

The predictable yearly ebb and flow of pig prices – lower in winter, higher in summer – experienced a particularly tragic anomaly in mid-2020, as African Swine Fever (ASF) and COVID-19 ravaged the industry for months.

Market conditions for pigs and pork took a sharp turn, starting in late 2018, with the outbreak of African Swine Fever (ASF) in China. Almost overnight, pork values for processors jumped dramatically as China looked to fill the void left by widespread culling of animals on its farms, which led to a situation of unexpected low supply but predictable high demand for protein, with pork being the cultural preference even among other options like beef, chicken and seafood.

Shortly after ASF hit China, hog prices in western Canada were around $150 per hog, with cost of production estimated at around $180, signifying a $30 loss. This period continued until 2020, when COVID-19 struck. While summertime usually spells the highest hog prices, they sunk to around $140 per hog, as costs approached $200. Producers were then losing more than $50 per hog, on shipments of about 200 hogs per week, for many weeks of that year.

Recognizing the severity of what was happening, western Canadian producer organizations – B.C. Pork, Alberta Pork, Sask Pork and Manitoba Pork – approached processors with a humble request to work toward bringing about some relief in their pricing structures. Olymel made favourable adjustments to its base pricing and bonuses, while Maple Leaf introduced a pricing floor, which temporarily kept base prices from falling too far, too fast. Separate from the producer organizations’ request, HyLife had recently introduced base pricing using cut-out (primal) values, rather than whole carcass values, which were lower. The net effect of all these changes was a small boost for producers. But, despite the efforts, which were appreciated, little could have prevented the damage that had already been done.

This situation ended up financially crippling many, as a result of that comparatively short period of market volatility alone. Some producers managed to limp through the most difficult parts, while others did what they could to escape the industry with as little collateral damage as possible.

While hog prices stabilized and became favourable through much of 2021 and 2022, costs kept climbing to historical highs. In good times, producers may have profited between $60 and $100 per hog for several weeks in the summer months of 2022, descending to break-even, at a low point, during this past winter. As of the first part of 2023, hog prices were sitting at $230 per hog, though future pricing estimates suggest this summer will be mediocre, if not outright negative. Compounding the problem, costs have yet to cool down, now upwards of $240 per hog.

It would seem that the roller coaster ride is set to continue, and for those who are unable to stomach the inevitable ups and downs, they may be looking to bow out. Should the number of active producers, once again, shrink faster than the reduced hog supply can be displaced, it will have a ripple effect on everyone, from processors and retailers, to consumers.

Producers and consumers deserve better

Despite the pork value chain’s internal struggles, for consumers, pork stands out as a candidate for being incredibly nutrient-dense and easy-to-prepare, along with being unusually affordable in the current high-price environment.

Retail pork prices by weight have actually declined year-over-year, making pork attractive relative to its red meat cousins, poultry and heavily promoted fake meat substitutes. Other categories of food – like produce, bakery and dairy goods – have increased.

And while the Canadian public should be encouraged to keep purchasing pork – undoubtedly, a mutual benefit for the consumer and industry alike – it may enhance their understanding if they took a deeper dive into the parts of the value chain that are less observable to the average person.

In the absence of clear answers to questions around food prices, and solutions to bring them closer to what is considered ‘fair,’ consumers will continue to eat. For the vast majority, that means frequenting grocery stores, often with few true options or cost savings to be had. Unfortunately for consumers, just like producers, most of the bargaining power does not belong to them.

At the same time, as pig prices fail to represent an equitable share of producers’ efforts, and as processors grapple with treacherous territory in the global pork marketplace, farmers and meatpackers will continue to deliver their products – feeding Canadians and the world. But for how long can it last in an economically sustainable fashion, under current constraints?

Consumers should not feel guilty about buying pork at discounted prices – hypothetically and unintentionally on the backs of producers – but they should keep searching for the reasons why grocery prices are the way they are, no matter the food item. Producers, too, will keep pressing.

Editor’s note: Dan Darling is President, Canadian Agri-Food Trade Alliance (CAFTA). For more information, contact Adam Taylor, Interim Executive Director, CAFTA at exec.dir@cafta.org.

Supply management of certain Canadian agricultural outputs is a given. But what about the 90 per cent of other commodities that rely on access to global markets?

Few pieces of legislation being considered by Canadian parliamentarians have the potential to jeopardize more sectors than they’re seeking to protect like Bill C-282, An Act to amend the Department of Foreign Affairs, Trade and Development Act (supply management).

In summary, the bill – put forth by the Bloc Québécois – would prevent Canada from ever contemplating concessions in sectors regulated through the system of supply management, specifically, dairy, eggs and poultry. As an organization representing the 90 per cent of producers, processors and agri-food exporters that rely on access to global markets, we believe this bill is ultimately unnecessary and runs counter to Canada’s broader economic interests.

First, this bill contradicts Canada’s long-standing trade policy objective of achieving comprehensive trade outcomes, as described by the Department of Foreign Affairs, Trade and Development Act.

Furthermore, tying the hands of trade negotiators before talks even begin will result in less ambitious pursuits across the board, as other countries will counter by excluding products or sectors from discussions where Canada has offensive interests.

This bill will also encourage other sectors to also seek exclusions from trade talks and will send the signal that protectionism is acceptable and indeed desirable – a public policy course that would be devastating for an export-dependent country like Canada.

Second, C-282 erodes Canada’s credibility as a leading voice for free and open trade. We shouldn’t kid ourselves; other countries are watching this legislation closely, and this bill’s passage will have immediate negative consequences as we fully expect many of our trading partners will respond by threatening to refuse to extend, review or modernize existing trade agreements. It would establish Canada as an undesirable trading partner and would limit our ability to even be invited to a seat at the table of various bilateral and multilateral negotiations. Perhaps most worrisome, this legislation contradicts Canada’s leadership at international forums like the World Trade Organization (WTO), where Canada opposes protectionism and supports free- and rules-based trade.

Third, this legislation is bad policy for a highly diversified economy like Canada’s. Removing options from trade negotiations out of the blocks would lead to less commercially meaningful results for all of Canada, because it would encourage every country to avoid making any significant concessions, especially in sensitive areas.

Simply put, prioritizing the economic interests of the products or sectors excluded above the economic interests of any other sectors in Canada is bad policy for a country where one-in-six jobs is generated by exports. And, make no mistake, this approach to trade negotiations will harm future growth opportunities for sectors that depend on trade, such as agriculture, energy, manufacturing, forestry, mineral products and consumer goods.

Finally, C-282 is bad from a food security perspective. International trade supports the accessibility and affordability of food. We cannot achieve global food security without free and open trade. As the world’s fifth-largest food exporter, Canada has taken on an obligation to feed the world. Closing access to markets is closing access to food. To that end, this bill also contradicts Canada’s commitments in recently signed declarations on food security at the Group of Seven (G7) Summit, Group of 20 (G20) Summit, WTO and Asia-Pacific Economic Cooperation (APEC) forum.

It should be noted that support for supply management and protecting it in trade negotiations is already long-standing government policy, from successive Canadian governments of all stripes. In fact, all of Canada’s recent marquee trade negotiations have been successfully concluded while protecting Canada’s system of supply management.

At the end of the day, there is no need or benefit for Canada to embrace and entrench protectionism on the world stage and set a dangerous precedent that delivers few – if not zero – benefits to the Canadian economy.

This is not an agricultural issue; this is a trade strategy and negotiation issue for an export-dependent country. We are calling on Canadian parliamentarians to look at the wider potential implications of this bill beyond the perceived short-term political clout.