Pork Commentary Jim Long President – CEO Genesus Inc. January 16, 2023

The December 1 USDA Hogs and Pigs Report indicated the market hog inventory at 66.966 million, a year ago 68.321 million. A 2% decrease year over year.

After seeing the 2% decline in inventory it was a surprise to us when we read the U.S. government’s quarterly Animal Product Production Report released last week.

Pork – Million Pounds

2022

2023

2023 as % of 2022

Quarter 1

6904

7040

+2%

Quarter 2

6639

6575

-1.4%

Quarter 3

6533

6650

+1%

Quarter 4

6920

7215

+4%

Total

26966

27480

+2%

Abracadabra – with a USDA report inventory of 2% less than a year ago, the USDA product report predicts 2% more pork in 2023.

You really wonder if USDA communicates within itself. There is absolutely no way the U.S. will have 4% more pork in the fourth quarter of 2023 compared to 2022. There is no scenario in the economics of this market that will lead one to believe in a 4% expansion. Negative producer margins, building costs, feed prices, labor issues, and the integrated model of owning pigs and slaughtering have been in the negative. We hear of capital calls and capital infusions to cover producer–packer integrated losses. This in no way leads to more hogs.

Now that we question the U.S. Animal Product report, we still show their predictions for Beef – Total Red Meat.

Million Pounds

Beef

Pork

Red Meat

2021

27948

27675

55815

2022

28302

26996

55482

2023

26445

27480

54108

USDA projects U.S. Beef Production to decline by almost 1.8 billion lbs. in 2023 compared to 2022. Total Red Meat production (including our belief Pork is overestimated) down about 1.4 billion lbs. in 2023. USDA predicts steers to be $1.58 lb. avg. in 2023 compared to $1.44 in 2022. Hogs 2022 71¢ lb. 2023 68¢ lb. To us seems strange with 1.4 billion lbs. less beef the hog price of the other red meat would be lower year over year.

The main takeaway to us is less beef for sure, we would bet less pork. Total Red Meat production is down. Less supply in a U.S. population that grows every year. We expect exports to steady. To us, a scenario of strong prices as moving forward into 2023.

Other Observations

Between holiday closures and bad weather, the U.S. hog slaughter was cut back the prior three weeks. This past week U.S. hog marketing’s roared back 2.688 million head, the week before 2.296 million, and last year 2.367 million. The big kill last week shows packer demand and supply. It will be interesting the next couple of weeks where slaughter numbers and hog weights go. Weights have jumped all over the last three weeks as slaughter numbers slowed.

Last week we highlighted the MIT article on GMO – Gene Editing. The article discussed the challenge of developing GMO – Gene Edited PRRS resistance pigs. The real concern will be if Retailers – Food Service – Importers buy the product. Consumer resistance hurting demand. One customer China ended all Paylean use – a legal product. What happens if one customer does the same with GMO – Gene Editing? With Paylean you stop immediately. What do you do if the market evaporates for a herd of GMO – Gene Edited pigs? Will the company who sold them to you compensate the loss? Quote, “I knew it was too good to be true, but I believed anyway.”

An article by the renowned MIT Technology Review (Massachusetts Institute of Technology) reports on PIC Gene Editing. An interesting part of the article on GMO-Gene Editing – PRRS.

“In experiments on pig cells, the Genus (PIC) researchers have tried many possible edits to the CD163 gene, looking for those that occur most predictably. Even with such efforts, the pigs being born have the right edit only about 20 to 30% of the time.”

Seems to us a huge spread between Beef and Pork Carcass prices. Beef is 3.4 times the price of Pork.

This tells us that consumers obviously will pay more for Beef. As a Pork Industry, we need to ask why. Obviously, consumers have the money to pay for the Beef, they are voting for Beef with their money. We expect the reason Beef sells for more is the eating satisfaction (taste) Beef has. On the flip side, the big discount Pork to Beef is a reflection of lower consumer demand.

If we are going to prosper as an industry, we need to figure out how to compete with Beef and pull our prices higher.

As many of you, regular readers know Genesus has worked diligently to produce Genetics with better taste. We can report seeing higher prices for better-tasting pork, consumers will pay for it, but it has to be better not just a story. We are seeing it in North America, Europe, and Asia. In some retail situations over $2 lb. premium to commodity pork. We need to make the pie bigger through a better product so everyone has a chance to get a bigger slice of that pie. Moving cut-outs to $1.20 is a lot better business than 81¢. We don’t think we will increase consumption and demand without an industry move to consistently better-tasting pork.

Next week we will be at the Iowa Pork Congress – visit us at Booth 1244 and or join us at the Genesus Reception on Wednesday evening.

Pork Commentary Jim Long President-CEO Genesus Inc. January 9, 2023

Last week it seemed the hog market had a holiday hangover. Shorter weeks of slaughter rarely seem to work for producers. This year was no exception. Lean Hog futures and cash prices all languished significantly. We expect as the dust settles and business returns to full week both lean hog futures and cash prices will rebound. Why? There are still fewer hogs domestically and globally. Also, less beef and less poultry. The only way to ration lower supply is higher prices. June futures were $1.05 on Friday. We expect in June lean hogs will reach $1.20.

Grain

Grains had issues last week. Corn down 24¢ bushel, soybeans down 32¢ bushel, and wheat down 49¢ bushel.

Corn in the USA is interesting. As of last week, U.S. corn export sale commitments are 47% lower than a year ago. U.S. corn ethanol production is barely holding steady. Certainly, makes you wonder where corn prices can go with exports significantly lower, ethanol production only steady, and all indications of less red meat and poultry production cutting demand.

Gene Editing

We have expressed concern about the ramifications of consumer acceptance of GMO-Gene Edited pork. A recent Iowa State survey indicates around 60% of women said they would be unwilling to eat and purposely avoid gene-edited foods.

The other issue as producers we should consider before we go down the path of consumer challenge. How well does the technology work? An article by the renowned MIT Technology Review (Massachusetts Institute of Technology) reports on Gene Editing. An interesting part of the article on GMO-Gene Editing – PRRS.

“In experiments on pig cells, the Genus (PIC) researchers have tried many possible edits to the CD163 gene, looking for those that occur most predictably. Even with such efforts, the pigs being born have the right edit only about 20 to 30% of the time.”

Seems to be a long way off that GMO-Gene Editing technology can deliver 100% of the population protected for PRRS. Makes you wonder not only about consumer acceptance but how effective the technology will be. We have all encountered products sold to us in the hog industry that the hype never delivered the expected results.

Finishing Mortality

An article by Bradley Eckberg MetaFarms/SMS in the National Hog Farmer reports on Finishing Mortality – data is from over 10,000 closeouts that MetaFarms has. The article highlights the continued increase in finishing mortality over the last ten years. The average is up nearly 1.5% over the last ten years.

Average Finishing Mortality

2013

4.28%

2021

5.12%

2022

5.69%

Last week we showed U.S. hog slaughter at about 126 million. Let’s say a 1.5% increase is equal to 1.9 million dead hogs. Let’s use the $80 value for a dead market hog. Our Farmer Arithmetic $150 million per year opportunity loss for the U.S. industry with the extra 1.5%. There is value in using resilient genetics. Over the last ten years, the industry has moved to mostly genetics owned and or based on European genetics. Not robust, lower appetite, temperament issues (tail biting, etc.). End of the day more dead pigs.

MetaFarms Performance Based on Mortality 2022

<3%

3-6%

>6%

% of total group

22.8%

43.5%

33.7%

Start wt. lb.

56

50.5

46

Out wt. lb.

282.37

284.1

282.27

Feed cost lb. of gain

41.78¢

42.34¢

43.70¢

Average daily gain lbs. per day

2.03

1.95

1.86

Average daily feed intake lbs. per day

5.58

5.51

5.35

Feed Conversion

2.75

2.82

2.87

Average day of finishing

110.7

118.3

123.0

Lots of data from a large database. Some observations:

Heavier pigs into finisher had lower mortality, growth, and feed conversion.

Lower-mortality pigs have higher daily feed consumption and growth rate.

It appears that pigs that live, eat and grow faster have a better feed conversion (Dead pigs eat feed before they die).

To us this data reinforces our premise high appetite pigs have lower mortality and lower cost of gain while getting hogs finished sooner (13 days). All economic factors contribute greatly to profitability potential.

Genesus at Shows

Genesus will be at the following upcoming shows/events including the South Dakota Pork Congress this week in Sioux Falls.

South Dakota Pork Congress – Sioux Falls, SD – January 11-12

Montana Pork Producers Council – Great Falls, MT – January 19

Kentucky Pork Producers – Bowling Green, KY – January 19-20

Iowa Pork Congress – Des Moines, IA – January 25-26

Illinois Pork Expo – Springfield, IL – February 7

Ohio Pork Congress – Lima, OH – February 7-8

Missouri Pork Expo – Lake of The Ozarks – February 21-22

Minnesota Pork Congress – Mankato, MN – February 21-22

AASV – Denver, Colorado – March 6-7

Montana Livestock Expo – Great Falls, MT – April 20

The Winter 2023 edition of the Canadian Hog Journal is here!

‘Innovation’ and ‘technology’ are buzzwords that are sometimes casually thrown around in a lot of industries. Prior to my time in the hog sector, I worked in Alberta’s research and development field, and I witnessed no shortage of empty promises, unfulfilled expectations and failed achievements that were once someone’s great idea and passion – only to fade away before ever becoming reality.

Representing more than just thwarted ambition, these underwhelming initiatives consume a lot of time, human resources and capital, which is perhaps the most regrettable part when they don’t work out. Innovation is a noble principle, and technology can be useful, but what matters most are tangible outcomes, and this edition seeks to shed light on some of the positive work being done when it comes to pigs and pork – going beyond the hype and examining the practical application.

Swine Innovation Porc (SIP) is the agency that has directed research in our sector for more than a decade, with support from provincial pork organizations, in addition to various industry partners, governments and academic institutions. SIP’s Cluster 3 research has just wrapped up, and Cluster 4 has started. Find a recap in this edition and find out what’s ahead.

The mission of Canada’s Agri-Food Innovation Council (AIC) is to be a unifying voice to advance Canada’s cross-sectoral agri-food research and innovation. AIC supports a carbon tax exemption on barn heating fuels, coupled with incentives for change, rather than unfairly punishing producers when they have no other options. Have a look at how AIC is fighting for farmers on the federal level.

When it comes to reducing greenhouse gas emissions, sequestration activities or purchasing offsets are the road-more-travelled if you consider most corporate policies on environmental sustainability. A new advanced pig genetics project by the U.S. National Pork Board and Pig Improvement Company (PIC) is approaching it from a different angle. Learn about why that’s a game-changer.

Measuring the environmental impact of animal agriculture, and communicating it, is yeoman’s work. On one hand, there are plenty of trustworthy folks looking to help farmers succeed, and on the other hand, a small but vocal minority of critics who would rather see them fail. Researcher, professor and presenter Frank Mitloehner is the undisputed champion when it comes to working with the livestock sector to mitigate its environmental impact while also maintaining professional neutrality and open public dialogue. He is widely respected by many for his support of responsible livestock production but reviled by some for his collaborative approach with industry. He recently felt compelled to clarify his stance, following an unprovoked attack by none other than The New York Times.

Three years ago, the Canadian Hog Journal introduced readers to a combined heat and power (CHP) unit that had been newly installed at a Hutterite colony in Alberta. Since then, the decision has proven nothing short of remarkable! The experience has been so encouraging, the colony just bought a second one.

Across Canada, in-person events seem to have fully returned, including the Porc Show in Quebec City and Prairie Livestock Expo in Winnipeg. Get the details here, and read about the 2023 Banff Pork Seminar in our next edition.

My family-of-four is now a family-of-five, as my wife, Kira, and I welcomed our third child and first son, Emeric, in mid-October. His older sisters, Agatha and Wilhelmina, have been enthusiastic little helpers as we learn to navigate and appreciate our new life together.

As always, I can be easily reached by email at andrew.heck@albertapork.com. You can also get my attention on social media and ‘follow’ the Canadian Hog Journal on Facebook and Twitter (@HogJournal) to contribute to the discussions that matter to you and the rest of the industry!

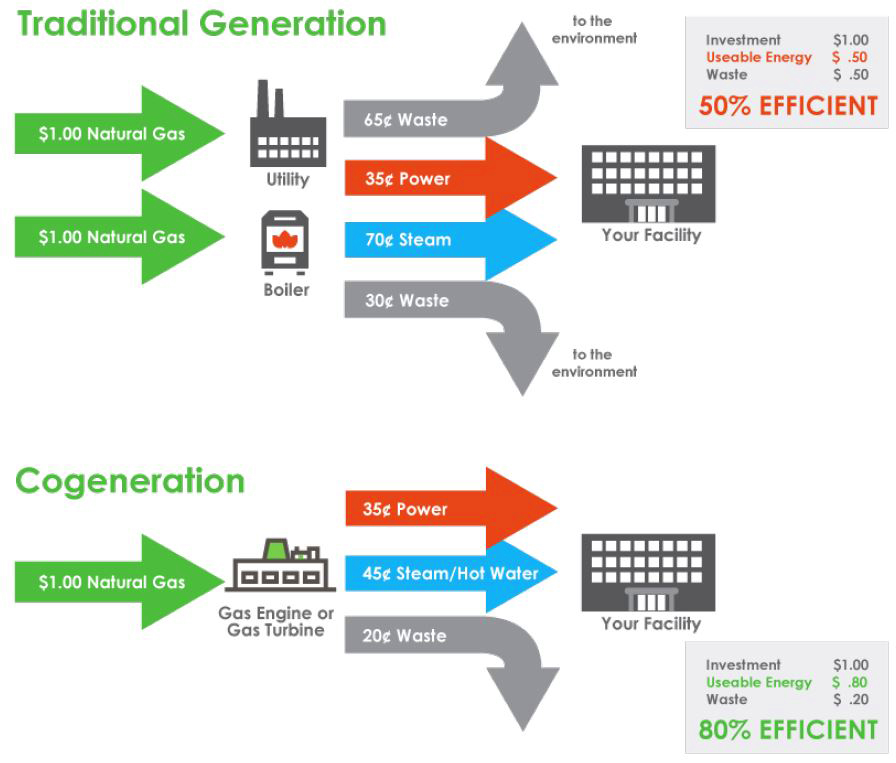

With traditional generation, more input energy – and money – is wasted, in addition to greater environmental impacts versus CHP.

Lowering emissions in animal agriculture is not only eco-conscious but potentially cost-efficient, if done strategically.

‘Cogeneration’ or ‘combined heat and power’ (CHP), is the use of a prime mover engine to generate electricity and heat at the same time, using a feedstock energy source like natural gas, methane or biogas. Such technologies are becoming increasingly popular not only for heating and powering large commercial and industrial buildings but also farms.

Alberta Hutterite colony implements CHP

In August 2019, Hartland Colony installed a combined heat and power (CHP) unit in its hog barn. Since then, energy savings have allowed the unit to pay for itself, with many years of useful life still ahead. The technology was so successful that a second unit has since been purchased.

In August 2019, Hartland Colony near Bashaw, Alberta – about 130 kilometres southeast of Edmonton – purchased a CHP unit in a bid to offset on-farm carbon emissions and costs, primarily aimed at the farm’s 650-sow, farrow-to-finish hog operation, crop production and canola crushing plant. Representatives from Hartland travelled to Germany to scout out potential products, then a Canadian partner was recruited to help broker a deal.

The CHP unit – manufactured by TEDOM, in Czechia – initially cost more than $600,000 all-in, from purchase to delivery to installation. Earlier this year, the capital cost was considered completely recovered, slightly quicker than anticipated, and well before the machine’s useful life expires. It is estimated to be running for another decade, at the bare minimum.

“At this point, the machine has more than paid for itself,” said Chris Waldner, Hartland’s electrician, who monitors the CHP unit. “We’re running at 100 per cent capacity, all day, all night, and we’re now even putting excess electricity back into the grid.”

Initially, the unit was operating at around 85 per cent capacity, based on need, but starting in mid-2020, the colony was offered a new contract by its utility supplier to be credited for unused electricity, particularly in winter, when demand is lower.

“We do as much maintenance on it ourselves as possible, and we’ve found that the manufacturer’s recommendations for frequency are very generous,” said Waldner. “In fact, we’ve had no major issues with it. The first scheduled major overhaul was at 20,000 hours of operation, but we’re now close to 30,000 hours, and it hasn’t been necessary.”

While electrical generation is the primary function of CHP, the secondary benefit, recovered heat, has plenty of applications as well. In winter, while hog barn ventilation is restricted, the heat is used to maintain temperatures in the barn and on other parts of the farm using a centralized loop. Year-round, even with higher summer temperatures, recovered heat continues to be pumped into the farm’s canola crushing plant, which provides canola oil and meal for use in the hog operation but also brings in additional revenue through external sales.

“About 50 per cent of the heat generated by the machine is recovered and used,” said Waldner. “When you crush canola, it needs to be about 30 degrees-Celsius, so using the recovered heat prevents us from needing to burn gas that would otherwise generate that heat.”

By all accounts, Hartland’s CHP experience so far has been even better than anticipated. So much so that the colony has since ordered an additional unit, even larger than the previous one. The new unit is expected to come online very soon.

“It’s bigger, it’s made in North America, and we have dedicated local tech support,” said Waldner. “That was important to us, weighing against other available options.”

The plan is to run the new, higher-capacity unit at whatever level is necessary to meet the colony’s needs, with the older, lower-capacity unit reserved for times of increased demand, such as harvest, since grain dryers can be a significant power drain. By running the larger unit around 90 per cent capacity most of the time, rather than both units at 40 or 50 per cent concurrently, unnecessary stops and starts can be avoided.

“The need changes based on time of day and time of year,” said Waldner. “The nice thing about having two units is that we benefit even more from keeping the power on-farm versus simply getting credited when we have too much. It saves even more money and is even more environmentally friendly.”

Finding the right fit for the future

Hartland’s new CHP unit is even bigger and more powerful than the one put into service three years ago, which has already been paying dividends for the farm.

Hartland’s new unit was manufactured by Missouri-based Martin Energy Group. The company supplies a range of products in addition to CHP, such as micro-grids and anaerobic digesters – commonly used to process manure for electricity. So far, in Canada, they have worked with greenhouses in Alberta and Ontario, but hogs represent a new venture north of the border.

“We typically build larger-scale units suited to industrial operations, but Hartland was ambitious and wanted to see what options we could provide,” said Kevin Roher, Sales Manager, Martin Energy Group. “They were very clear on what they were looking for in terms of technology that was customized for their farm and able to be serviced and supplied easily.”

The price tag on the new unit was close to $750,000 and, like the older unit, that initial investment is expected to be recovered in a fraction of the time that the technology will be operable. At best, Hartland is expecting to pay off the unit in three to four years, and at worst, in six to seven. While lower energy prices are generally preferrable, the trend of higher prices equals bigger savings in the short-term. Whether prices stay high or drop lower, the farm is well-situated to make the most of the market rates.

“These units have served us very well so far, and we’re excited to share the news with other operations,” said Waldner. “To us, this makes a lot of sense, and it might make sense for them, too.”

According to Roher, Hartland’s pace-setting example has led to further business for Martin Energy Group, as two additional Hutterite colonies in Alberta are actively purchasing CHP units through the supplier.

“It’s been great for all of us,” said Roher. “Hartland has been an excellent client, and we appreciate their straightforward, honest approach.”

Supporting farmers’ transition to clean tech

Across Canada, completing an Environmental Farm Plan is an important first step farmers can take to potentially receive funding for implementing technologies like CHP.

With technologies like CHP increasingly making their way into the hog sector, emissions reductions and cost efficiencies are becoming more readily available, assuming they are affordable in the first place. For many producers, this may not be the case without additional incentives that encourage innovative practices.

While certain funding programs are in-place on various provincial and federal levels to support the transition toward the use of clean technologies in agriculture, many of these initiatives are available only for operations that have completed an Environmental Farm Plan (EFP), offered in virtually every province under the Canadian Agricultural Partnership (CAP). Creating an EFP is free and highly recommended, since it is a prerequisite for accessing most forms of government support.

As more and more producers take steps toward improving their on-farm practices, it is incumbent upon decision-makers to recognize this willingness to adapt, proactively, rather than resorting to penalties for longstanding behaviours where few, if any, other options exist.

In the case of Hartland Colony, as with many other farms across Canada, producers are willing and able to make a positive difference when it comes to environmental sustainability, but it is hugely beneficial when financial burdens are lessened, so farmers can continue producing food for Canadians and the world without needing to make costly sacrifices that could jeopardize business continuity. Successful incentivizing can even lead to self-sufficiency, which is the case with Hartland’s new CHP unit, for which no outside funding was required or received.

Environmental and financial sustainability alike can and should become the goal for all farming operations in Canada, and this is certainly possible, when the conditions are tailored to farmers’ needs. The future of food production and public trust in agriculture looks bright if experiences like Hartland’s can become the norm, rather than the exception.

Quebec City’s ‘Petit Champlain’ quarter in the old town – named for founder Samuel de Champlain – is one of many perks for guests at the Porc Show, which was back in-person this year.

Following a three-year hiatus due to COVID-19, the Porc Show returned in-person for more than 800 guests at the Quebec City Convention Centre on Dec. 6 & 7.

Without a doubt, producers and industry partners from coast-to-coast have had their calendars marked since 2019, eagerly awaiting this pilgrimage to Canada’s second-oldest city and the country’s largest pork-specific conference.

From an exploration of supply chain issues in meatpacking and the environmental impact of pork, to improving the judicious use of antimicrobials and better management of feed, the Porc Show this year featured a full slate of engaging speakers and timely topics.

Supply chain issues continue to hamper meatpacking

Executives from federally inspected meatpackers spoke frankly about the challenges they have faced in the past few years, during an on-stage chat to kick off the first day of the event.

On the first afternoon of the conference, a panel discussion took place with Paul Beauchamp, Vice President, Olymel; Arnold Drung, President, Conestoga Meats; and Stéphanie Poitras, Executive Director, Aliments Asta, covering a range of issues that have created obstacles for packers, including political tensions, labour shortages and consumer demands.

Uninterrupted market access for Canadian pork continues to be a barrier. For Drung, the often-rocky but usually reliable trade relationship between Canada and China has been more unpredictable in recent times.

“You can’t build a business plan on China,” he said.

While high-quality cuts of meat earn a premium in markets like Japan, price-conscious markets like China favour offal, which has few other outlets, almost none of which are domestic. Despite that favourable situation, certain high-level decisions still prevent some Canadian packers from sending pork to China, without much hope of change anytime soon.

For Beauchamp, filling shifts at Olymel’s plants in Quebec has proven harder than he would like. For years, his company has targeted foreign workers from Francophone countries in the Caribbean and North Africa, but even that has proven to be not enough. Thankfully, an update to federal legislation is now making it easier for families of Temporary Foreign Workers (TFWs) to come to Canada. Drung concurred, citing the example of two Filipino workers who joined Conestoga nearly two decades ago as TFWs and remain with plant today, as a result of eventually having established permanent roots in Canada.

“The meat industry has always been an industry of immigrants,” he said. “Look back 100 years. We have a good track record with them, and a lot of them want to stay.”

In addition to politics and labour, new considerations have emerged when it comes to the preferences of international pork buyers.

“We’ve had enormous pressure in the last five years on animal welfare,” said Poitras. “We need to watch everything we do.”

Despite this, members of the panel agreed that, between Canadian Food Inspection Agency (CFIA) requirements and voluntary quality assurance programming, the Canadian pork industry has a better handle on animal welfare than some other major producers globally, which should be an encouraging prospect.

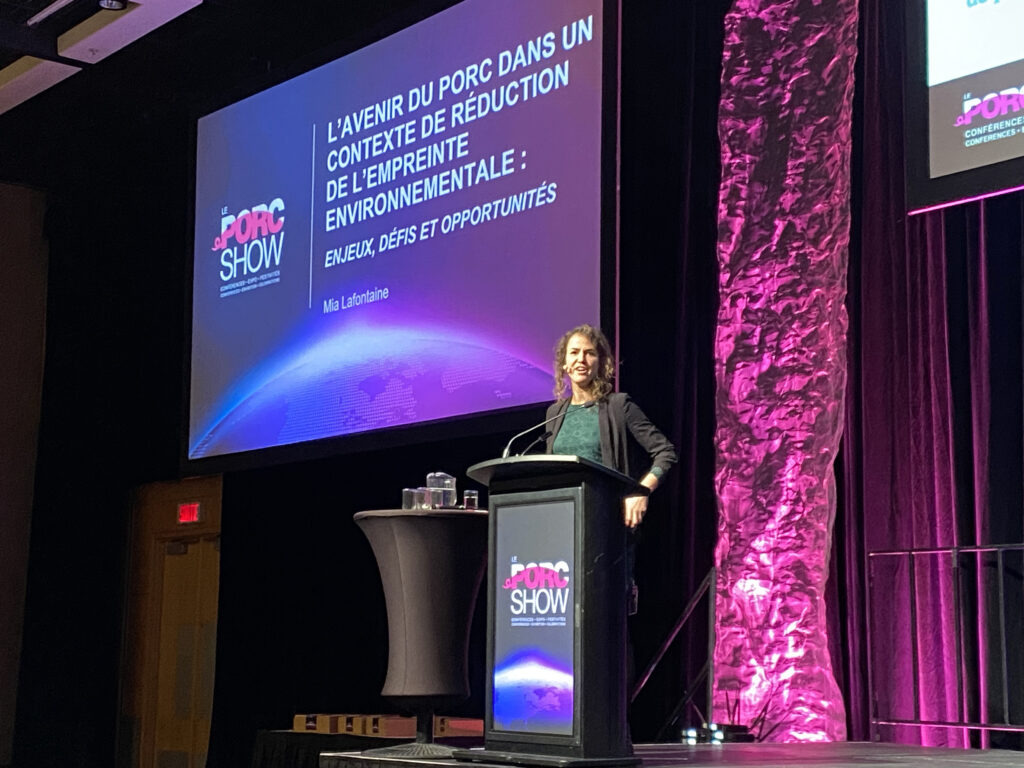

The future of pork’s environmental impact

When it comes to climate concerns, threats to the agriculture industry are inevitable and ongoing. Turning those threats into opportunities is key.

Mia Lafontaine is a consultant and speaker in sustainable development for the agri-food sector. She has previously worked as a feed company representative. Originally from France, she currently lives in the Netherlands, which is at the centre of a bitter dispute between farmers trying to protect their livelihoods and a government that is hostile toward agricultural land use.

However, based on data out of Quebec and Ontario, pork’s increasingly smaller land use in our country is already very competitive globally. But when it comes to measuring environmental impacts on-farm, we have some work to do. In order to fully understand the sector’s carbon footprint, we first need baseline data to measure improvements over time, which is beginning to happen.

Not only in Europe, but also in Canada, packers and retailers are starting to set ambitious climate targets. She cited Maple Leaf Foods and Loblaw as two examples of companies looking to become ‘carbon-neutral.’

“Despite the environmental crisis being a global problem, we have to start working locally,” said Lafontaine. “As an industry, we have to stop thinking this isn’t a priority – it is.”

Lafontaine believes some important steps for producers include environmental farm planning and responsibly applying hog manure to crops, offsetting the use of chemical fertilizers. Both practices align with federal government priorities and represent a huge opportunity to demonstrate success, which could translate into financial support.

Threats also continue to linger. Despite varying degrees of government support in Canada, myths regarding the use of water and plastics in agriculture continue to eat away at public trust. While some elected officials here are working toward a carbon tax exemption on farm fuels, in New Zealand, producers will soon be taxed on total farm emissions, starting in 2025. Avoiding such unreasonable legislative steps will be a massive task for all of Canadian agriculture.

Progress sought on antimicrobial use

Around 700,000 people die every year across the planet due to antimicrobial resistance (AMR), which disproportionately affects those in the developing world. At the current rate, that number is predicted to climb to 10 million annually by 2050, according to Laurie Pfleiderer, a veterinarian with Triple-V Inc. The culprit? Depending on which source you consult, animal agriculture has a lot to do with it.

While there is a tangible yet fairly weak link between AMR that impacts animals and AMR that impacts humans, the issue is not so black-and-white. Between 2016 and 2020, global antimicrobial usage (AMU) declined by 20 per cent, but there is still much room for improvement. Data presented by Pfleiderer suggests median AMU in Canadian livestock production is slightly higher than in the U.S. and about three times higher than in Europe, with hog production composing the greatest single proportion of that usage.

Many different and often valid reasons exist for administering antimicrobials, and ‘judicious use’ means they may continue to be used to ensure animal welfare. But where alternatives exist, Pfleiderer believes those should be explored.

“Why are you giving antibiotics? Is it treatment or prevention?” she asked. “You need to have a conversation with your veterinarian to address the problem in the best way.”

Vaccine protocols are one alternative, along with options like water acidification and even the use of essential oils. Favouring individual treatments for smaller numbers of animals can help prevent bacterial spread to an entire herd and the need for mass treatment.

Feed management makes the difference

‘Teamwork makes the dream work.’ Or, when it comes to feed management, producers and nutritionists finding solutions together.

Misuse of feed can equate to tens of thousands of dollars of losses annually for a producer, depending on barn size. Feed represents not only the largest chunk of production costs but also contributes significantly to pork’s ecological impact. As such, managing feed effectively and efficiently makes a great deal of sense.

Aurélie Moulin is a nutrition consultant with Agri-Marché Inc. Her main recommendation is to use ‘feed budgets’ containing specific phases to optimize rations. The better the phases are defined, the more controlled the process can be.

As sow feed composition changes, so does density, and so should volume, accordingly. Particle size is a factor, whether the feed is pre-mixed or made on-farm. Feed wasted in gestation can range from nearly $10 per sow to upwards of $40 per sow, and during lactation, heat stress can have negative impact on performance. The hotter a sow is, the less she will eat.

Starting from farrowing, nursey feed management is critical. It is the costliest stage and has the greatest impact on future performance. Understanding proper feed composition in weaning helps prevent diarrhea and lost energy. Lighter piglets are especially vulnerable in this regard.

Feed that goes uneaten is also part of the problem not only on a cost basis but in terms of performance as well.

“Any feed that isn’t consumed is made up from body reserves,” said Moulin. “Having access to enough feed early on is important for growth.”

However, feed intake levels and performance are not always correlated. Finding the sweet spot for your operation is key. Maintaining feeders is an important task for producers to help themselves manage feed better and control costs.

As an overarching message, Moulin believes that this area is not only the responsibility of a nutritionist; producers must work closely with their partners to ensure that feed is being put to best use from day one all the way to shipping out of the barn.

Porc Show highlights the industry’s best

This year’s meal included braised pork shank; potato and parsnip purée; winter veggies with bacon; and a pan sauce of beer, mushroom and maple. The dish was the winning creation of culinary students from Quebec’s Institute of Tourism and Hotel Management – an annual tradition for the Porc Show.

The gathering of minds at the Porc Show is special and different from most other North American pork conferences. Not only the predominant use of the French language and the wonderful setting, but also the level of expressed government commitment to the province’s pork sector.

“We want the industry to be profitable, and the industry is only as strong as the weakest link in the value chain,” said André Lamontagne, Minister, Quebec Agriculture, Fisheries and Food. “We need to focus on each part. Is it working for everyone in the long term? We need to find solutions.”

Canada’s ag minister, likewise, echoed the sentiment of strengthening the sector through continued collaboration.

“I know the situation is not easy, but the federal government wants to support producers as much as possible,” said Marie-Claude Bibeau, Minister, Agriculture and Agri-Food Canada (AAFC). “Our ASF funding is designed to support biosecurity and wild boar management, and new market development opportunities are meant to support trade.”

With another Porc Show in the books, participants are reminded of the beauty, diversity and history of Canada and our industry, which are stronger united – in-person – than divided along boundaries we impose ourselves. Together, we can continue to do great things across the value chain and across our country.

Pork Commentary Jim Long President – CEO Genesus Inc. January 3, 2023

2022 is over. Interesting year for global pig production. High feed prices all over the world minimized profits for pig production. In many areas, the high feed prices trumped hog prices leading to financial losses. Producers who grew their own feed had a good year if you look at the whole farm income.

USA – North America

As we look to 2023, we see swine inventories lower than a year ago. On December 1 the U.S. was down 1.4 million head from the year before and 4.3 million less than two years ago.

In our opinion, high feed prices relative to hog prices are leading to even lower hog production levels in the near term.

The dynamics of labor challenges, new animal welfare pressures (Prop 12), disease, increased building costs, higher interest rates, old facilities, etc. curtail much expansion enthusiasm.

There will be less U.S. beef in 2023. USDA projecting -7%. Even if it’s not that large there will be significantly less beef in 2023. This will support pork prices.

Poultry is having a big challenge from Avian Flu. The latest data shows 57 million exterminated in the USA. It appears to be not letting up. Egg and Turkey prices have jumped significantly so far, it’s not hit Chicken Broilers as hard. Higher poultry prices support pork prices.

We expect no growth in Canada’s swine sector. It hasn’t changed in five years, and we expect this to continue.

In Mexico, there is not the most reliable inventory data. Price is the reality of supply. Last week Mexico’s national average price 44.75 MXN/kg ($1.06 U.S. liveweight a lb.). The spread between U.S. – Mexico 40¢ lb. or $100 a head. To us, this means Mexico is short of pork pushing prices higher. This is the reason huge amounts of U.S. pork are being imported and will continue.

Productivity

The U.S. Federal Inspected hog slaughter in 2022 – 124.673 million.

The Canada Federal Inspected hog slaughter in 2022 – 20.911 million.

Total – 146.584 million.

The combined U.S. – Canada swine breeding herd in June – July 2021 was 7.482 million.

If we divide 7.482 million into 146.584 million market hogs the result is 19.6 hogs slaughtered per breeding animal.

Combining U.S. – Canada data captures the pigs imported from Canada whether as small pigs or slaughter.

The average of 19.6 indicated the reality of production. Half are below 19.6.

Dead sows don’t have pigs – average U.S. sow mortality is 14-15% – half of the producers are higher.

Wean to Finish mortality – 9.5% – half of the producers are higher.

Both sow mortality and wean-to-finish mortality have been increasing.

Having more resilient genetics has some true economic benefits.

Observation

Last week we wondered about the December 1 U.S. inventory report showing a steady breeding herd. Some of the other data didn’t support this in our opinion. This past week we looked at data further. Here’s an observation.

Illinois Breeding Herd (1,000 head)

2021

2022

September 1

660

590

December 1

590

660

Last week we spoke to several hog industry people we know in Illinois. We asked what did they think of Illinois gaining 70,000 sows from September to December. To summarize no one seemed to name and know where anything close to this could have happened. The thought was September – December was next to zero. Look at numbers from USDA. Did someone transcribe wrong. Are we to believe last year Illinois liquidated 70,000 and this year expanded 70,000. In our opinion good chance the USDA breeding herd on December 1 was overestimated. There is a reason less hogs are coming.

Europe 2023

Europe has over 10 million sows. It is a major global producer and exporter. We wrote in October 2021 that the economic conditions of Europe’s industry would lead to the liquidation of 1 million sows before it is done. The inventory report has not been released for November – December this year for all countries. Germany the second largest producer in Europe released there’s a week ago. Down 400,000 sows in the last two years.

Pig numbers are down across Europe leading to high hog prices but with high feed costs. Spain’s price last week was 1.645 Euro/kg (79.8¢ U.S. lb.). Europe has had an advantage in exports through the summer and early fall with lower hog prices then USA-Canada. Now U.S. 60¢ lb. – Europe 80¢ lb. Expect more U.S. exports.

In 2023 we expect continued high hog prices in Europe due to less supply of pork. With less pork, there is less to export.

China 2023

The lifting of Covid restrictions and large numbers of Covid infections has put big pressure on China’s hog price. In our opinion sick people don’t eat much. Don’t go to restaurants for the fear of getting Covid. Price has dropped over $100 per head but is still high at 17.48 RMB/kg ($1.11 U.S. liveweight lb.). China from what we observe had earlier released its pork reserves. There is no more to release.

Who knows what will happen next. We believe the financial losses from the end of 2021 and into 2022 cut China production in the 10’s of millions. That’s why the China hog price is so strong.

As Covid eventually slows down we expect the China hog price to recover as there will be still a lot less hogs than a year ago. We expect more pork imports.

2023

We see less hogs in North America, less hogs in Europe, less hogs in China. These three areas are about 75-80% of global pork production. This decline in our opinion will lead to very strong hog prices. We continue to believe the summer U.S. price in 2023 will reach beyond $1.20 lb.

We hope in 2023 our industry continues to move to producing better-tasting pork. It is the true driver of consumer demand. It is a way we can grow per capita consumption and sustainable profits. Better eating experience pork we observe in retail stores will sell for more than antibiotic-free and or pen gestation. Taste trumps all. Consumers vote with their money.

Pork Commentary Jim Long President – CEO Genesus Inc. December 19, 2022

Last week we attended the Prairie Livestock Expo held in Winnipeg, Manitoba. The defacto Pork Congress for the Manitoba Pork Industry.

Our Observations

The Manitoba hog industry has about 341,000 sows, with little change over the last five years.

There are three major producer companies. HyLife, Maple Leaf Agri Farms, and Progressive Group. Combined about 210,000 sows of Manitoba’s production. All three have hog slaughter capacity.

The rest of the production is independent hands including Hutterite Colonies.

A significant part of Manitoba’s production is exported as small pigs to the USA (80,000 a week approximately). There are few market hog exports.

Consolidation in Manitoba has happened in the last decade as both HyLife and Maple Leaf have acquired significant-sized production groups. Maple Leaf purchased Puratone – HyLife purchased ProVista. Manitoba like the rest of the world the big get bigger.

The Hutterite Colonies are mostly farrow to finish. They have large land bases and grow most if not all their feed needs. This past year has been good for the whole farm income. Have pigs, grow crops, put manure on land for fertilizer. Most Hutterite Colonies are excellent pig producers and coupled with the whole farm approach a model that has had a very successful 2023 as opposed to buying expensive feed.

The Prairie Livestock Expo last week had a very good turnout despite tough travel conditions due to a snowstorm. It was the first event in three years as the other annual shows were shut down for COVID. There were lots of exhibitors this past week for the one-day event. It was so busy you wonder if two full days would not be warranted.

As part of the event, there is a carcass competition with many producers entering hogs to find the best traits for eating attributes. A Genesus customer Woodland Colony entered a Genesus Jersey Red Duroc sired pig bred to a Genesus F-1. The pig came first of all who are supplying to Maple Leaf Foods plant in Brandon, Manitoba the largest slaughter plant in Canada. We congratulate Woodland a Genesus customer for over twenty years. This win comes off Genesus sweeping the Maple Leaf Foods – Lethbridge, Alberta Plant Awards were given out a few weeks back that had full program Genesus customers finish 1, 2, 3 as the best carcass quality. The pork that goes into the Lethbridge, Alberta plant has a brand name called Lethbridge Heritage which is considered the most premium pork in all of Canada. Genesus full program Jersey Red Duroc x Genesus Female customers are responsible for a high percentage of the pork that goes into this plant and premium pork brand.

There is no net expansion in Manitoba. The sow herd is holding steady. The cost of buildings, feed costs, labor issues, etc., and more importantly the general lack of profitability is not conducive to having an industry grow. Manitoba goes sideways.

Members of Genesus present at the Prairie Livestock Expo

Other News

A reflection of the financial challenges felt in the European Union swine industry is the latest inventory report from Lower Saxony one of the major swine-producing areas in Germany. From November 2021 to November 2022 the sow herd is down -16% to 359,800. The market inventory is down from 7.8 million to 7.1 million a -8.9% decrease. With the sow herd down -16% we would expect an even further decline in the market inventory going forward. We expect Europe’s market hog numbers to continue to plummet in 2023. Less pork = higher prices.

Lean Hog Futures continue to gyrate up and down. Last Friday some future months jumped $4.00. Summer months at $1.06 range are still undervalued relative to what we see coming in 2023 for U.S. and global pork production, both going to be down. We expect lean hogs to reach $1.20.

Summary

The industry is not very buoyant right now. Losses continue currently when you factor in high feed prices. Both packers and producers are hurting. Some packers and producers losing millions upon millions. There is not much joy in Mudville. Despite this and maybe we are the boy who sees a pile of manure and thinks there is a Pony inside. Too optimistic? But despite this we see a total lack of supply coming in the next few months not only from pork but beef and poultry with the continued Avian Flu issues. We remain optimistic about real solid hog prices and good profitability. Maybe there is a Pony?

Merry Christmas

Never got a Pony for Christmas, but it was always a special day in our house. It was the only day of the year that we didn’t work on the farm. That in itself was special. But we had church and all the extended family got together. We weren’t prosperous when I was a child, but we felt wealthy. Growing up on the family farm we were around parents, brothers, grandparents, uncles, and aunts. Like most dynamics, this in itself had its challenges but I wouldn’t trade my upbringing for anything. It’s one of the great things of family farms. I am happy my family got to work and continues to work together. Christmas was and is about family time.

I expect many in farming have similar experiences and memories. Being a family farmer is being part of a special tribe no matter where you are in the world.

To all, we wish you a Merry Christmas and a Happy New Year.

Pork Commentary Jim Long President-CEO Genesus Inc. December 12, 2022

Last week we attended the Midwest Pork Conference held in Lebanon, Indiana. Organized by the Indiana Pork Producers Association it attracted producers and exhibitors from the state of Indiana, Ohio, Michigan, and Illinois.

Our Observations

As our industry consolidates there are fewer vendors and producers. Less people selling to less people. Not that many years ago a similar event was held in Indianapolis at the Indiana Convention Center a large and expensive venue with many vendors and producers attending. It’s not necessary to have such a site anymore. Consolidation has led to fewer producers and vendors.

Last week’s Midwest Pork Conference was well organized and the facility was good. Keynote speakers brought interesting perspectives and breakout sessions had good production topics and were well attended.

The exhibits were fewer than in the past, a reflection of the consolidation we have seen. For example, in years past there would have been up to 20 plus exhibitors selling swine genetics, including Indiana-based companies. This past week including Genesus there were five. None from Indiana and three of the five are based in Europe.

Our sense from talking to exhibitors and producers last week is the sow herd is continuing to contract. The combination of producer profitability being next to non-existent and high feed prices is contributing to less sows. Steve Meyer ag economist was one of the speakers and he reported that since 2004 to date the average producer has made a profit of $2.04 per head. A staggering low number is not conducive to optimism or reinvestment.

Is there any wonder there are next to no new players entering the swine industry? It appears it’s only the marooned that continue production.

Jayson Lusk an ag-economist from Purdue University spoke. He reported only 25% of the retail pork price comes from the producer hog price. Tells us the hog price has to be significant to really alter retail pork prices. Recently retail pork price is near record levels.

Last week it was nice to speak to a number of readers of the commentary. It’s interesting the number of people who believe as an industry we need to produce better-tasting pork to increase demand. The second part is the number of producers who affirm the prolapse problem and high sow mortality in certain genetic lines. Many agree – Dead sows don’t produce pigs

Not sure what the data says but from conversations last week there appears to be PRRS and PED hitting more than enough producers.

Speakers at the conference spoke of California Prop 12. Now delayed until summer 2023 while waiting for the Supreme Court decision if it is legal. It was reported about 300,000 sows in the U.S. are currently Prop 12 compliant, the estimate is 600,000 are needed to feed California – 10% of U.S. sow herd. Prop 12 herds with breeding in pens will be seeing lower farrowing rates and litter size which not only lowers production but increases the cost of production. Need more money to produce Prop 12 pigs. We were told ½ to 1 pig per litter decrease, 5-10% lower farrowing rate than breeding in stalls and holding over 35 days post-breeding.

We sense the U.S. supply of hogs is decreasing. The summer hogs have been bred and made. There is no way in our opinion we won’t have less hogs in summer 2023 than 2022. The lean hog futures are significantly undervalued to the reality we expect. There will be less beef, there will be less turkey and eggs due to Avian Flu. There will be less pork in Europe and they will have less to export. China already has less pork production and will pull pork in. October U.S. pork exports were the largest in more than a year (June 2021). We expect the trend will continue as the world pork supply declines. We need to get through the next few weeks of the shortened holiday weeks but we believe 2023 will have very strong prices.

Members of Genesus at the Midwest Pork Conference

Jersey Red Duroc

Genesus has believed for over two decades that as an industry we should be producing pork that is more marbled, redder, and juicier – Taste matters. Our Jersey Red Duroc continually dominates taste tests globally. The link below is Genesus’ Chef Glenn Mckenzie Smith preparing Genesus Jersey Red Duroc pork. If as an industry we are going to grow pork demand we need to deliver a better eating experience. When is it bad business to have a better product?

Click on the below link to watch Jersey Red Duroc – Pork Chop video:

Pork Commentary Jim Long President – CEO Genesus Inc. December 5, 2022

Last week Lean Hog Futures dropped big time and then recovered the losses by Friday’s close. When the dust settled July closed at $107.15 a new contract high. We believe July will be $1.20 plus before it goes off the future board.

Some Other Observations

Much angst at the first of last week over the effect of COVID lockdowns to China’s domestic pork demand and import potential. If markets reflect demand, look no further than China’s National hog price it increased last week from 22.93 RMB/kg ($1.44 U.S./lb.) to 23.17 RMB/kg ($1.48 U.S./lb.). Seems China’s domestic market did not get hurt by COVID lockdowns.

The U.S. corn price seems to be hitting some headwinds. March corn closed to 646’2 or 25¢ a bushel net loss for last week. We continue to wonder how this can’t be further pressure on corn prices when U.S. exports are substantially lower than last year (-40%). A week ago, corn exports 13.6 million bushels compared to USDA expected export levels of 48.4 million bushels. Seems the lack of water in the Mississippi is restricting exports from less barge movement. We don’t see how current poultry and livestock inventories will increase corn consumption. Corn for Ethanol seems stable. Seems to us lower corn exports could continue to put pressure on the corn price including basis.

Always makes us wonder why USA – Canada with surplus grain and oilseed production doesn’t put together strategies to produce more red meat to export for added value rather than just ship grain and oilseeds.

Due to the Avian Flu, the U.S. has culled 50.5 million birds mostly chickens and turkeys. The UK and Europe have also experienced major Avian Flu breaks. In the U.S. a large dozen of eggs was $3.50 last week. At first of the year, they were $1.00. One of the latest breaks a 1.8-million-layer flock in Nebraska. Less eggs and poultry meat are supportive of hog prices. Looking at the current egg price it appears the saying “One person’s misery is another’s opportunity” seems to be true.

Seems the U.S. hog price currently is lower than Europe’s. For several months it was the other way around making U.S. pork less competitive in global markets. In U.S. dollar liveweight a lb. a week ago U.S. 62¢, Spain 77¢, France 71¢. We expect this difference in pricing will help USA – Canada pork export sales.

Last week it was announced JBS has purchased assets of Tri-Oak of Iowa. It is reported to have no real estate involved. Tri-Oak is reported to have 70,000 sows and was already sending their market hogs to JBS harvest plants. This acquisition will push U.S. JBS swine operations over 200,000 sows. JBS also has significant sow production in Brazil and the United Kingdom. To us, this is part of the domestic global consolidation ongoing. The big are getting bigger. 39 producers in the U.S. control 65% of the U.S. sow herd (one of the 39 was Tri-Oak). Recently Seaboard Foods acquired some sow production from the Maschhoffs. We are hearing of other major changes in ownership coming. “Change is inevitable, except from vending machines.” – anonymous old quote.

China

In China, there are 92 swine nucleus farms in the National Breeding Pig Evaluation Program. As part of the program, the data is evaluated by comparing and ranking the performance of each participating nucleus. With 92 farms participating we are unaware of any such comparison ongoing of such scale in the world. Our understanding is all major swine genetic companies have nucleus farms in the national program. It’s quite a unique structure. When you consider the scale and competition for the 92 farms, we were really pleased to see Genesus Nucleus Meishan Wanjiahao Pig Breeding Co., Ltd. (WJH) dominating the recently published data reports. Genesus WJH No. 1 Duroc 141.63 days. Genesus WJH No. 1 Landrace 144.29 days. Genesus WJH No. 2 Yorkshire 147.80 days.

Days to 100 kg

Genesus WJH

National System No. 10 herd result ranked out of 92 herds

Duroc

141.63

152.29

Landrace

144.29

154.15

Yorkshire

147.80

154.22

We only have data of the top 10 herds of each breed but already you can see the dominance of Genesus.

WJH was an import from Genesus and has been operated as part of Genesus Global Genetic Program – MaxGen. We congratulate the WJH team on their execution of the Genesus Genetic program and excellent production management.

We believe Genesus has the fastest-growing genetics. Fast-growing pigs have a high appetite and that lowers wean to finish mortality. Our Jersey Red Duroc doesn’t only grow fast but produces pork with the best eating attributes that consumers crave.

92 nucleus farms in the China system, every major global genetic company is represented. Data shows Genesus domination.

Jersey Red Duroc

Genesus has believed for over two decades that as an industry we should be producing pork that is more marbled, redder, and juicier – Taste matters. Our Jersey Red Duroc continually dominates taste tests globally. The link below is Genesus’ Chef Glenn Mckenzie Smith preparing Genesus Jersey Red Duroc pork. If as an industry we are going to grow pork demand we need to deliver a better eating experience. When is it bad business to have a better product?

Click on the below link to watch Jersey Red Duroc – Pork Chop video:

Pork Commentary Jim Long President – CEO Genesus Inc. November 28, 2022

Last week we were honored to be invited to speak at the Alberta Pork Annual General Meeting. Alberta Pork is the pork producer organization for the province. Our observations:

The Annual General Meeting was well attended with 350 people present and well organized. Thank you to Darcy Fitzgerald, Executive Director of Alberta Pork, his staff, and the Alberta Pork board of directors for their excellent hospitality.

The province of Alberta is in the western part of Canada. The inventory of sows is 123,000 in 2022. About 40% of this production is done by Hutterite Colonies with a balance of independent – producer groups. This sow herd has been stable in numbers over the last few years.

In our opinion, some of the best producers in the world are in Alberta. We define this by the large number of producers pushing 30 pigs per sow with low wean to finish mortality. With many of Alberta’s producer customers of Genesus we see their production numbers are able to compare with other areas and countries we do business.

Alberta like most of Canada exports approximately 70% of its pork production. This makes the world pork market dynamics a big factor in the industry.

In the past year, China decreased pork imports. This has made other countries I.E. Japan, Korea, and the Philippines battleground for global pork exporting countries. This has led to a challenging situation for not only Alberta but all Canadian Pork Producing and Packers dependent on importing countries. In our opinion, the effects have been negative for all Canadian Packers with some losing significant money. Producers need strong packers to continually upgrade facilities and fund domestic and export markets.

Alberta like most of the world has suffered from high feed costs driving up the cost of production. We observe 2022 has been a good year for producers that grow their own grain. The whole farm income has been good with the business model, grow feed, manure on land, feed pigs, and own appreciating land. Many producers in Alberta have this scenario. In North America, we expect 80% of pig production is buying feed.

Also last week Maple Leaf Foods – Lethbridge, Alberta plant had its annual producer meeting. The Lethbridge facility focuses on high-quality pork for premium export and domestic markets (Lethbridge Heritage brand). High-quality pork with the best eating attributes. Maple Leaf Foods Lethbridge is unique in an award program recognizing producers who deliver pigs that have quality. We believe it’s the only plant that does this in North America. As all readers of this commentary are aware we believe that our industry should produce better-tasting pork to grow demand. Genesus Genetics program is to do just that. The Lethbridge plant is supplied by a high percentage of Genesus – Jersey Red Duroc hogs. Obviously, we were pleased when the Quality awards were presented to the top 3 herds. All Genesus full genetic program Jersey Red Duroc x Genesus Female. We congratulate Neu Muehl colony, Rock Lake colony, and Elmspring colony. All herds push 30 pigs per sow. Production and Quality are a necessity for competitiveness.

Also, this past week we toured the Lacombe Research Facility in Lacombe, Alberta. Lacombe is the Canadian government’s meat research centre for Beef and Pork. They raise Beef cattle and have a farrow to finish unit stocked with Genesus Genetics. At Lacombe, they undertake research on farm in on site abattoir and with various meat quality measuring protocols with world-class equipment. Genesus is collaborating on several projects with Lacombe with the goal to produce ever-better pork. As the only Canadian-owned swine genetic company it is appreciated our opportunity to work with Lacombe and their world-class facility.

Other Observations

U.S. sow slaughter in October was 266,000, a year ago 246,000, a 20,000 increase. A year ago, the U.S. breeding herd decreased by 65,000 September 1 – November 30. We expect the U.S. breeding herd is decreasing this quarter. Less Sows = Less Pigs = Higher Prices.

At a recent NSIF Conference Mike Tokach a recognized global expert on swine production gave a presentation of Iowa State research. The study determined that a 1% change in wean to finish mortality is worth 82¢ to $1.20 a pig. With the U.S. wean to finish mortality records indicating an average of 9-10% the economic effects are huge. Using a wean to finish average value of $1.00 per head a 3% improvement would be $3.00 per head. 10,000 head = $30,000. Real money.

Let’s assume the U.S. sow herd is lower so is the market hog inventory. We believe lean hog futures for the summer circling $1.05 lb. are undervalued. We expect lean hogs at $1.20 in the summer of 2023 will be a reality.

Jim Long presentation at the Alberta Pork Annual General Meeting

Inside the lab at the Lacombe Research Facility

Inside the Lacombe Research Facility

Genesus pigs at the Lacombe Research Facility

Jersey Red Duroc

Genesus has believed for over two decades that as an industry we should be producing pork that is more marbled, redder, and juicier – Taste matters. Our Jersey Red Duroc continually dominates taste tests globally. The link below is Genesus’ Chef Glenn Mckenzie Smith preparing Genesus Jersey Red Duroc pork. If as an industry we are going to grow pork demand we need to deliver a better eating experience. When is it bad business to have a better product?

Click on the below link to watch Jersey Red Duroc – Pork Chop video:

USDA Confuses U.S.

Pork Commentary

Jim Long President – CEO Genesus Inc.

January 16, 2023

The December 1 USDA Hogs and Pigs Report indicated the market hog inventory at 66.966 million, a year ago 68.321 million. A 2% decrease year over year.

After seeing the 2% decline in inventory it was a surprise to us when we read the U.S. government’s quarterly Animal Product Production Report released last week.

Abracadabra – with a USDA report inventory of 2% less than a year ago, the USDA product report predicts 2% more pork in 2023.

You really wonder if USDA communicates within itself. There is absolutely no way the U.S. will have 4% more pork in the fourth quarter of 2023 compared to 2022. There is no scenario in the economics of this market that will lead one to believe in a 4% expansion. Negative producer margins, building costs, feed prices, labor issues, and the integrated model of owning pigs and slaughtering have been in the negative. We hear of capital calls and capital infusions to cover producer–packer integrated losses. This in no way leads to more hogs.

Now that we question the U.S. Animal Product report, we still show their predictions for Beef – Total Red Meat.

USDA projects U.S. Beef Production to decline by almost 1.8 billion lbs. in 2023 compared to 2022. Total Red Meat production (including our belief Pork is overestimated) down about 1.4 billion lbs. in 2023. USDA predicts steers to be $1.58 lb. avg. in 2023 compared to $1.44 in 2022. Hogs 2022 71¢ lb. 2023 68¢ lb. To us seems strange with 1.4 billion lbs. less beef the hog price of the other red meat would be lower year over year.

The main takeaway to us is less beef for sure, we would bet less pork. Total Red Meat production is down. Less supply in a U.S. population that grows every year. We expect exports to steady. To us, a scenario of strong prices as moving forward into 2023.

Other Observations

An article by the renowned MIT Technology Review (Massachusetts Institute of Technology) reports on PIC Gene Editing. An interesting part of the article on GMO-Gene Editing – PRRS.

“In experiments on pig cells, the Genus (PIC) researchers have tried many possible edits to the CD163 gene, looking for those that occur most predictably. Even with such efforts, the pigs being born have the right edit only about 20 to 30% of the time.”

Link to the full article:

https://www.technologyreview.com/2020/12/11/1013176/crispr-pigs-prrs-cd163-genus/

U.S. Carcass Cut Out

Last Friday

Pork Carcass Cut-out 81.64 lb.

Beef Choice Carcass Cut-out 2.78 lb.

Seems to us a huge spread between Beef and Pork Carcass prices. Beef is 3.4 times the price of Pork.

This tells us that consumers obviously will pay more for Beef. As a Pork Industry, we need to ask why. Obviously, consumers have the money to pay for the Beef, they are voting for Beef with their money. We expect the reason Beef sells for more is the eating satisfaction (taste) Beef has. On the flip side, the big discount Pork to Beef is a reflection of lower consumer demand.

If we are going to prosper as an industry, we need to figure out how to compete with Beef and pull our prices higher.

As many of you, regular readers know Genesus has worked diligently to produce Genetics with better taste. We can report seeing higher prices for better-tasting pork, consumers will pay for it, but it has to be better not just a story. We are seeing it in North America, Europe, and Asia. In some retail situations over $2 lb. premium to commodity pork. We need to make the pie bigger through a better product so everyone has a chance to get a bigger slice of that pie. Moving cut-outs to $1.20 is a lot better business than 81¢. We don’t think we will increase consumption and demand without an industry move to consistently better-tasting pork.

Next week we will be at the Iowa Pork Congress – visit us at Booth 1244 and or join us at the Genesus Reception on Wednesday evening.