By Justin Shepherd

Editor’s note: Justin Shepherd is Senior Economist, Farm Credit Canada (FCC). This article has been used with permission from FCC. For more information, contact ‘mediarelations@fcc-fac.ca’ or visit the ‘Knowledge – Economics’ section on FCC’s website.

After an unexpectedly strong 2025, things continue to look positive for the Canadian hog sector starting off 2026. Hog futures prices are near five-year highs and are well supported. After several years of weaker demand and oversupply globally, the hog market has become more balanced. With lower feed costs relative to a few years ago, margins look to remain well supported for producers.

Disease continues to be a concern for producers all over the world, with many pork-producing regions dealing with outbreaks of African Swine Fever (ASF), Porcine Epidemic Diarrhea (PED), and Porcine Reproductive and Respiratory Syndrome (PRRS). If Canada can continue to keep PED and PRRS under control, and keep ASF out of the country, producers can feel optimistic given strong hog prices and manageable feed costs. In this outlook, we examine what margins are expected to look like for the year ahead, and what domestic and international demand looks like for Canadian pork.

Hog prices supported by cattle markets

For 2026, our forecasts for cash hog prices across the country are slightly above 2025 and well above their five-year averages (Table 1). With cattle futures near record levels, this provides support for the hog market as a substitute protein. Demand for hogs is being fueled in part by domestic hog slaughter that increased in 2025 after multiple years of consolidation and is expected to be up slightly again this year.

While live hog exports look to remain steady to the U.S. this year, there is risk on the horizon as the Canada-U.S.-Mexico Agreement (CUSMA) is up for review, and as voluntary country-of-origin labelling (vCOOL) came into effect at the start of January. For now, these risks are being outweighed by the demand for Canadian hogs.

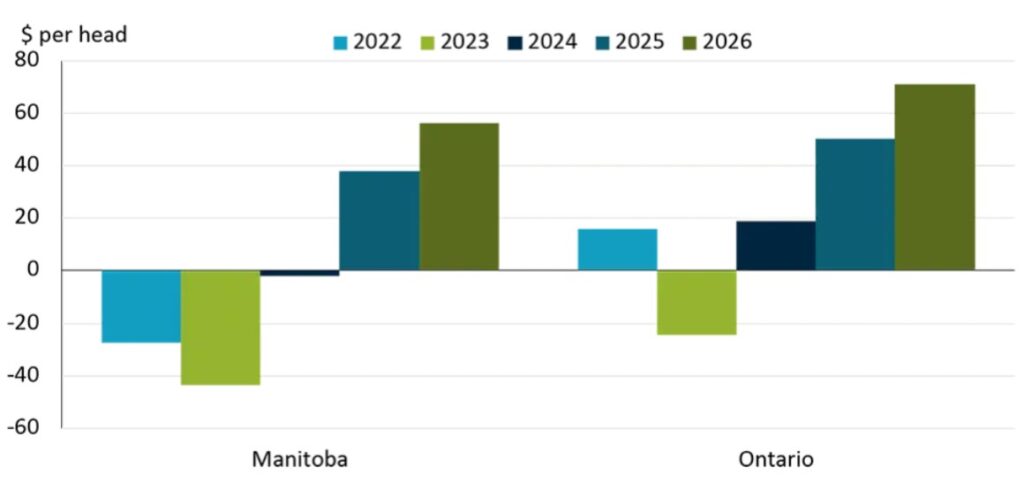

Hog margins benefiting from lower feed costs

Record Canadian crop production last fall is pushing grains and oilseeds down. Feed grain prices – including wheat, barley and corn – are expected to be steady or slightly lower, while oilseed prices are projected to decline due to high global stocks.

Large domestic supplies and market access restrictions on Canadian pulses to India are likely to result in additional peas diverted to the feed market and utilized in hog rations. This drop means cheaper peas, soybean and canola meals for feed, with ample supplies expected to hold feed prices below the five-year average throughout 2026. When we add in strong hog prices, it suggests Manitoba and Ontario farrow-to-finish hog margins could reach their highest levels in five years (Figure 1).

Canadian pork prices encourage consumers

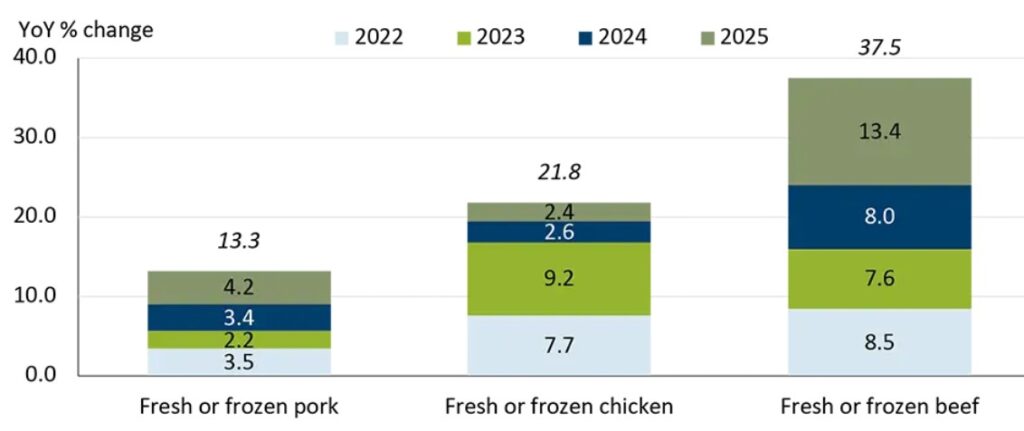

The price of pork at grocery stores is just one aspect to consider; it’s important to compare how it performs against alternative meats like beef and chicken. Since 2022, pork prices in grocery stores have increased by more than 13 per cent, but this rise pales in comparison to chicken and beef, whose prices went up nearly 22 per cent and 38 per cent respectively (Figure 2). Because pork prices have risen more moderately, that meat has become a more affordable protein choice for Canadian shoppers.

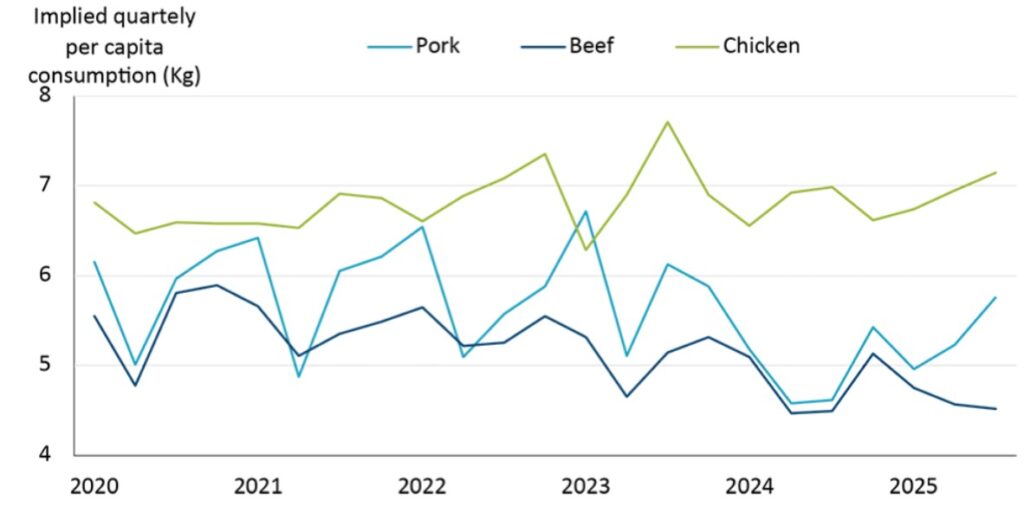

That at least partially explains the uptick in pork consumption last year – an encouraging development for the Canadian pork industry (Figure 3). Provided pork prices continue increasing less than other proteins, it is reasonable to assume continued consumption.

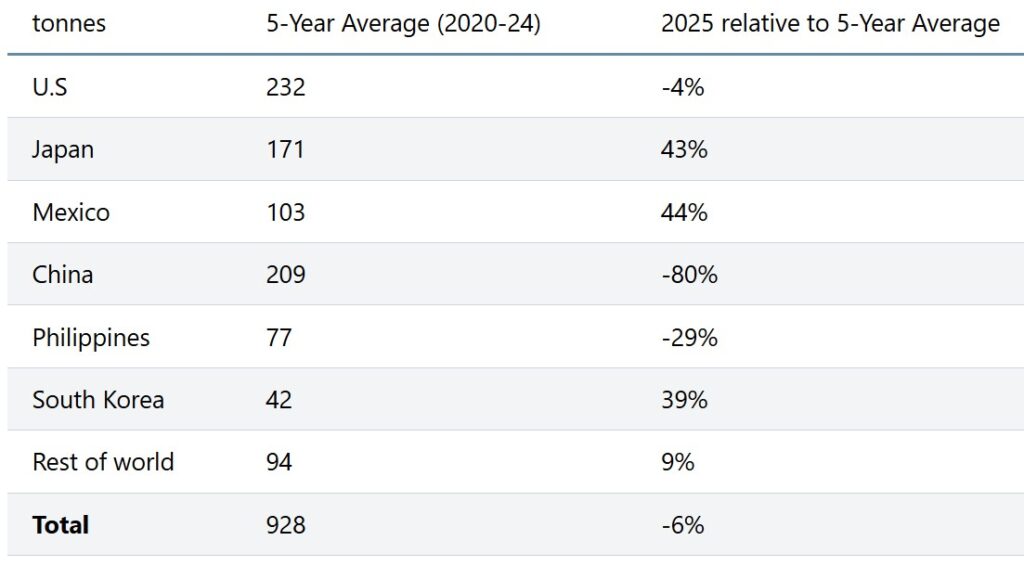

Canadian pork exports down through most of 2025

The Canadian pork industry is heavily reliant on exports, as more than 60 per cent of our pork production is exported. Through October 2025, Canadian processors exported six per cent less than the five-year average of 928 thousand metric tonnes (Table 2). This is highlighted by the large drop in shipments to China, part of which can be attributed to that country’s decision to impose a 25 per cent tariff on Canadian pork. Despite recent announcements of tariff relief for other Canadian agricultural products, pork has not yet been granted a reprieve.

Continued success is being found, however, in Japan, Mexico and South Korea, where Canada’s pork exports continue to grow at a solid pace. Trade to the U.S. continues to be strong and stable year-to-year, but as mentioned earlier, it remains a watch item for the second half of this year, as CUSMA discussions start.

Market access continues to be important

Unlike last year where trade concerns were an immediate issue that could potentially impact margins, this year we are expecting relatively smooth sailing through the first half of the year. Canadian hog production remains closely tied to exports to the U.S., and with disease impacts slowing herd growth stateside as well as restrained feed costs, it is creating strong margin opportunities.

The Canadian pork industry continues to make strides in growing export markets, while remaining hopeful for changes in the relationship with China. In other words, after weathering the storm of the past several years, producers are now in a good position to achieve solid profitability.