Pork Commentary, October 26th, 2020 Jim Long, President-CEO, Genesus Inc.

At the end of September, Pork in U.S. Cold Storage was down 22% from a year ago, 466,674 vs. 598,750 (1,000 pounds). This is quite positive for markets going forward. Less Pork in storage means buyers have less to pull from.

Other Observations

Last week the U.S. marketed 2,679,000 hogs, a year ago 2,690,000. The USDA Hogs and Pigs Report September 1st indicated 10% more hogs year over year. Almost 2 months gone and the hogs have failed to show up. Just like June USDA report, wrong, wrong, wrong. We doubt if anyone is keeping the hogs as pets.

Hog Market weights are running similar or lower than a year ago. If hogs backed up, we would expect year over year heavier hogs.

If in mid-August we had said U.S. Pork Cut-Outs would be in the 90’s in late October, most would have said that was “insane”. Fact is there are. A huge reflection of overall domestic and export demand despite weekly hog marketing’s in the 2.7 million range. If we can get 90’s now with 2.7 million it’s hard to believe that prices won’t be higher when weekly numbers go to 2.4 – 2.5 million in 2021.

We understand China back in market for split carcasses. Some plants geared up. This is a result of Germany losing China – Asia as an export market due to ASF.

The hogs going to market now were born in April. In our opinion everything from April to September created a scenario to lower the sow herd and production. As weeks go on, we expect to see year over year weekly hog numbers decline. This will be price supportive.

U.S. sow slaughter in September was 276,120 last year 238,300. An increase of 28,000. Year to date 2,508,400 a year ago 2,235,220. An increase of over 273,000 year over year. If anyone doubts there has been significant breeding her liquidation, they should review the sow kill. Also, from all we can observe sow death rates of 12% are at record levels, gilt retention has been low, and next to no new sow barns being built. Put it all together. Less sows to produce pigs.

The Chicken Little Economist who said in mid-August that the U.S. would produce more hogs in 2021 than 2020 had no clue what he was talking about. You have to wonder if there are vested interests tied to futures trading that see it in their interest to bad mouth the prospects of prices and supply to the detriment of hog producers but to the benefit of Big City future trading sharpies.

We hear about the benefit of the futures market. The U.S. has the only hog future market in the world. What’s the benefit? Most of the time U.S. has the lowest hog prices in the world. As my late friend Doug Maus often said, “Chicago: Las Vegas casino with no rules.”“In the casino, the cardinal rule is to keep them playing and to keep them coming back. The longer they play, the more they lose, and in the end, we get it all.” – Samuel “Ace” Rothstein_Casino movie –

Editor’s note: Dr. Sylvain Charlebois is a professor in food distribution and policy at Dalhousie University. He has authored five books on global food systems and has published more than 500 peer-reviewed academic journal articles.

Unlike what many analysts have said in the past, the food sector has never been recession-proof. COVID-19, however, may show us that it is in fact immune to deflationary pressures. And meat counter economics will matter more than ever.

Despite a negative inflation rate, recent StatsCan numbers are telling us that we are in for a wild ride at the grocery store. The numbers are also telling. While the general inflation rate sits below zero per cent, the food inflation rate is close to four per cent. In December 2019, Canada’s Food Price Report forecasted a food inflation rate of about four per cent for 2020, and this is very much where this year is heading toward. But COVID-19’s economic shock will likely be long-lasting and will affect grocery shoppers’ pocketbooks for quite some time.

In Canada, inflation has not been an issue for the past decade. It came close to four per cent in 2011, and that is about it. Not much excitement there. We have seen some decoupling between the general rate and food inflation before, but nothing like this. Over the course of this past summer, food prices increased almost four times more rapidly than the price of any other durable goods in the economy. Now, the Consumer Price Index is not reflecting the actual costs households are facing due to lockdowns. We are all consuming differently. Still, the difference between the two is huge.

Meat supply chain disruptions in March and April 2020 caused temporary product shortages in certain parts of the country, such as this Costco in Lethbridge, Alberta.

COVID creates initial meat shortages

In March 2020, the initial COVID-19 shockwave was real rather than financial, and it impacted industry and the rest of the economy directly. Food service, a sector which generates more than $90 billion of revenues a year in Canada, essentially disappeared almost overnight. Lockdowns forced the entire food industry to adjust quickly to a change in our economy. That shock was swiftly transmitted to the demand side, as households were hit by layoffs and lower incomes.

Financial markets were then hit hard by the uncertainty, not knowing when the pandemic and lockdowns would end – unlike other recessions where a slowdown is triggered by a shift in demand, which leads to subsequent market pressures to cut supply. That is what our textbooks tell us. COVID-19 is essentially a one-two punch to the system, whereas both sides of the economy, supply and demand, were hit hard. There is no textbook for that. The recovery’s sequence is hard to predict, with more than eight million Canadians who have applied for the Canadian Emergency Response Benefit (CERB).

Once confinement measures loosened up and Canadians could go out, shop, visit restaurants and do other normal activities to support the economy, the question was whether Canadians would show up. If lingering fears of contagion and of a possible second wave and uncertainty about household incomes prevail, the likely outcome is deflation or at least a price drop for most things. ‘Deflation’ is likely the scariest word for any economist. It is like cancer to an economy. Hard to end deflation and grow an economy when consumers know that what they want to buy today will be cheaper tomorrow. That could impact clothing, cars, houses – you name it. Taxes will go up, putting more pressure on consumer demand.

Food differs from other products

Food will likely buck the deflationary trend for an extended period. Unlike what many analysts have often said, the food sector is not recession-proof, as consumers will either trade down or will not go out as much. But with COVID-19, nobody has been going out to restaurants, and consumers have not really celebrated their lockdowns over caviar either. Most of us went back to basics: cooking, baking and making bread. Consumer demand now has a COVID-19 benchmark. Deflation or not, we need to eat.

Yet, on the supply side, COVID-19 is making everything more expensive to produce, process, distribute and retail. New cleaning protocols, higher salaries and building infrastructure for e-commerce will all cost more. Plant shutdowns and food safety issues are the last things the food industry needs. With online shopping becoming more popular, delivery costs will also need to be covered by consumers, whether we like it or not. Food has always been a high-volume, low-margin business, and that is not going to change. For industry, covering the cost to produce and distribute food, and asking consumers to pay more, will not change either. COVID-19 is impacting the entire planet, so we cannot import our way out of this scenario either.

As a result, we could see the average Canadian family devote a much greater percentage of their budget to food. Pre-COVID, roughly nine per cent of our budget was devoted to food. It is one of the lowest percentages in the world. That could rise to 11 or 12 per cent by 2022. In fact, given lockdowns, that percentage is likely much higher right now. In comparison, Americans are at six or seven per cent, whereas Europeans will spend about 15 per cent. Their percentage will likely change as well. In 1970, Canadian households were spending 21 per cent of their budgets on food. So, in a sense, we are going back in time.

The latest StatsCan data shows how retail meat prices quickly climbed between March and June 2020, with a slight decline starting in July.

COVID helps dictate buying trends

As for meat counter economics, things may get interesting. Early signs suggest consumers are not giving up on meat. In fact, 91 per cent of Canadians still eat meat regularly, based on recent polling data released by the Agri-Food Analytics Lab at Dalhousie University. With the regular trifecta of meat products, which includes pork, chicken and beef, consumers will continue to visit the meat counter, but with much tighter purse strings. With beef prices going up since January, we are expecting Canadians to consider chicken and pork as budget-friendly options. Chicken has been a stable option for years, but pork could also become the product of choice for the next little while. Beef will likely remain popular, but price will be an issue for families financially challenged by the economic downturn.

Simply put, current food economics are overwhelmingly forcing us to revisit the social contract we have with food, perhaps for the betterment of society. Valuing food, especially meat products, has only positive socio-economic implications.

Current food economics are making us more attuned to what is happening around us food-wise. It is also making us more food-literate. Such a shift in food prices is relative to what else is going on in the economy and will leave many behind as food insecurity levels in many parts of our country will soar.

Single parents, children and underprivileged demographic groups will require more attention as we embark into a new food era. Animal proteins, one of the most significant misunderstandings in modern agriculture, could get a boost by renewing its relationship with consumers. Our rural/urban divide has generated significant disconnects around major issues like GMOs, processed foods and, yes, animal production. The market could open up to a more traditional case, which suggest that animal production is very much part of sustainable agricultural systems.

While meat on the retail level has been a roller coaster for consumers in the past few months, Canadians still want meat, and home cooking is driving families to become more frugal in their habits, such as freezing meat.

However, there is a silver lining: since the beginning of COVID, even if food prices have been rising, most households are spending less on food. Each household in Canada is saving approximately $5 a day by just cooking at home and avoiding restaurants. That is roughly more than $600 since the beginning of the pandemic, which far exceeds price hikes shoppers needed to absorb during the same period.

Any way we look at it, COVID-19 will have a long-lasting impact on our relationship with food, and no-one is immune to that.

Canada’s Chief Veterinary Officer, Dr. Jaspinder Komal (centre), met with his counterparts from Mexico and the U.S. in April 2019 as part of an international ASF prevention forum.

As all those in the Canadian pork sector know very well, African Swine Fever (ASF) is not found in Canada – nor anywhere in North or South America for that matter – and a huge amount of activity is occurring to keep it that way. This serious pig disease, endemic to Africa, is already found in many locations so far in the Asia-Pacific region, the Caucasus region, eastern Europe and Russia. It was present in wild boar in Belgium until April 2020, and it was first discovered in wild boar in Germany in September 2020.

In April 2019, the Canadian Food Inspection Agency (CFIA) hosted a seminal international forum on ASF entry prevention, and ever since, CFIA, Canada Border Services Agency (CBSA), Swine Innovation Porc (SIP), the Canadian Pork Council (CPC), Canada Pork, provincial agencies and governments and other stakeholders have been working hard on various prevention initiatives.

Canada’s Chief Veterinary Officer, Dr. Jaspinder Komal, explained that, after the forum, a risk assessment was conducted. The biggest potential ASF entry threats were found to be meat products brought into Canada by individual airline travellers, illegal imported shipments of pork from infected countries, imported feed ingredients (especially illegal ones) and insufficient on-farm biosecurity protocols.

“It’s important that people realize that not only can the virus travel in meat products or feed ingredients, but it can survive on clothes and shoes,” said Komal. “This makes it very important that no international visitor who has recently visited a farm in another country visits a farm for two weeks after they arrive back in Canada.”

CFIA is working with CBSA and the travel industry both here and around the world to reach air travellers in a variety of ways about ASF entry prevention (the ‘Don’t Pack Pork’ campaign) and the importance of declaring all food, plant and animal items. These include signage that is seen on airport screens and airlines providing in-flight announcements to passengers upon landing in Canada. CFIA and CBSA have also placed posters at 18 Canadian airports in 16 languages and asked international airlines to post them as well. CBSA provides an ASF pamphlet to travellers who indicate that they have recently visited a farm.

“We also had a very focused campaign for the winter holiday season, from December 2019 to February 2020, and it worked very well,” Komal added.

The ‘Don’t Pack Pork’ campaign features multilingual signage and information at airports across the country as a way to deter international travelers from bringing potentially ASF-infected pork into Canada.

Online outreach through the CBSA and CFIA websites, along with social media, is ongoing. Relevant ASF operational updates are communicated internally to appropriate staff both in Canada and overseas at airport authorities and airlines. Federal funding provided in 2019 is also enabling CBSA to implement 24 more ‘Detector Dog Service’ teams, which will bring the total to 39 teams focused on agricultural imports by 2024.

Other governments of ASF-free countries are doing similar things. In December 2019, for example, the Australian government announced $66.6 million in funding for more biosecurity officers, six new detector dog teams, new scanning equipment, development of mobile technology to issue infringement fines on the spot and more.

With all this in place, it would have been easy to see if the message was getting through to airline passengers, but the emergence of COVID-19 resulted in the severe curtailment of international travel. However, CBSA notes, from January to August this year, 285 travellers entering Canada failed to declare pork products. Of those, 197 received a $1,300 penalty. Meanwhile, there were no reported cases of product importers who failed to follow the proper protocols. In all of 2019, almost 600 travellers failed to declare pork products (506 received a $1,300 penalty) and another 167 failed to properly import pork products (132 received a $800 penalty).

An ounce of prevention is worth a pound of cure

A Standing Group of Experts on ASF was formed in 2019 to help ensure collaboration, coordination and capacity in the region to prevent the entry of ASF. Komal chairs the group and says that its formation was a key recommendation from the ASF Forum hosted in Canada in April 2019. The standing group helps to ensure key areas for action are advanced, as defined in the framework developed during the forum. Komal also holds multiple ASF-relevant positions at the World Organisation for Animal Health (OIE) and is president of the Regional Steering Committee for the Global Framework for Transboundary Animal Diseases.

Here in Canada, there is the ASF Executive Management Board, a collaboration formed last year between government and industry. It spearheads the pan-Canadian Action Plan on ASF and has allowed, said Komal, “us in the government to work closely with industry members to make collective decisions. We meet every two weeks to continue developing and implementing the Action Plan. This includes preparing frontline workers to do testing for ASF if it appears a pig has the disease. At the CFIA lab in Winnipeg, we are working in collaboration with scientists in Vietnam and with funding from the Swine Health Information Centre in the U.S. to develop a non-invasive rapid diagnostic tool involving saliva.”

So far in the development of this tool, testing of saliva taken from a rope hung in a pen with ASF-positive pigs has provided good accuracy, but evaluation needs to be done in commercial conditions to see if this accuracy holds. The work on the pen-side test kit, Komal explained, has involved things like ensuring reagents would store at ambient temperatures. There is now an agreement with a company to mass-produce the kit, and they are expected to be ready sometime in 2021.

‘CanSpot ASF’ is Canada’s new ASF surveillance program.

To improve Canada’s ability to detect ASF should it enter our borders, a program called ‘CanSpotASF’ has been launched to enhance surveillance activities. Risk-based early detection testing at approved laboratories is the first new surveillance tool to be implemented as part of CanSpotASF.

Development of rapid ASF testing is also part of SIP’s current research priorities, announced in May 2020. After the 2019 forum, SIP had invited various Canadian and U.S. swine health experts to form the Coordinated ASF Research Working Group, which includes Dr. Egan Brockhoff, a swine veterinarian in Alberta who is also the CPC’s veterinary lead. Other working group research priorities include biosecurity (including control of wild pigs, which could potentially spread the disease over large areas of Canada), and in the event of an outbreak, the destruction and disposal of infected pigs and the ensuing economic impact and recovery phase.

Brockhoff noted that there is no evidence to suggest ASF is present in Canada’s wild pig population, but a working group that is developing ASF surveillance options for Canada may include wild pigs.

The CFIA has also formed the ASF National Emergency Operations Centre, which can create scalable regional command structures and holds national simulation exercises to ensure that the response to an ASF outbreak in Canada would be smoothly coordinated. Some of these simulations are done in partnership with U.S. authorities.

“We recently went over roles and responsibilities in terms of who makes what decisions,” said Komal. “And we are planning a simulation involving movement of pigs.”

Vaccines and antivirals for ASF are also being tested and developed, as announced in January 2020, at the University of Saskatchewan’s Vaccine and Infectious Disease Organization-International Vaccine Centre (VIDO-InterVac).

ASF brings major trade implications

On the export front, Canada has re-confirmed established reciprocal ‘zoning arrangements’ for trade of pork with the U.S. and the European Union. This means that, should there be an ASF outbreak in Canada, export of pork can continue from non-infected zones once zones are established in Canada and the importing countries accept the zoning decisions made by Canada. Trade zone arrangements are also being sought with Japan and some other Asian countries.

Brockhoff explains that, in addition, ‘compartmentalization’ guidelines are being worked out by the OIE, and various countries, including Canada, are working on the development of compartment standards.

“It’s management-focused and not geography-focused,” Brockhoff explained. “That is, a group of vertically integrated producers working under the same biosecurity, traceability and surveillance management system would still be able to export pork even though their ‘compartment’ is located within an ASF-infected geographical zone.”

Komal noted, however, that if the international guidelines for this concept that are currently being developed are not accepted by trading partners, the pork from a compartment within an infected zone in Canada could only be consumed domestically.

“I think we’re getting there with the U.S. and Europe at least,” Komal said. “But zoning is the primary tool to ensure trade continues.”

Producers should pay attention to feed risks

The Canadian Pork Council (CPC) has ASF resources available for producers of all sizes, veterinarians and the food service industry.

It was back in early 2014, when porcine epidemic diarrhea (PED) first arrived in Canada, that it was determined the virus that causes the disease had been transmitted through imported feed. Studies were later done in the U.S. on many other pathogens, including ASF, and it was confirmed that the ASF can easily be transmitted through feed. In response, the CPC has listed pig feed ingredients according to risk of ASF and provided feed storage time and temperature recommendations for producers. Komal has recommended that producers should look for feed made at mills that belong to the FeedAssure Program. By April 2019, CFIA had placed additional import controls on plant-based feed ingredients from countries of ASF transmission concern.

A big development on the feed front came this year in July, when U.S. scientists published results showing that 14 commercial feed additives can mitigate the presence of Senecavirus A, PED and Porcine Reproductive and Respiratory Syndrome (PRRS) in contaminated feed. The products include essential oils, organic acids, fatty acid blends and formaldehyde-based products. Pigs on supplemented diets had significantly greater average daily gain, significantly lower clinical signs and infection levels, and numerically lower mortality rates compared to non‐supplemented controls. Tests of these products on mitigating ASF are being conducted now.

ASF prevention going forward

Looking ahead at the future of ASF prevention in Canada, Komal, Brockhoff and many others believe the unprecedented measures to keep Canada ASF-free must continue.

“Given the seriousness of this disease, I think it will remain in the forefront of transboundary animal disease prevention efforts,” said Komal.

Disease is a major contributor to increased costs in the swine industry. For example, the cost estimated from the Porcine Reproductive and Respiratory Syndrome (PRRS) disease alone is $664 million annually to the U.S. swine industry (year 2012 estimate), with 45% of this cost attributable to the breeding herd and 55% attributable to the grower/finisher herd (PRRS.com; Boehringer Ingelheim Vetmedica GmbH). The report breaks down the cost to a per pig basis, equating to $4.67 for every pig marketed in the U.S. If we consider the effects of other global swine diseases, the cost is much higher. Therefore, selection of pigs with improved disease resilience will significantly influence the swine industry`s ability to supply affordable pork products.

In a previous technical report, we shared Genesus’ perspective on genetic selection for healthier pigs (The Path to Genetically Healthier Pigs). Disease in swine is not likely to disappear. It is probable that mitigating the impacts of disease pressure will become more challenging due to geographical spread of currently identified pathogens, and mutation of existing strains into new.

Our intent is to identify pigs within Genesus breeds that are naturally more resilient to pathogen challenge and allow them to pass their desirable genes on to the next generation of selection candidates. This strategy results in the inclusion of an additional component to the breeding objective of Genesus purebred breeds, and a path toward genetic improvement for disease resilience.

One potential method of implementation is by placing selection emphasis on antibody response. The immune system elicits an immune response when an antigen is introduced. The level of immune response mounted within the individual can be measured from blood. Heritability is an estimation of the amount of control that genetics has in the expression of a phenotype and is estimable only when known pedigrees or genotypes accompany the phenotype. In a challenged environment, antibody response showed moderately high heritability (h2 = 0.45 ± 0.13) on Genesus grandparent females (Serão et al., 2014), which suggests this trait will respond to genetic selection.

In the same study, large and favorable genetic correlations (rg) between antibody response and reproductive outcomes were discovered, which were much higher than their phenotypic correlations (rp) (Table 1). A secondary study where the Genesus population was used in cross-validation supported these initial findings, reporting heritability with a range of 0.28 – 0.47, depending on the data used (Serão et al., 2016). A later study using a separate F1 female population reported a similar heritability for vaccine response (h2 = 0.34 ± 0.05) (Sanglard et al., 2020).

Together, these results indicate that antibody response to PRRS vaccine is under genetic control and can be used as a predictor of reproductive performance under PRRS challenge. These conclusions point to this approach as a potentially effective strategy to select pigs with improved disease resilience.

Table 1. Phenotypic (rp) and genetic correlations (rg) with standard error (s.e.) between reproductive traits and antibody response under direct PRRS challenge (Serão et al., 2014).

Reproductive Trait

rp (s.e.)

rg (s.e.)

Number born alive

0.06 (0.05)

0.73 (0.24)

Number of stillborn

-0.07 (0.05)

-0.72 (0.28)

Number of mummies

-0.04 (0.05)

-0.66 (0.28)

The clean environment within nucleus herd settings does not present a challenge-type environment suitable for measuring resilience phenotypes, and vaccination for many diseases is not an option. However, vaccination is a common practice in commercial farms, and the timing often coincides with the timeline required to capture data for implementation of genetic selection. The isolation of incoming replacement gilts allows for the measurement of Ab response from vaccination, as incoming replacement gilts are typically health-tested to ensure no disease is present prior to introduction into the sow farm.

Previous research discovered that PRRS-infected and PRRS-vaccinated animals show similar antibody responses (Ellingson et al., 2010). The level of antibody elicited within an individual serve as the phenotype. Therefore, genetic selection under vaccine challenge will mirror selection under a direct challenge. Associations between Ab response and other reproductive and sow productivity traits are then estimated to establish the basis for genomic selection for disease resilience.

Obtaining phenotypes from environments outside the nucleus herd is important to the advancement of purebred populations. Genesus is acquiring genotype, phenotype, and pedigree information from commercial farms. Employing antibody response phenotypes in a genomic evaluation of purebred relatives provides an additional phenotype to aid in genetic improvement toward healthier pigs.

References Ellingson, J. S., Weng Y., Layton S., Ciacci-Zanella J., Roof M.B. and Faaber K.S. 2010. Vaccine efficacy of porcine reproductive and respiratory syndrome virus chimeras. Vaccine 28:2679–2686. Global PRRS Solutions; PRRS.com; Boehringer Ingelheim Vetmedica GmbH

Sanglard L.P., Fernando R.L., Gray K.A., Linhares D.C., Dekkers J.C., Niederwerder M.C. & Serão N.V. (2020). Genetic analysis of antibody response to porcine reproductive and respiratory syndrome vaccination as an indicator trait for reproductive performance in commercial sows. Frontiers in genetics.

Serão N.V., Matika O., Kemp R.A., Harding J.C.S., Bishop S.C., Plastow G.S. & Dekkers J.C.M. (2014) Genetic analysis of reproductive traits and antibody response in a PRRS outbreak herd, Journal of Animal Science. 92: (2905–21).

Serão, N. V., Kemp, R. A., Mote, B. E., Willson, P., Harding, J. C., Bishop, S. C., Plastow, G. S., & Dekkers, J. C. (2016). Genetic and genomic basis of antibody response to porcine reproductive and respiratory syndrome (PRRS) in gilts and sows. Genetics, selection, evolution : GSE. 48(1), 51.

Pork Commentary, October 19th, 2020 Jim Long, President-CEO, Genesus Inc.

Successful Farming yearly does a list of the Top 40 swine producers in the U.S. It’s a regional survey compared to the Global Mega Producer list that Genesus sponsors which covers the world.

What we found interesting in this year’s U.S. Powerhouses list is the decrease of the total sows by 61,475. We expect this is the first time the list has decreased since it has begun. The 61,475 decrease also doesn’t include the 55,000 Maxwell Foods is liquidating as their name wasn’t included in the 2020 list although they were on the 2019 one.

The USDA on the September 1st USDA Hogs and Pigs Report indicated the U.S. sow herd expanded last quarter. We totally disagree. We believe the herd has decreased. The drop in the Pork Powerhouses sow numbers is another example of what has happened to our industry. Financial losses cut inventory, big doesn’t make you immune from the realities of the marketplace.

Of note U.S. sow slaughter continue to run at liquidation levels, over 65,000 a week. A few weeks over break-even in finishing hogs gives help and some hope, but not filling the massive hole created by the pandemic debacle.

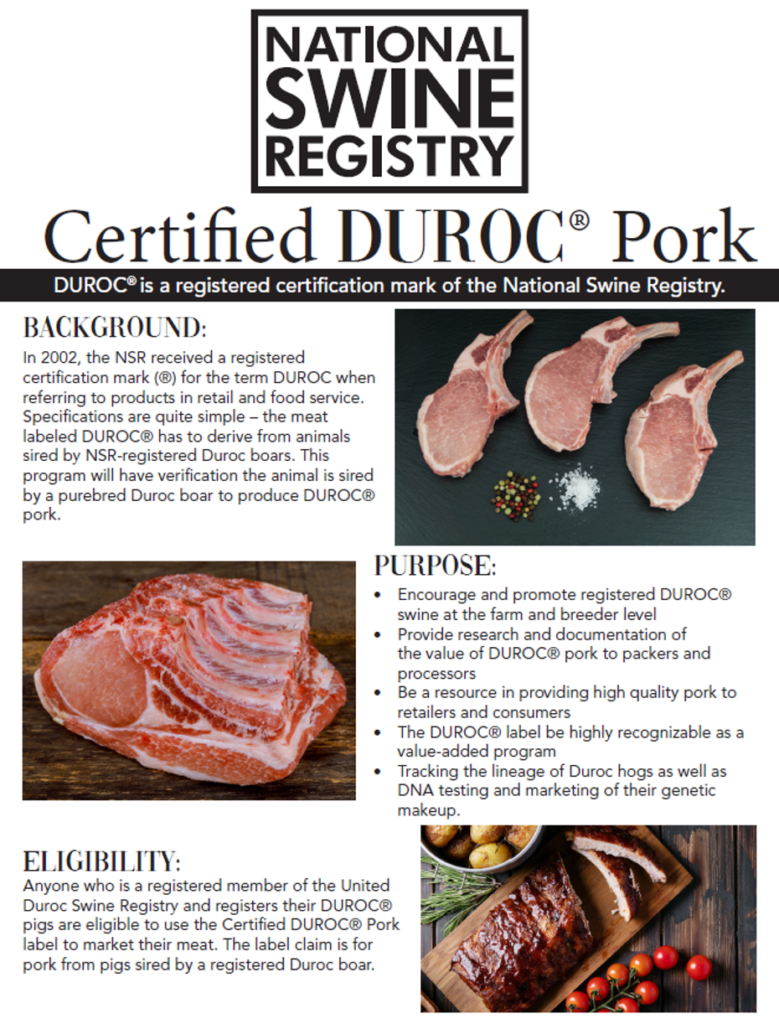

Certified Duroc

Thanks for the feedback last week in regards to our commentary on Certified Duroc. Your comments supported our belief that greater Domestic Pork Demand can be unleashed by producing pork that meets and exceeds consumers’ taste and flavor. It will be a challenge but as pork producers we are used to challenge. As an industry we need to put the marketing disaster of “The Other White Meat” program behind us and focus growing domestic per capita consumption. Ford move on from Edsel, we need to move on from “The Other White Meat” program.

“Failure is simply the opportunity to begin again, this time more intelligently.” – Henry Ford

An example of the mindset of our industry that we have to overcome was a discussion last week with a U.S Packer representative. He explained that they sort the best pork for Japanese Export (Best pork is redder and more marbling). They then do another sort for some foodservice. The leftovers go to the U.S. domestic market.

This mindset will never increase domestic consumption. What other business knowingly send lower quality product to its major customer? It’s like U.S. consumers are second class citizens. Maybe if the best pork is redder pork and has more marbling, we should figure out how to have more of that type of pork to grow demand. Would it be a Common Sense Revolution producing a product that meets consumers demand for taste and flavor, more domestic demand will increase producer profits.

To clarify from some questions we had last week re qualification for Certified Duroc Program. You must use an NSR registered Duroc boar to legally use Certified Duroc Label. We were asked if this precludes PIC and DNA Durocs from label use. Some had been told by PIC and DNA that there Durocs would soon qualify, indeed there were efforts to have rules that would have allowed their participation. It’s obvious the success of the Certified Angus Beef program has swine genetic companies wanting rules diluted so they could be part of Certified Duroc. In the end the breeders of NSR reconfirmed that only NSR registered Durocs qualify for use in the Certified Duroc Program.

Durocs that cannot prove they have a purebred history will not, Mongrel Durocs will not. PIC and the like will be able to join if and when they have a purebred registered Duroc in NSR. Genesus produces Globally 83,000 registered purebred Durocs annually. We believe that to be a true Duroc it needs to have the lineage proof that registered Durocs program affirms. Many Durocs of breeding companies are not pure but synthetic lines with other breeds mixed in. Of the world’s major Genetic Companies only Genesus has a program for all breeds that affirms registered purebred breeding stock. To reiterate to be part of the Certified Duroc Brand you must use an NSR registered Duroc.

“If you are not a brand, you are a commodity.” –Philip Kotler

By: Everestus Akanno, PhD., Geneticist, Genesus Inc.

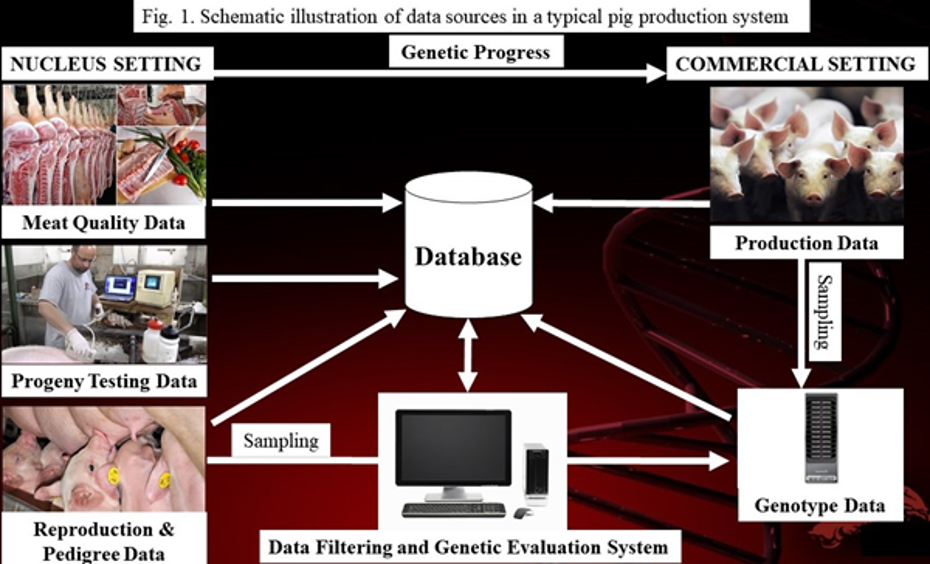

The success of pig genetic improvement programs depends heavily on the continued generation, collection, and analysis of industry-wide data from both the nucleus and commercial settings.

These data come from a variety of sources including progeny test facilities, packing plants, nucleus and commercial barns, and DNA laboratories (Fig. 1) which are typically characterised by a fast-paced work environment where data generation and collection happen quickly and continuously and people may not have data accuracy as their top priority, thus, creating room for possible errors. In addition, advancements in technology and computation have allowed for automation of data generation and integration into a remote database which can reduce potential errors. Nevertheless, questions still exist on the quality and validity of industry-wide data for comparing cohorts, evaluating genetic merit, and making selection decisions.

What is data integrity?

In the context of genetic improvement programs, data integrity is defined as the extent to which data collected on an individual is complete, consistent, accurate and reliable for genetic evaluation purposes. According to guidelines provided by International Council on Animal Recording (ICAR, 2018), a complete and accurate record on an animal should have the following attributes:

Animal identification – The animal should be properly identified using any suitable identification methods.

Parentage verification – The parentage of the individual should be verified and trackable.

Dates of recording – The dates of birth and dates of measurements should be complete and accurate.

Phenotypic values – The value of the animal record of production or performance level should be within allowable published baselines for the traits and breed.

Systematic effects – Factors known to be associated with the record of performance for an individual should be noted and properly documented.

Issues with data integrity in pig production

Data collection and interpretation form the foundation for the many decisions made in the pig industry. Generation of significant amounts of data has become a normal part of the pig genetic improvement business, especially with the advent of genomic technology. However, human errors and failure of automated systems can compromise data integrity. Examples of potential issues with data integrity include but are not limited to the following:

Mislabelling of samples (e.g. for genotyping purposes).

Poor handling of samples during storage which may result in missing data.

Incorrect animal identification.

Incorrect assignment of parentage.

Error in data entry.

Failure in automated measurement systems leading to inaccurate measurements or a break in timed measurements (e.g. individual feed intake equipment).

Inaccurate ultrasound recording from inexperienced or untrained technicians

Efforts to mitigate these issues will go a long way to improve the quality and integrity of data used for genetic evaluation, thus, leading to more accurate estimation of genetic merit.

Measures to improve data integrity in genetic evaluation systems

As previously noted, mistakes in parentage assignment and in the linking of data (genotype or phenotype) to the right animals in the recording system can be very disastrous and undermine the predictive power of the genetic evaluation system. The most important key to data integrity is people. Staff that have a keen interest in and understanding of the importance of quality data are the most valuable resource to ensure data integrity. Therefore, data integrity needs to be frequently monitored by keeping a close eye on the following areas:

Data from various sources need to be verified and interrogated before integrating into the database.

All software that supports data collection, data processing and data reporting need to be regularly validated.

Access to the database should be restricted to individuals responsible for data collection and management.

All persons involved with data collection and analysis should be trained and maintain certification, as appropriate.

Quality control measures should be in place and automated to identify potential errors in data entry.

Data usage and analysis should include steps for identifying, visualising, and filtering erroneous data.

As a leading global pig genetic company, Genesus Inc. takes data integrity very seriously. Our dedicated staff consider data integrity as the highest priority. We continuously monitor data integrity and have established measures for identifying and excluding erroneous data from entering the database. In addition, the Genesus Genetic Team is continuously researching and developing novel approaches for improving the quality of data used in the estimation of genetic merit, thus, delivering the best genetics to our customers.

Pork Commentary, October 13th, 2020 Jim Long, President-CEO, Genesus Inc.

Last week the U.S. sold 60,200 metric tonnes of pork. The highest amount this year and the highest since early 2019. We expect the closing of German exports to Asia due to ASF is giving underlying support. Last week China sales were 29,000 mt. the fifth-highest amount this year. We expect to see continued strong export sales over the coming months as Asian demand and loss of German pork pulls more sales to USA-Canada.

Other Observations

The miracle of the fall of 2020 continues.

On August 18th October lean hog futures were 51¢ lb. Last Friday they closed at 78.125¢. That’s a $55 per head appreciation. Going from losing $30-35 a head to a profit of $20-25. What a turn around. Not anytime too soon. Some producers who 6 weeks ago were ready to pull the plug now see a future.

So many were discouraged by the constant drumbeat of the chicken littles who were telling them the negativity of the futures. They were ready to give up.

Case in Point last week we received the latest Iowa Producer Magazine from Iowa Pork Producers Associations.

Chicken Little 1 – “It’s shackle space that will dictate pig prices moving into the future, not the pig supply.” With that he said “it will likely be 8-10 quarters before the profit looks much better.”

Comment – No wonder producers were depressed and had little hope – 8-10 quarters?

Chicken Little 2 – He also thinks “the pork industry doesn’t see a recovery until at least 2022.”

Two Chicken Littles preaching doom and gloom as recently as a magazine delivered last week.

The funny thing is our check off dollars get used for there “experts” to give us know nothing crap.

“Talkers are usually more articulate than doers, since talk is their speciality.”-Thomas Sowell

The Tragedy of Pork Consumption

Since the ill fated “Other White Meat”program was launched 20 years ago, pork per capita consumption has flatlined. This despite total U.S. meat and poultry per capita consumption increasing by 30%. The reality is our Pork Industry has lost domestic market share. This has led us to push for exports as an “opiate” for expanded pork production.

The “Other White Meat” program was a push to make us like Chicken. A cheaper product. It must be the only marketing program in the history of advertising that tried to compare your product to a cheaper option. Bizarre. Obviously, the “Other White Meat” program failed a billion dollars (Check off) of producer money went into this losing plan.

The quest to make lean lean like chicken took away marbling that leads to taste. Loins and hams that once led the pork cut-out in price now languish behind bellies, ribs, shoulders. The destruction of loin and ham values (half the carcass) has hurt the profits of our industry for years. Consumers vote with their money. Not only they have decided to buy more other meats and poultry, they are voting bellies, ribs and shoulders which have more marbling and better taste. This is what’s winning the consumer dollars and preferences. Big Taste is the driver for repeat consumer purchasing. It’s been calculated if each American ate pork one more time a month it would lead to 7 million more hogs domestically consumed. That would be reliable domestic consumption and not one dependent on the vagaries of exports and the political issues that affect its reliability.

It’s one thing to rail against what’s wrong, but it’s more important to find solutions to unlock U.S. domestic demand. We all are aware of the run away success Certified Angus Beef and what it’s done for beef consumption and cattle producers. Fortunately for the pork industry the National Swine Registry (NSR) has trademarked “Duroc” for U.S. meat case. The Certified Duroc Program will be an option for producers, packers and supermarkets to use a program that through legal verification can brand a product that like Certified Angus not be a niche product but one that resonates to all consumers.

The best part of the Certified Duroc Program is that NSR stringent legal trademark requirements ensure that only Verified NSR Registered Durocs can qualify for use of the Duroc label. This quality control measure will ensure purity of the Durocs that will deliver the Big Taste and Flavor. Unfortunately for some Genetic companies i.e. (PIC, DNA) what they call Durocs won’t meet these stringent NSR trademarked requirements.

It’s a bright new day. A vehicle from NSR to drive domestic demand through a universal available Duroc brand with quality attributes for taste and flavor. Genesus is proud to be a member of NSR and have a Certified Duroc that will deliver Big Taste and Flavor needed to enhance domestic demand. As an industry, consumer demand ignited by Big Taste and Flavor is a pathway to better profits.

The Fall 2020 edition of the Canadian Hog Journal is here! I was first introduced as the incoming editor of the Journal in the Fall 2019 edition, so this makes it my official first anniversary.

While every new edition is an exciting accomplishment for me personally and professionally, more importantly, it is an opportunity to advocate for this industry that supports tens of thousands of jobs, millions of Canadians and billions of global consumers.

We should all take time to appreciate the good things in our lives, but I feel compelled to digress a bit. The 2020 calendar year certainly has felt like an eternity for all the wrong reasons, no thanks to where we find ourselves as a sector, and producers are still facing a long-term negative pricing situation. Being so close to this issue myself, from an investigative point-of-view, it can be mentally draining. Still, that feeling pales in comparison to the ongoing stress producers must manage on a daily basis.

It is my sincere hope that all industry representatives, including magazine editors, are doing the right things to help you navigate this storm with as little hardship as possible. That is our goal and duty. Our collective success or failure has wide-reaching implications for many people.

In the Summer 2020 edition, we continued to provide coverage of shared value concerns across the entire Canadian pork supply chain. And while it would appear there are some positive outcomes to certain discussions, lingering issues and adversarial relationships can be difficult to overcome. Drilling down on shared value, this edition considers the balance of marketing power between producers, processors and retailers, and how that has changed over time. Despite the discomfort, producers must keep fighting for fairness.

Processing plant protests continue to be a platform for animal activists, but now, support for farmers and truckers is starting to receive attention, as shown in this edition’s coverage of recent rallies.

On the disease management side, we provide an overview of activities taking place on the national level to combat African Swine Fever (ASF). While value-sharing and other contentious issues can divide stakeholders, ASF represents a universally respected threat, and we all have to be on guard.

On the food side, consider an expert’s opinion on COVID-19’s impact on meat retail. While grocer profits are up, so are consumer prices, thanks to more Canadians eating at home.

Research in this edition covers a study of genetic disease resilience in grow-finish pigs, how science is taking a bite out of feed costs and the cost of sow exercise.

Readers are always encouraged to drop me a line at andrew.heck@albertapork.com. I want to share your views in our ‘Letters to the editor’ section. Dialogue and understanding are the only way we can move forward, and we need a stronger chorus of voices to speak up if we wish to be heard. As it stands, it would seem our messages are getting lost somewhat in a world with so many competing interests, whether those represent ‘priorities’ or not. When push comes to shove, many may soon find out the hard way that food is not only a priority but likely the top one.

Letters to the editor

In reply to “Producer-packer tensions threaten viability” (Summer 2020)

“Why aren’t Canadian pig farmers seeing any benefit from the record-high pork export prices and volumes processors are benefiting from? The prices we receive for our animals are at a decade low. The pricing system is broken and needs to be fixed ASAP, or there will be no pig farmers left in Canada outside of Quebec.” – Mick O’Toole, Neerlandia, Alberta

In reply to “Producer-packer tensions threaten viability” (Summer 2020)

“Western Canadian producers could perhaps benefit from a pricing system like Conestoga has in Ontario, where their producers were being paid more than $2 per kilogram in mid-July, while others across the province were being paid $1.20, which is roughly $0.60 below cost of production. I have also heard about multiple producers sending their financial statements to packers like Sofina to try and get better prices, since the packers are making money like crazy right now.” – Jeremy Van Dorp, Woodstock, Ontario

In reply to “Producer-packer tensions threaten viability” (Summer 2020)

“This really looks like the end of the western Canadian independent producer as a previously viable part of our agricultural output. The circumstances are what make this almost unbelievable – that a commodity with increasing worldwide demand cannot be produced economically because of local pricing structure, rather than logistics, climate or other more obvious variables.

“This is a very western Canadian problem, and it saddens me to see independent producers choosing to downsize or exit the industry. Clearly there must be a space for all viable production. With the loss of one part of the sector, we lose production in the short term and the value of agri-business diversity overall. Not everyone can be, or desires to be, a global megaproducer, but both indeed have merit for different reasons. And there should be room for both, if both can find ways to access fair value in their product.” – Brent Taylor, Drumheller, Alberta

Editor’s note: Bijon Brown is the Production Economist for Alberta Pork. He is currently collecting and analyzing cost and pricing data to improve producer success. He can be contacted at bijon.brown@albertapork.com.

All business relationships contain a balance of power. In the western Canadian hog industry, over time, the power has swung from an equitable place for both producers and packers, to favouring packers and retailers.

Most will likely agree that a united front for producers is now more important than ever before to address the hog pricing situation. Concepts such as single-desk selling have largely gone by the wayside, as ambitious farmers more than two decades ago sought to outpace others around them, putting collective action aside in favour of high-octane capitalism. It was a good time to be in hogs, if you could compete, but since then, much has changed.

When the single desk was disbanded in Alberta, as an example, individual producers were now left to negotiate with a few packers, which became even more disproportionately skewed as the years went by. The tables have turned, and the negotiating power now resides with the packer. With very little government oversight on economic practices, packers have used this power to their advantage.

Packer power suppresses price

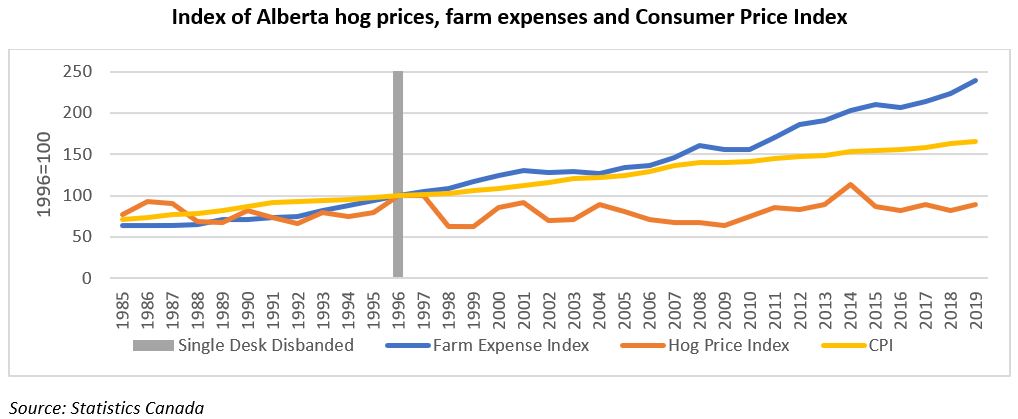

Lower hog prices, higher farm expenses and general inflation have all contributed to financial difficulty in the industry.

Cost of production is on the rise, along with overall inflation, but hog prices paid to producers have not increased. With the removal of the single desk, packers’ market power has driven down the ‘real price’ of hogs, which is the price that accounts for changes to the general cost of living. This has resulted in a considerably worse financial situation for producers.

In Alberta, the hog price index closely tracked the farm expense index until 1996, the year single-desk marketing ended. Since then, there has been a clear and growing divergence between the price and expense indices. Expenses in 2019 were more than twice what they were in 1996, while on the revenue side, the hog price in 2019 was lower than what it was in 1996. The same relative trend can be observed across the prairies.

With so few packers in western Canada, they can dictate the price in the contracts offered. Packers influence price through their ability to segment producers by individualizing agreements. This may be done by giving some producers more favourable rates or premiums than others based on volume, proximity or on any other desired basis. The inclusion of confidentiality clauses in contracts is also a component of market power. Market price uncertainty is generated because true prices are kept hidden. If producers cannot determine the true market price, how can they adequately negotiate better prices?

Improving prices requires greater unity

Negotiating power stems from producers’ ability to come together. The more producers are divided, the more power they give to packers, and the less control they have over prices.

How can producers unite? The notable and most effective option is to pursue the establishment of a single desk. Instead of being able to play hundreds of producers against each other, packers would need to deal with only one marketer that has producers’ best interests in mind, first and foremost.

The adoption of a single desk could shift the balance of power back to producers, resulting in a hog price that is more consistently favourable, though government support for this concept may be long gone. As an alternative to using the single desk, producers could consider coming together and forming marketing groups, some of which already exist.

A marketing group could sell and coordinate the distribution of hogs to the plants. For example, Hutterite colonies in Alberta currently make up more than 40 per cent of the industry’s core producers and own nearly half of all sows on-farm. If colonies were to form a marketing cooperative, then this could increase their bargaining power. Consolidated producer marketing means that a few packers would now be forced to compete on price for a larger volume from one source.

Packers’ economic model is driven by the number of hogs they can process in a day. Because they are still operating under-capacity in western Canada, the more hogs they can process in a day, the greater their profitability. If producers returned to collectively marketing their hogs, volumes would be more important to packers, and they would need to be competitive in their pricing to maintain their volumes.

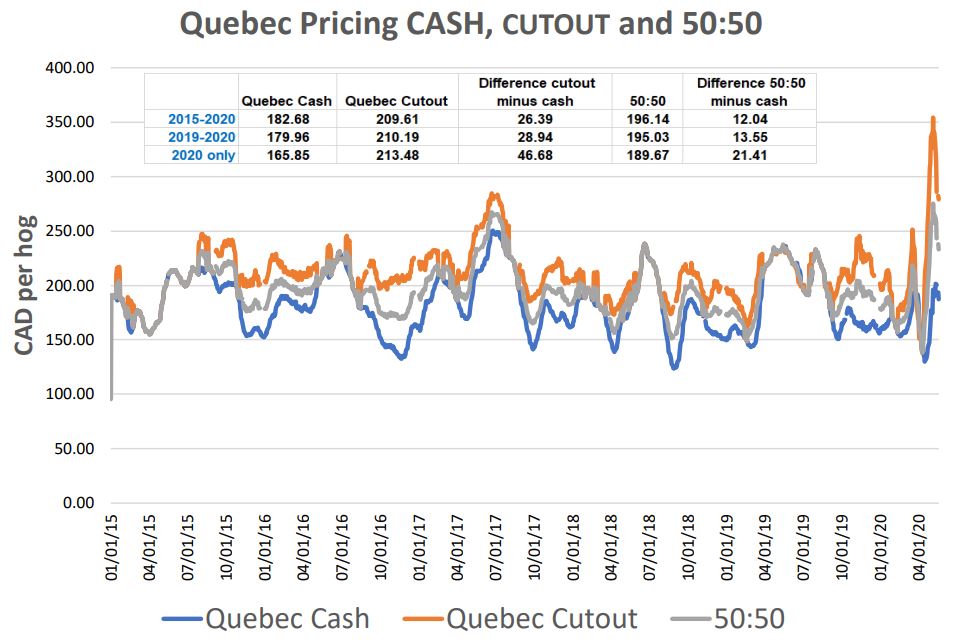

Quebec pricing model shows promise

Producer unity generates a more sustainable pricing model for Quebec producers.

The Quebec pricing model is perhaps the best example we have in Canada of successful consolidated marketing power.

Hog price discovery in Quebec has been governed since the early 1980s by the Quebec Hog Producers’ collective marketing plan, where producers collectively negotiate a sales agreement with packers. The Régie des marchés agricoles et agroalimentaires du Québec, which regulates marketing plans in Quebec, recently upheld the previous cut-out formula in which the cash price can vary within 90 to 100 per cent of the cut-out price.

Two things have contributed to better prices in Quebec: single-desk marketing and an objective arbitrator to mediate the situation when there is no agreement between both sides. Provinces outside Quebec have neither a single desk nor an arbitrator. Having a single desk makes it possible for an arbitrator to review proposals from both producers and packers. When producers come together with one voice, they can create a better pricing environment.

Producer unity creates a platform for change

Greater producer power can lead to a more equitable share of value in the supply chain. With more power, producers can negotiate changes to contracts.

The main consideration in contract pricing is the source of base prices. Currently, hogs in Canada are priced based on U.S. hog prices, which U.S. packers are required to report to the U.S. Department of Agriculture (USDA). While the hog industries in Canada and the U.S. are integrated to a degree, pricing suffers due to this unnatural linkage, especially when political gamesmanship and trade disputes are considered.

U.S.-influenced hog pricing can be a detriment to the western Canadian producer if the numbers are manipulated. The main argument in favour of U.S. pricing is that Canada competes with the U.S. in the global market, so it makes sense to measure ourselves against this large competitor. The method works, but only if fair pricing and cut-out value are considered on an even playing field.

The North American pricing model is broken. U.S. price signals have been impacted by politics, government subsidies and continued structural change. A made-in-Canada pricing solution that incorporates our export differences may be the only sustainable way forward if U.S. signals continue to distort the picture.

Producer-packer unity strengthens the entire industry

While much attention is paid to the relationship between the producer and packer, a third player, the retailer, should not be forgotten when it comes to understanding price disparity.

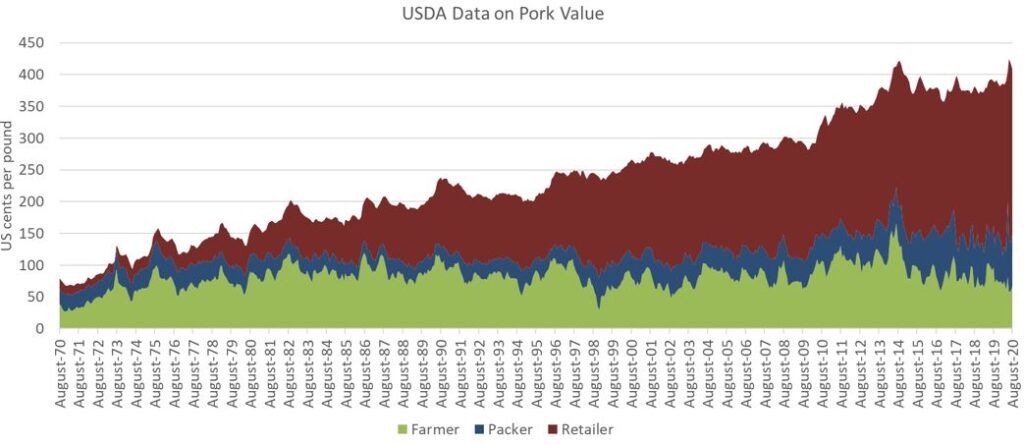

USDA data going back to 1970 shows how, despite predictable market fluctuations for producers and packers, on the retail side, value for pork has shot up nearly 500 per cent, which is not consistent with the price for pigs or wholesale pork. While the U.S. system is fundamentally different from how we should measure ourselves in Canada, it is the best existing benchmark we currently have.

Since 1970, pork retail margins have risen much faster than producer margins and even processor margins.

In 2019, most American farmers received less than $1 per pound for their pigs, while processors received nearly $1.50 per pound of wholesale pork. Meanwhile, retailers received close to $4 per pound for packaged pork sold in-store, and consumers have been paying upwards of $8 per pound, in some cases, to take that product home. The situation in Canada is very similar in that regard.

Nearly six per cent of product found in retail meat cases is wasted at the store level. This means, of the $4 retail price, approximately $0.24 is discarded. It may not seem like much, but if we could eradicate the waste and spread this benefit across the value chain, producers could receive almost $12 more per hundred kilograms of meat produced if just $0.04 of that $0.24 was passed back to producers, with the remaining savings benefitting other stakeholders.

What would drive such an incentive for change? One such impetus comes from producers and packers working together to lobby for consumer buy-in, as eliminating waste is known to be a consumer concern. Consumers should consider where their meat originates and whether their dollar is going to the right place – to pay hard-working Canadian farmers for the end-product that is possible only because of a longer-term commitment to raising pigs.

Taking the next steps toward fair pricing

When it comes to generating positive change across the value chain, greater producer action and packer collaboration are needed.

Producers need to ask: What steps do I need to take to shift the power back to an equitable place for both producers and packers?

Shared value, or lack thereof, has been on the minds of many producers these days.

In the Summer 2020 edition of the Canadian Hog Journal, we introduced the work taking place behind the scenes between western Canadian provincial pork producer groups and processors: “Producer-packer tensions threaten viability.”

In mid-May, the pork producer organizations in B.C., Alberta, Saskatchewan and Manitoba issued a joint invitation to executives from Donald’s Fine Foods, Maple Leaf Foods and Olymel to have an open and frank discussion on the state of the industry, and to work for solutions that create shared value for producers and processors.

“We appreciate the opportunity to engage in these conversions, as well as the time committed to the discussions,” said Darcy Fitzgerald, Executive Director, Alberta Pork. “We look forward to seeing tangible outcomes, and we will keep producers updated as the process continues.”

Initial meetings with all three packers took place virtually in mid-July and early August, with further commitments made to conduct additional meetings in the future. Following the meetings with Donald’s and Maple Leaf, the producer groups released a summary of their discussions and findings, which received a great deal of attention from across the supply chain. The initial meeting with Olymel was conducted following the release of that summary, approximately one month after the provinces had met with Donald’s and Maple Leaf.

Olymel demands CPE, rejects Quebec-style pricing

The Quebec pricing model has been looked upon favourably by many in the hog industry across Canada, but processors have been reluctant to adopt it.

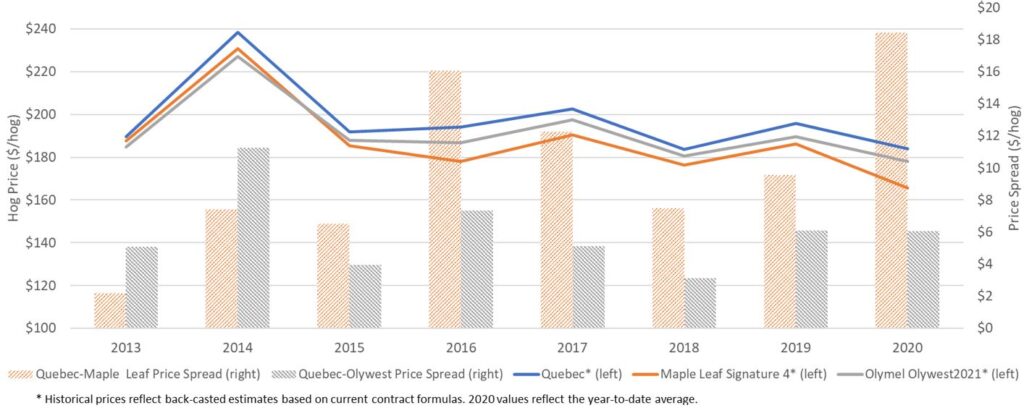

Notably absent from the meeting between the western producer groups and Olymel was Réjean Nadeau, President & CEO. However, Casey Smit, Vice President, Swine Production, Western Canada and Ian Moon, Manager, Hog Procurement, Western Canada were available to provide an overview of the company’s 2021 contract.

In late June, Olymel introduced its new contract, which includes a split between 50 per cent of the HM-LM201 price plus 45 per cent of the PK0602 cut-out value. A wider grid index and premiums are also offered on top of the calculated price. The contract addresses producer desires for cut-out value inclusion and helps reduce the negative pricing valleys, but the use of an index factor, common to most packers, takes away some of the price peaks, as does using only 90 per cent of cut-out in the formula.

A large caveat, however, is that the Olymel 2021 contract requires producers to be certified under the Canadian Pork Excellence (CPE) program. In western Canada, especially Alberta, CPE adherence remains very low following two years of deliberation between producers and packers, as highlighted in the Winter 2020 edition of the Canadian Hog Journal: “Quality assurance brings value, but who pays?” Training on CPE has not yet been delivered at all in Alberta, and it is being slowly introduced in Saskatchewan and Manitoba. The process takes months for producers to become fully certified, which could jeopardize their eligibility for the contract in the immediate future.

On a positive note, the new formula would only require a small change to create large gains and improve the industry outlook. For Olymel’s 2020 contract, also reflected in the 2021 contract, the company introduced bonuses for carcass weight, loin depth and proximity to the Red Deer plant. The proximity bonus has no official distance cap; however, it was suggested that anywhere farther than approximately 600 kilometres from the plant (about as far east as Swift Current, Saskatchewan) would not receive full compensation on distance. The 2021 contract increases the five-year average price over the 2020 contract price by $0.07 per pig.

Further to the contract discussion, the producer groups were disappointed to learn that Olymel had effectively shut the door to any consideration of supporting a ‘Quebec-style’ pricing system in western Canada, which could help alleviate some of pricing woes producers are experiencing.

The Quebec model uses an average value between a whole carcass value and the USDA cut-out value, taking a percentage of each to arrive at a final price. In Quebec’s 2019 to 2022 marketing agreement, that amount is a 50 per cent of each the whole carcass and cut-out. However, since the start of the COVID-19 pandemic, an ongoing dispute between Olymel and Les Éleveurs de porcs du Québec (Quebec Pork) has resulted in an adjustment, which currently uses 65 per cent of the whole carcass and 35 per cent of the cut-out. The decision to make the adjustment was the result of processor pressure.

Maple Leaf arrives prepared for serious discussion

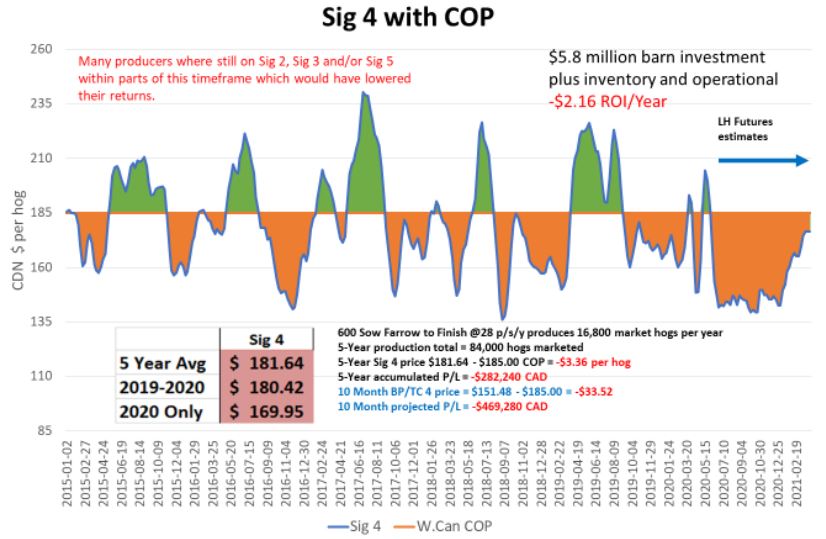

Cost of production acts as a benchmark for determining profitability. Even at a generous $185 per pig, the picture is not pretty for producers.

Prior to Maple Leaf’s meeting with the western producer groups, the company issued a letter to its producers offering $20 per pig for 13 weeks if an extension of one year was added to their current contracts. This interim help is appreciated but will not address the systemic pricing problem for producers in western Canada nor the large pending financial shortfall projected until May 2021.

During the meeting, some attention was paid to the western provinces’ cost of production figures. Because there are nuances between Alberta, Saskatchewan and Manitoba, a round number of $185 per pig was chosen as a benchmark to demonstrate producer losses across the three jurisdictions.

Maple Leaf officials questioned why the benchmark was set that high, but for the provinces, the number was an appropriate median between a rare, low-end cost of production at $165 per pig versus a more common, high-end $200 or more per pig. Anecdotal evidence from Manitoba suggests some highly efficient producers fall within that low-end range, whereas data recently collected in Alberta shows many producers sit closer to the high-end range.

The initial meeting with Maple Leaf proved to be an important extension of an olive branch between the two sides. Much discussion centred around competitiveness challenges for both producers and processors relative to their U.S. counterparts.

For processors, the Canadian producer’s disadvantaged spot also puts hog buyers in a tougher situation compared to U.S. processors. A main difference, however, is capacity: in the U.S., prior to temporary plant shutdowns due to COVID-19, processors were nearing 100 per cent capacity, with slaughter and export volumes at record highs. In Canada, the same cannot be said for capacity, despite a similar trend among U.S. and Canadian pork exports.

Due to increased supply in the U.S. this year, prices have been depressed. While that reality conforms to the laws of supply and demand, we have seen the reverse effect in Canada, where supplies have been lower than packer demand, but pricing is telling producers to reduce supply or even exit the industry, in some cases. For producers, in addition to negative pricing signals, an added difficulty surrounds the Canadian federal government’s lack of financial support relative to what U.S. producers have received in the past three years.

While shared challenges were discussed, so was market potential. Maple Leaf believes its corporate initiatives – such as ‘raised without antibiotics’ status and ‘carbon neutrality’ – have benefited the brand in the eyes of consumers. Producers, likewise, take care to adhere to quality assurance measures, though it is often unclear how those efforts translate into value back to the producer. Many producers would say the value is absent without any tangible strides to reward the production behaviours that brands are built upon.

Donald’s willing to work toward producer equity

During Donald’s Fine Foods’ meeting with the western producers groups, the company announced that it would operate a floor price of $1.40 per kilogram per pig over a four-week period to help address the current pricing situation while further options are considered for the future. An additional four-week period was announced thereafter, for a total of eight weeks. While this extra cash infusion is welcomed, unfortunately, the losses for producers continue to accumulate at a significant rate with little long-term support on the horizon.

Donald’s offerings amount to an extra $20 to $25 per pig in the short term, but there is no change to the current formula going forward. Donald’s formula is based on the Maple Leaf Signature 4, with the additional benefit of having transport costs fully covered. This helps ensure Donald’s maintains its largely out-of-province hog supply.

HyLife leads when it comes to producer support

HyLife was not included in the recent shared value discussions, given the company’s proactive steps to working with producers. While all western Canadian processors are looking to expand, HyLife is taking a balanced approach.

When it came to extending the shared value meeting invitation to packers, HyLife was excluded, albeit not out of disrespect. From the perspective of many producers, especially those who sell their pigs to HyLife, there is a lot of promise on the horizon for cooperation.

In April, HyLife met with the company’s independent producers to discuss the creation of a new hog pricing formula – one which utilizes the existing Chicago Mercantile Exchange (CME) whole carcass price, along with a new index factor, premium structure and weight-based grid, as well as incorporating a window price using USDA cut-out prices.

Concerned with the springtime shutdowns of pork processing plants in the U.S. due to COVID-19, HyLife decided to cushion volatility in the CME and cut-out price by implementing the new formula in a phased approach: If the CME price is between 90 and 100 per cent of the cut-out, then CME is the default, but if the CME price is greater than 100 per cent of the cut-out, the default is 100 per cent of the cut-out.

HyLife’s transition to favouring cut-out pricing is a clear demonstration that some processors in western Canada are willing to adapt in a way that is profitable for all. By implementing its new formula, HyLife is also demonstrating its willingness to address producer pricing concerns and strengthen relationships with producers who supply the company’s hogs. All things considered, HyLife’s new formula amounts to an estimated $20 per pig increase, indefinitely, over the previous formula.

Producers push for greater transparency

One of the major stumbling blocks in the pursuit of shared value so far has been transparency – between producers, processors and retailers.

In early March, Alberta Pork introduced the concept of a pricing calculator for producers in attendance at the organization’s semi-annual meetings across the province, with much encouragement expressed for the initiative. Not long after, work was undertaken to develop the tool, which is now allowing producers to compare their existing contracts with hypothetical conditions offered by other processors.

In mid-July, an eagerly anticipated hog pricing calculator was made freely available on the Canadian Pork Council’s (CPC) website. The calculator uses pricing formula data compiled in-house by Alberta Pork, based on U.S. Department of Agriculture (USDA) mandatory reporting, which is also the basis for Canadian prices. Further work is currently taking place to refine the accuracy of some metrics. In only the first three weeks following its launch, the calculator had been used more than 1,000 times by website visitors from across North America.

While red meat costs have surged, poultry and plant-based protein costs have decreased. At this Real Canadian Superstore in Edmonton, in mid-July, President’s Choice brand frozen ‘chickenless breasts’ were similar in price to boneless, skinless real chicken breasts, albeit seemingly less popular.

Based on data from Agriculture and Agri-Food Canada (AAFC), comparing 2019 and 2020, processors’ export profits were up 25 per cent, collectively earning those companies more than $440 million or $28 per pig extra over the previous year. Meanwhile, for retailers like Loblaws, both profits and costs grew as a result of COVID-19. In the first quarter of 2020, Loblaws generated $240 million of revenue, compared to $198 million during the same period in 2019.

Going forward, the CPC and its provincial members hope to continue working to develop new initiatives to highlight issues not only for industry stakeholders but the general public as well. Suffice to say, the processing and grocery businesses have been very lucrative in recent months.

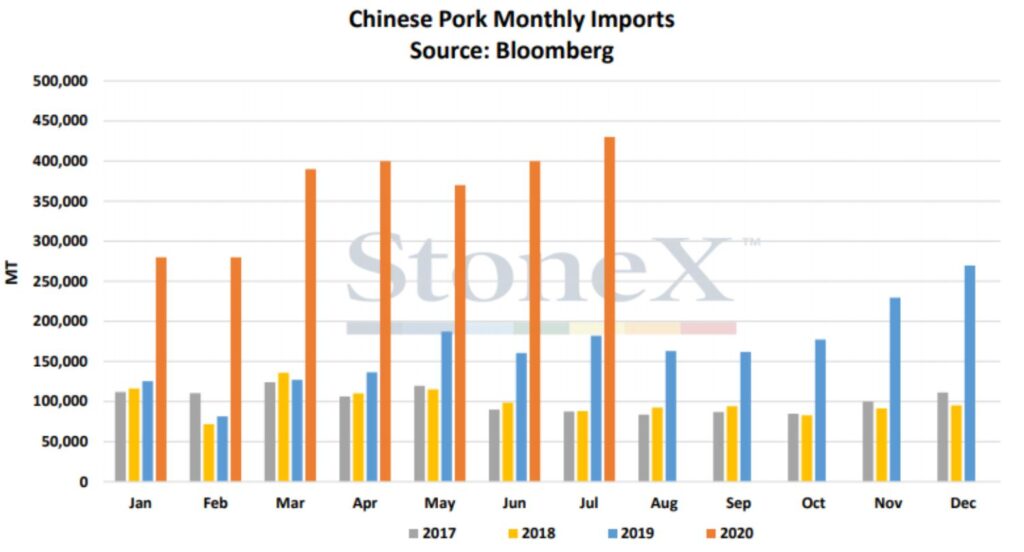

Typical summer pricing bump non-existent this year

In July 2020, China imported more than double the amount of pork as in July 2019, which itself was double the amount of pork imported in July 2018. Producers have not benefited from this incredible growth.

In most years, summer pig prices experience a boost due to increased domestic consumer demand, among other reasons. This year, while the increase in demand was palpable both domestically and internationally, prices for producers did not respond nearly as positively as they did for other supply chain partners.

In China, lingering issues like African Swine Fever (ASF) resulted in sky-rocketing meat prices for Chinese consumers – a phenomenon that was exploited to its full potential by all global pork players in the race to fill the enormous and growing Chinese protein gap.

Domestically, as locked-down Canadians started cooking at home more frequently compared to pre-COVID times, grocers raked in the profits, while restaurants and other food service providers generally suffered due to forced closures and public hesitation.

Various factors including North American meat plant temporary shutdowns helped drive up retail prices for pork and beef, to the tune of 30 per cent higher than this same period in 2019. To make matters worse, in August, Walmart and United Grocers – a national food procurement organization representing many major retailers – imposed new ‘supplier fees’ that are designed to breed competition and exclusivity when it comes to stocking products. As a result, the Canadian Federation of Agriculture (CFA), Food & Consumer Products of Canada (FCPC) and other organizations joined forces to raise concerns about the potential impact of the fees, which are considered arbitrary and unreasonable, threatening the affordability and security of Canada’s food supply.

In September, Walmart also eliminated its price-matching program, a long-time hallmark of the company’s commitment to keeping prices low for consumers. The move comes at a time when unemployment is at a decade high across Canada and has more than doubled in some provinces.

Government support still desired, albeit cynically

For most producers, consumer pricing surges either internationally or domestically were merely a slap in the face as margins remained submerged in a sea of red ink. These pricing woes have been met with a substantial non-response from the Government of Canada.

While the feds continue to insist that producer support is being effectively delivered, no meaningful publicly available data has demonstrated just how much money has actually reached producers’ pockets, and the government has given no indication that further comprehensive support is forthcoming any time soon, despite renewed calls from the Canadian Pork Council (CPC) to make adjustments to AgriStability’s payout levels. Given the long-term depressed pricing situation, it has come to a point where many producers have lost so much equity that any further losses are incapable of triggering an AgriStability payout.

On separate occasions earlier this year, the CPC had asked for the AgriStability reference margin to be increased from 70 to 85 per cent, along with a request for an ad hoc payment to producers at $20 per head – both of which were summarily rejected. As such, outgoing federal ag critic John Barlow did not mince words in expressing his disappointment with the efforts of Marie-Claude Bibeau, Minister, Agriculture and Agri-Food Canada:

“Minister Bibeau has to pound her fist on that cabinet table saying, ‘You know, enough is enough! Canadian agriculture needs attention – needs should be a priority, and we need to step up.’ That’s her job. Right now, I don’t think she has the clout at the cabinet table. If she did, we would see an assistance package already announced.”

Progress is slow and overdue but welcomed

In August, Alberta Pork publicly reported that a number of prominent commercial hog producers were actively undergoing a reduction in breeding stock at a minimum of 25 per cent of their herds, and, in some cases, as high as 50 per cent.

“If something doesn’t change dramatically, and soon, we’re going to see the coming year look like the last five,” said Andrew Dickson, General Manager, Manitoba Pork. “The industry is going to continue to integrate, which will result in independent producers becoming landlords – unable to afford their own operations and instead leasing barns to packers.”

As shared value discussions move forward, involving a greater number of producer and packer representatives, working collaboratively, the pricing situation will not be solved overnight. It will take a constant, concerted effort on the part of all stakeholders to drive meaningful change for the entire industry.

As we take a closer look at ourselves and where we want to be, consumers too are noticing us, often for unfortunate reasons. Especially since COVID-19, our less-glamorous side has been ripped open wide for all to see, while the positive work we do to secure Canada’s food supply has often been ignored.

For processors and retailers, it is likely easy to get wrapped up in playing public relations defense in these situations, and for producers, it is equally easy to get wrapped up in financially charged offense against value chain partners.

We all have a role to play in keeping this industry viable. For some, that objective may still seem very attainable, but for others, it is looking less so. Realistically, if any part of the value chain weakens to the point of breaking beyond repair, we are all going to be in trouble.

response")

U.S. Pork Cold Storage

Pork Commentary, October 26th, 2020

Jim Long, President-CEO, Genesus Inc.

At the end of September, Pork in U.S. Cold Storage was down 22% from a year ago, 466,674 vs. 598,750 (1,000 pounds). This is quite positive for markets going forward. Less Pork in storage means buyers have less to pull from.

Other Observations

Last week the U.S. marketed 2,679,000 hogs, a year ago 2,690,000. The USDA Hogs and Pigs Report September 1st indicated 10% more hogs year over year. Almost 2 months gone and the hogs have failed to show up. Just like June USDA report, wrong, wrong, wrong. We doubt if anyone is keeping the hogs as pets.

Hog Market weights are running similar or lower than a year ago. If hogs backed up, we would expect year over year heavier hogs.

If in mid-August we had said U.S. Pork Cut-Outs would be in the 90’s in late October, most would have said that was “insane”. Fact is there are. A huge reflection of overall domestic and export demand despite weekly hog marketing’s in the 2.7 million range. If we can get 90’s now with 2.7 million it’s hard to believe that prices won’t be higher when weekly numbers go to 2.4 – 2.5 million in 2021.

We understand China back in market for split carcasses. Some plants geared up. This is a result of Germany losing China – Asia as an export market due to ASF.

The hogs going to market now were born in April. In our opinion everything from April to September created a scenario to lower the sow herd and production. As weeks go on, we expect to see year over year weekly hog numbers decline. This will be price supportive.

U.S. sow slaughter in September was 276,120 last year 238,300. An increase of 28,000. Year to date 2,508,400 a year ago 2,235,220. An increase of over 273,000 year over year. If anyone doubts there has been significant breeding her liquidation, they should review the sow kill. Also, from all we can observe sow death rates of 12% are at record levels, gilt retention has been low, and next to no new sow barns being built. Put it all together. Less sows to produce pigs.

The Chicken Little Economist who said in mid-August that the U.S. would produce more hogs in 2021 than 2020 had no clue what he was talking about. You have to wonder if there are vested interests tied to futures trading that see it in their interest to bad mouth the prospects of prices and supply to the detriment of hog producers but to the benefit of Big City future trading sharpies.

We hear about the benefit of the futures market. The U.S. has the only hog future market in the world. What’s the benefit? Most of the time U.S. has the lowest hog prices in the world. As my late friend Doug Maus often said, “Chicago: Las Vegas casino with no rules.” “In the casino, the cardinal rule is to keep them playing and to keep them coming back. The longer they play, the more they lose, and in the end, we get it all.”

– Samuel “Ace” Rothstein_Casino movie –