Pork Commentary, August 16th, 2021 Jim Long, President-CEO, Genesus Inc.

The last few days we have read commentaries from pundits and future trading houses of big concern on pork demand. This is of course due to some of their vested interest to drive down lean hog futures. Doubt anyone of them has ever owned a hog or ever will.

We are glad to point out that last Friday, U.S. Pork cut-outs closed at $125.68. To us, the cut-outs reflect Pork demand here and now. If a year ago we wrote that Pork cut-outs would be $125.68 a year later it would have been called delusional (a year ago August lean hog futures 74.10). To us, Pork demand is currently solid and we see it continuing. Pox on the house of the vested interest’s intent on destroying better pricing for producers.

Hog slaughter continues to run well below USDA June 1 projections of 2% fewer hogs. Last week 6% less year over year, since first part of July slaughter close to -10%. Doubt anyone not shipping any market-ready hogs as we move into lower fall price market. We aren’t raising pets.

Hog Market in Europe

The hog market in Europe has its issues. High feed costs coupled with large volumes of Pork due to slow down in China Exports have decreased hog price in Spain, from a historic high in June of 1.55 Euro/kg liveweight (90¢ U.S. lb.) to 1.26 Euro/kg (68¢ U.S. lb.) last week. The Netherlands, in the same time frame, has gone from 1.21 Euro/kg liveweight (66¢ U.S. lb.) to 1.02 Euro/kg (55¢ U.S. lb.) last week. Danish 30 kg (66 lbs.) feeder pigs are 35 Euros ($42.64 U.S.)

Many producers will be losing money, with corn at 221 Euro a ton ($7.57 U.S. bushel) and imported soy meal 413 Euro a ton ($495 U.S. ton).

Currently, the Dutch government is paying for swine producers to leave the industry. We expect significant liquidation over the coming months in the Netherlands and Germany.

August Crop Report

USDA came out with its August Crop Report last week with big Corn acreage states of Iowa, Illinois, and Nebraska showing projected yield increases year over year. Of the top 10 producing, all are up in Corn and Soybean yields year over year other than Minnesota and South Dakota. Not sure why report was considered bullish when national projected average yield is second highest in history.

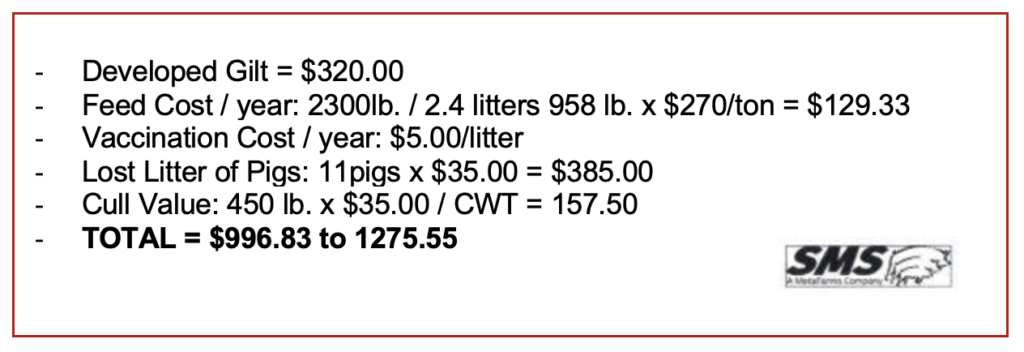

Cost of Sow Mortality

Last week we wrote about the cost estimation by Ron Ketchum, a founder of Swine Management Services, that a dead sow was $996 – $1275. Huge number and it’s a challenge for our industry. Quarter 2 2021 Meta Farms Database has average sow mortality 14.2%. We believe there is difference in swine genetics. Genesus average sow mortality in 2020 of all North American producers we have data was 4.36%. Big difference. As one competitor said, that isn’t a fair comparison because Genesus has better producers. Now that’s a comeback? Probably a certain Genetics Company should be less focused on going down the rabbit hole of GMO – Gene Editing and realize structure – temperament is a huge part of sow liveability. Dead sows cost big money as Mr. Ketchum calculates.

CFAP 1 Top-Up

Last week the Senators of Iowa and Minnesota sent a letter to Secretary of Agriculture Vilsack asking why CFAP 1 payments promised to swine producers had not been paid. This is good, we need to keep pressure on Senators, Congressmen, and Secretary Vilsack. The CFAP 1 top-up payments promised by Government have been paid to Dairy, Crop, and Cattle producers ($ billions). Why hasn’t the $17 per head promised been paid to swine producers? Are we second-class citizens, a second-class industry?

The CFAP payments were to compensate for damages producers of the food chain had incurred due to Covid. We kept producing as an industry, we had billions in losses. It is our right to be treated fairly as promised. Keep the pressure on, it works, do you think the Senators would have got engaged if weren’t reaching out? Keep contacting, it works.

Some have asked where is NPPC in all this. They are ones paid to represent our industry in Washington. Unfortunately, the Executives leadership of NPPC is wanting. It’s time for NPPC Directors to drain the swamp in Washington. We need new leadership that can get something done.

Below are some comments from our readers regarding CFAP 1 payments:

“I think the first question you should be asking yourselves is if the program said it was going to give out $11 or $13 per pig to the guys that actually own the pigs first, why didn’t we all get that? The people that actually pay you. If you look at the money allocated in that bill for swine was the lowest percentage-wise paid out of any other commodity.”

“Jim, thank you again for all you do, as an independent producer please stay on the CFAP trail. I too have been wondering what happened to it, grain guys have 6.50 corn and got 20.00 per acre.”

“Great write up Jim! Very refreshing to see someone preaching the truth to our producers, especially when it comes to the NPPC. Thanks for sending this out!”

“Jim, Thank you for keeping us informed on this. That top-off payment can most definitely help out! Appreciate your direction on this.”

“Appreciate your bringing this up. Don’t let it go. I’ve contacted my reps but no response so far. Don’t expect NPPC to step up – the CFAP payment cap penalizes their strongest supporters – mega-producers. NPPC has no incentive to go to bat for small/medium-sized producers which is who would benefit most from the additional CFAP 1 payment.”

“U speak the truth. Yes, beef and dairy both got well over a billion a piece in the last round and had their money 4 months ago. We had as good of a downtrodden scenario as anyone in Dec and Jan when this was put together. We should of gotten 1 billion-plus of the euthanization money we get now. What a wasted opportunity!!!!!!!”

Had one negative comment from an NPPC apologist and part of their bureaucracy:

“Why don’t you pick up the phone and call Neil instead of bashing him and NPPC? Complainers don’t accomplish very much. Why don’t you be a team player?”

Letter written to the USDA by a reader:

“USDA -VILSACK: As a small family hog farmers we are asking why the TOP-UP payments have been paid to cattle and grain farmers BUT not to hog farmers. Covid, plus the slow down of chain speeds which has not be challenged by the USDA has seen our contract with Hormel terminated next month. We have been with them in good standings for 12 years but the slowdown will affect 500,000 hogs they won’t buy. They also said their accident records have gone down NOT up like has been written.

Equality?Equity? Payment being held with no valid reasons. You’ve had 7 months now, step-up and support family hog producers!!! It is not playing well out here in the country. Period!”

Pork Commentary, August 9th, 2021 Jim Long, President-CEO, Genesus Inc.

Last week the U.S. marketed 2,327,000 market hogs, a year ago same week 2,559,000. That’s close to 10% less! In the last five weeks numbers have been close to 10% lower. Anyone keeping hogs because they think the price will go higher? We don’t think so, and weights holding at 277 – 278 lbs. over that time tells us we are keeping hogs moving.

Year to date U.S. total marketing’s 1.1% less than a year ago. Remember the Chicken Little Economists and followers who campaigned to tell us the U.S. was going to have more hogs in 2021 and the lean hog prices would not be profitable. These wise guys of course never owned hogs and never will. They had no clue how bad 2020 was for producers financially. As if losing $50 a head makes more hogs. The same “experts” work hand and hand with the NPPC executives that don’t seem to care why producers are not getting CFAP 1 top-ups promised by the government. Cattle and Grain producers got billions in the CFAP 1 top-ups. As if they were the only ones damaged by Covid debacle. The Washington-based NPPC crowd kept getting their big paycheques while accomplishing next to nothing for producers.

This past week NPPC big accomplishment, they applauded new measures on imported dogs that USDA put in place. How about CFAP 1 top-up? Let’s hope the swamp gets drained in Washington and NPPC directors can find new dynamic leadership.

Every producer needs to contact their Congressman and Senators. Ask where CFAP 1 top-up promised to hog producers is? Why haven’t we got it? Pork is an important part of America’s Food Chain and we need to be treated fairly.

Other Observations

US Pork Export to China

China bought 18,000 tonnes of Pork from USA last week. A significant purchase. Why does China need to buy Pork if they have lots?

Fewer Hogs Year Over Year

The 10% decrease in Market Hogs in the last few weeks, we believe, is a combination of liquidation, disease, and high temperatures. Financial losses last year devastated the industry, sow herds inventories were not maintained, we believe PRRS issues are hurting the industry big time.

Talked to a producer last week hit with PRRS. Expects 30% decline in weaned pigs over the next 12 months from previous year and a 20% increase in wean to finish mortality. That’s a 50% decline in market hogs.

Weights have held at 278 lbs. over the last few weeks, there is chance hogs backed up some due to the fact that weight didn’t drop lower.

We expect fewer hogs’ year over year for the next several months.

Cost of Sow Mortality

We have written about ever-increasing sow mortality in our industry, jumping 6% over the last few years to last year’s 13.9% average on PigCHAMP data system. Ron Ketchum, with Swine Management System, a well-known expert and founding partner of the database, recently spoke to the value of a dead sow. Mr. Ketchum estimates a range of $996 – $1275

At calculation midpoint, big economic difference, with our farmer’s math estimating every 1% change is 45¢ a pig. A 5% sow mortality change makes $2.25 a pig. We have talked to producers that used to have 7-8% sow mortality they now are pushing 20%. We have asked what changed? Barn? Penning? Density? Health? Answer was, nothing but sows don’t hold up and have prolapses that didn’t have before. Ask yourself same questions.

Huge economic cost to sow mortality. 5% change on a 2,500 sow unit is $135,000 a year, using a $40 sew price you need to produce an extra 3,375 pigs per year to cover the loss of 5% sows in a 2,500 sow unit.

If your sows prolapse, cripple, need toe clipping, poor sow salvage value, maybe you need different genetics. It’s your money.

When pigs fly: It is an expression used to cast doubt on unlikely circumstances, but with the help of Canadian airports, exports of agricultural commodities – including pork and live swine – are taking flight.

While most pork moves through the supply chain via truck and container ship, air freight is becoming an increasingly popular option for processors and exporters who can justify the cost, especially when it comes to delivering the highest-quality products to markets that are willing to pay.

Sky-high consumer demand drives profits

Using air freight means fresh Canadian pork reaches Chinese supermarket shelves within a day or two of passing through the Sunterra Meats plant in Trochu, Alberta.

Sunterra Meats of Trochu, Alberta – approximately 150 kilometres northeast of Calgary – has been sending fresh pork to select Asian destinations for several years, in addition to selling much of its product through Sunterra Markets locations in Alberta’s largest cities. Savvy overseas consumers are more than willing to pay a higher price for fresh Canadian pork loin, side ribs and belly, even compared to cheaper products more widely available in their home countries. As a prime example, in 2017, Costco Japan replaced its U.S. chilled pork products with Canadian pork, resulting in a 300-tonne monthly increase in sales. Associating Canadian pork with high quality has long been an important focus for the entire sector.

In 1986, Canada became one of the first countries to implement a national hog carcass classification system, employing electronic grading probe technology, which values carcasses based on objective measurements of both fat and muscle content. Sunterra regularly ships slice-ready primals with four-out-of-five muscle colour, fat colour and marbling criteria to high-end retailers in China and Japan, where finishing cuts are performed before the products is packaged using Sunterra-branded materials and labelled with the local retailer’s price tag.

Sunterra’s consumer-facing export products feature the Verified Canadian Pork (VCP) branding – a mark of distinction in Asian markets, as established in the Canadian Pork Council’s (CPC) independently developed Made-in-Canada Hog Price Report, which evaluated Canadian pork’s place in global markets. In Japan, pork of Canadian origin commands an observable premium over and above similar products of U.S. origin. The VCP program is backed by farmers’ quality assurance commitments through the Canadian Pork Excellence (CPE) program.

“A major difference between here and Asia is that they are more brand-conscious than us,” said Tony Martinez, former Vice President, Sales and Marketing, Sunterra Meats. “The brand represents the story, and they want to know that story. That’s important for our company.”

In June 2019, following a diplomatic dispute and consequent ban on Canadian pork exports to China, Sunterra’s shipments to the country came to a temporary halt.

“Pre-ban, we were sending three to four metric tonnes of product to China every week,” said Martinez. “Post-ban, we’ve been faced with some new challenges related to regulations and seal requirements.”

The challenge is related to the location where Canadian Food Inspection Agency (CFIA) seals are applied to the product. Previously, Sunterra was able to truck unsealed pallets to Edmonton International Airport (EIA), where they were then sealed and loaded onto an airplane. Now, per the CFIA’s Safe Food for Canadians Regulations, introduced in January 2019, each pallet must be sealed at a federally inspected processing facility by a CFIA inspector. The problem is the distance between the CFIA inspectors at EIA and Sunterra’s plant 200 kilometres southeast of the airport.

“It has become a bit impractical for larger loads,” said Martinez. “If we’re trying to send the same volume as we did before the change in regulations, now we need to individually seal and provide documentation for each pallet, which amounts to a lot of paperwork.”

And while paperwork is an administrative hassle at best, at worst, it can be the source of controversy. When China stopped imports of Canadian pork, it was under the pretext of inaccurate inspection certificates. This climate of concern leaves Martinez wondering if something similar could happen again.

“It makes us a bit paranoid, since it’s the kind of thing that could cause trouble. We already saw it happen once,” said Martinez.

As of July 2021, all food for export being transported on passenger or cargo flights must go through an enhanced security check, per Transport Canada requirements. This means products will need to be unloaded at the originating airport, X-rayed, physically opened up for inspection by CFIA, resealed, then reloaded before departure.

In June 2020, CFIA launched a pilot project to address the problem of sealing, working with stakeholders such as the Canadian Pork Council (CPC) and Canadian Meat Council (CMC). At that time, CFIA inspectors headed to EIA to oversee and re-apply the seal to 20 tonnes of chilled pork to China, as part of the test. The shipment, originating from Sunterra, arrived in China within days and was released to the importer in good condition. EIA provided support for the project and assisted Sunterra in obtaining and implementing the sealing equipment.

Despite regulatory concerns, Sunterra is confident that shipment volumes will eventually recover as they work with CFIA to smooth out any wrinkles in the system. For the markets served by the company, a steady stream of Canadian products not only satisfies a purchasing trend but also helps relieve a domestic industry that has been decimated by the effects of African Swine Fever (ASF) since August 2018, along with changes in consumer behaviour that have been spurred by the spread of COVID-19 since early 2020.

Breeding stock is uploaded to the cloud

For Fast Genetics, China is a popular destination for live swine. Animals are loaded onto crates and then lifted into cargo aircraft for efficient delivery to overseas clients.

From premium pork to breeding stock, companies far and wide across the value chain are making using of air travel when the margins make sense. Saskatoon-based Fast Genetics has moved animals by plane to locations like China in the past, mostly via airports in the U.S.

“For us, it’s about recognizing a need in a place like China, where the government is attempting rapid re-population,” said Sarah Heppner, Marketing Manager, Fast Genetics. “ASF has driven a shortage, and the government is trying desperately to rebuild production models; however, tensions between China and Canada have made exporting difficult at certain times.”

For Alliance Genetics Canada, a 15-year partnership with South Korea has resulted in pig movements to that country annually for several years. While COVID-19 delayed the company’s most recent shipment – which usually takes place early in the year – it was delivered, albeit later than desired, in November 2020. According to the company, the quality of its breeding stock is the main reason why business continues to flourish in spite of hurdles to global trade.

Meanwhile, for companies like PIC, destinations in Europe and South America are locations where pigs are desired. The company relies heavily on air transport to meet its business needs beyond North America. PIC raises its genetic improvement stock on nucleus farms in Saskatchewan and South Dakota, which are the source of live animals for export, especially boars and gilts, in addition to semen.

“Air shipments ensure our supply remains protected against the incurrence of disease,” said Tom Riek, North America Health Assurance Veterinarian, PIC. “The airplane offers a controlled environment, and the speed of transport helps mitigate health risks.”

One of PIC’s recent endeavours is a project that ships one or two full Boeing 747s every six to eight weeks out of EIA to a commercial producer in eastern Europe. Veterinary certificates and regulatory processes vary from one jurisdiction to another, and the relationships between Canada or the U.S. and those jurisdictions can impact decisions. It is also one of the reasons why PIC operates nucleus farms on both sides of the border.

“Export requirements for some countries are simple, while others are complex,” said Riek. “Our export coordination team is based in Tennessee, and they are responsible for scheduling the shipments.”

Navigating the intricacies of protocols is part of what Riek does alongside CFIA. Through CFIA, Riek and PIC are able to make the necessary arrangements to see the uninterrupted flow of products to foreign clients.

The reliability and quality of products delivered by air builds client confidence and keeps the venture profitable for PIC. The company ships ‘grandparent’ animals for clients to produce ‘parent’ stock, which will then be used to breed the first generation of animals sent to slaughter. The multiplication process amplifies the value of the grandparent animals, making them highly coveted.

Edmonton International’s reputation reaches for the stars

Airports like Edmonton International are increasingly looking to diversify their own portfolios and stimulate economic growth in the regions they serve.

While it was only Canada’s fifth-busiest airport in terms of annual passenger traffic prior to COVID-19, EIA is the country’s largest by physical area – a significant advantage over other major metropolitan airports when it comes to developing facilities to service cargo shipments.

“It’s part of our development strategy,” said Alex Lowe, Manager, Global Network Development (Cargo) Air Service and Business Development, EIA. “We know that air freight is not always number-one for exporters, but we are working on building strategic relationships to help Canadian businesses reach their full potential.”

EIA’s focus on moving products more than people is contrasted by some other Canadian international airports, including Calgary, but it comes down to what each location offers in terms of transportation logistics and priorities.

“Speed is the main advantage of air freight,” said Lowe. “It allows our clients to deliver products much quicker than other methods, and that speaks to a perceived value of freshness from farm to fork.”

With market-based struggles hampering Alberta’s oil and gas industry in recent years, moving agri-food products in particular has been a target for EIA. The disruption to passenger traffic, as a result of COVID-19, has also played into this consideration. Perhaps surprisingly, the airport handles not only commodities from western Canada but also items like cherries from Washington state – one of EIA’s proudest crowning achievements.

During peak cherry harvest, which is only a few weeks long in the summer, airports in Seattle and Vancouver quickly reach capacity, and fruit growers are left looking at the next best options: Los Angeles and Edmonton. While the distances between interior Washington and Los Angeles or Edmonton are comparable, factors such as traffic congestion and weather make the difference for exporters. Navigating the busy labyrinth of southern California can be a headache, and the state’s hot temperatures – while ideal for growing a wide variety of crops – create challenges for keeping product cool. For those reasons, the route from Washington to Alberta just makes more sense.

All major airports in Canada are publicly owned through the federal government. A lesser-known mandate for airports, aside from the obvious, is supporting economic development in the communities they serve. All told, while air freight is not usually the first thing that comes to mind when the transportation of pigs and pork is concerned, it can and does play an important role in facilitating movements and stimulating growth for the industry.

Keep your eye on the sky and feet on the ground

It is no longer the stuff of fantasy: pigs really do fly! And the entire pork value chain is better for it.

Success stories in the pork industry seem to be few and far between these days, but the use of air freight to move pork and live swine is a win for the modern Canadian pork value chain. More than providing a novel alternative to conventional transport, it signifies that the industry is stepping up to the plate to meet the needs of elite, emerging and evolving markets, where high quality wins over satisfied, paying customers. And that should sound good to just about anyone.

Next time you find yourself glancing up at a jetliner, consider that tens of thousands of feet overheard might be a shipment of premium meat raised on your farm or the genetics sector’s best and brightest candidates for populating foreign herds. Canada’s $24-billion annual swine industry depends on global partnerships, which are enhanced when trade routes are open and abundant.

Editor’s note: Carrie Selin is Manager of Taste Alberta, representing organizations within Alberta that have come together to encourage loyalty to local foods. She can be contacted at carrie.selin@tastealberta.ca.

By now, almost everyone in the Canadian agri-food industry has experienced some form of minor or major disruption to a meeting, conference or event that had been previously scheduled to take place in-person, prior to COVID-19.

With the easing of public health restrictions across the country, many people are breathing a little easier these days and looking forward to the continued interpersonal interactions that were missed in the past year or longer. Getting back to regularly planned activities, as before the pandemic, has become a priority for enhancing industry effectiveness and improving workplace pride and satisfaction.

Producer get-togethers stifled

Nearly 100 producers packed the main hall at the Coast Lethbridge Hotel & Conference Centre in southern Alberta during Alberta Pork’s semi-annual meeting, in March 2020. The next day, the province implemented COVID-19 gathering restrictions.

The Canadian agri-food value chain begins with producers, and COVID-19 has had a range of unexpected impacts on how business has been conducted. Sometimes, the impact was relatively minor, such as a few more phone calls or an exchange of emails instead of meeting for coffee. For others, the impact was a little more painful, forcing a change in habit from normal gathering settings to a completely virtual arrangement – something that even the most tech-savvy among us can struggle with.

“When COVID-19 restrictions were originally put into place in Alberta last year, it was the very day after our last face-to-face meeting with producers,” said Brent Moen, Chair, Alberta Pork. “Little did we know then it would take this long, but we are excited to get back to in-person meetings, hopefully within the coming months.”

The meeting referenced by Moen – one of four hosted by Alberta Pork across the province – touched on many hot-button issues that were burning then and are still smouldering today. Often, when it comes to addressing important business, something is lost when that process moves out of the hotel conference room and into the Zoom meeting room.

However, feedback from producers on subsequent virtual meetings – such as Alberta Pork’s annual general meeting (AGM) in November 2020 and following the round of semi-annual meetings in March 2021 – suggests that, while producers almost unanimously prefer in-person get-togethers, the virtual platform can be useful when needed. In lieu of an ability to gather in-person, remote meetings have been an adequate replacement and have even offered some benefit when it comes to limiting unnecessary travel and making those meetings more easily accessible to producers who struggle to balance their farm workload with taking time to attend a meeting in town.

The annual Banff Pork Seminar attracted nearly 800 guests in-person in 2020 and a similar number virtually in 2021.

More broadly, larger, internationally recognized events like the half-century-old Banff Pork Seminar were hit by restrictions in more ways than one. The Banff Pork Seminar is known as a premier event within the North American and global swine industry, attracting hundreds of attendees every year. However, in addition to the excellent programming offered, there is simply no way to digitally replicate the splendor of the Canadian Rockies. In 2020, the Banff Pork Seminar attracted upwards of 800 guests, which was matched in 2021, albeit with much less fanfare.

“We look forward to hopefully seeing everyone in-person in beautiful Banff for our delayed 50th anniversary celebration,” said Ashley Steeple, Conference Coordinator, Banff Pork Seminar. “The 2021 edition of the Seminar presented many challenges, and while we were able to climb over that hurdle in the end, we would much prefer a return to what everyone knows and loves!”

Originally, the Banff Pork Seminar organizing committee had considered extended opportunities as part of a 50th anniversary celebration, including a banquet, with a meal served by the legendary kitchen at the Fairmont Banff Springs Hotel. This celebration was wisely though grudgingly postponed, as attempting a virtual equivalent would have been a major injustice to fully appreciating the quality of the food at the Banff Springs, in addition to the life-long memories that are forged in that kind of intimate setting.

While the virtual world has presented us with many unique solutions to COVID-related problems, some things, such as celebrations, are too substantial to re-create.

Public engagement efforts transitioned

Edmonton’s ‘Bacon Day’ features the best food and beverage creations of Workshop Eatery’s Paul Shufelt, who loves to highlight local ingredients. In 2018, the event included a pig roast.

COVID-19’s impacts on food processing have been well-documented, but further down the value chain, the successful execution of food-related marketing activities has continued to bolster farming communities by encouraging support for Canadian-grown and -raised food.

In the past, consumer engagement opportunities have focused on extoling the virtues of high-quality Canadian food, with opportunities to meet a farmer or taste a local dish prepared by a talented chef. Events and festivals are an effective way to showcase where food comes from beyond the grocery store, but gathering limits have smothered some of the momentum like a wet blanket.

With that in mind, COVID-19 restrictions have meant that we need to find new ways for consumers to take in memorable experiences without being in direct contact with those offering the experiences, and this has taken shape in different ways.

“Like many other businesses in the province, we have been experimenting with solutions to continue serving our customers safely, creating the best possible experience in spite of conditions,” said Paul Shufelt, Chef & Proprietor, Workshop Eatery. “Some of those concepts have done better than others, and going forward, we are looking to leverage our lessons learned in a world that is embracing new ways of appreciating great food, during a pandemic or otherwise.”

Shufelt is a proud partner of Alberta Pork, having been involved in multiple events over the years celebrating all things piggy. In addition to his flagship restaurant, he operates two Woodshed Burgers locations in Edmonton, acts as an ambassador for the local culinary scene and has appeared on Food Network Canada’s “Fire Masters” as a contestant. Being on the cutting edge is in his nature, and like many other innovative food industry players, COVID-19 has allowed him to flex his creative muscles.

Rather than offering dining room service or hosting private functions, restaurants across the country have made the move to high-end takeout options, including full gourmet meals, along with newer concepts, such as cocktail packages. Cooking classes and demonstrations, usually reserved for public spots, have moved online, giving viewers a glimpse into processional kitchens without the hassles of finding physical space or needing to consider aspects of food safety in the service environment.

Porkapalooza welcomes BBQ competition teams from across western Canada and is the country’s largest certified BBQ event.

The Porkapalooza BBQ Festival is a world-class cooking competition, sanctioned by the Kansas City Barbeque Society (KCBS) – the world’s largest organization of barbeque and grilling enthusiasts. Historically, Porkapalooza has afforded groups like Taste Alberta and Alberta Pork the opportunity to collaborate and bring agri-food education to the masses. Since 2014, Porkapalooza has taken place annually in Edmonton, with the exception of 2020, when the event was stayed until May 2021, and then further moved to August 2021. In the early days of COVID-19, when it was uncertain whether restrictions would last two weeks, two months or two years, Porkapalooza’s path forward was unclear but ever-optimistic.

“We are incredibly eager to get back to hosting our competition for all the BBQ teams that invest their own time and money to take part,” said Mark Bosworth, Chair, Porkapalooza BBQ Festival Society. “Our event showcases some of the best food around, from some of the best cooks and pit masters you’ll find, which is a testament to the great work of everyone in the value chain – all the way back to the farmers who raise the products we are privileged to use.”

In 2021, Porkapalooza will look a little different, as this year’s competition is closed to the public – a difficult decision made earlier in the year, prior to the first postponement, out of an abundance of caution. In previous years, Porkapalooza came with a well-attended public festival component, including interactive tours of the cooking area, food stage demonstrations from local pros, plus plenty of family-friendly entertainment to ensure an enjoyable experience for everyone. While the festival’s valued guests will not be able to attend in-person this year, there are still plenty of opportunities to participate online, including prize contests and other event-related content shared through social media.

In years past, team attendance has pushed upwards of 50 cooking crews, mostly from Alberta and Saskatchewan, but also from as far away as British Columbia, Manitoba and Ontario. Given restrictions that were in place when the festival was first being organized, and on account of event logistics, Porkapalooza this year will host close to 30 BBQ teams to build excitement heading toward the 2022 event, which will hopefully inspire even more teams to participate, with public guests welcomed back.

Arriving at the ‘new normal’

During ‘National Takeout Day’ in mid-April, organized by Restaurants Canada, social media users posted pictures of their food from local establishments, including these pork and beef taco boxes from La Patrona in Sherwood Park – a suburb of Edmonton.

When it comes to telling the story of the Canadian agri-food value chain, the most authentic and resonating way to accomplish that goal is to place consumers directly into conversations with producers. And for producers, being aware and informed of industry issues around them is a necessary condition of being able to tell that story in a compelling and accurate way.

Natural opportunities to facilitate conversations between producers and consumers are presented with in-person events, generating widespread return-on-investment for the entire industry. Now more than ever, digital platforms have become critical to transmitting information, by using blogs and social media to promote content like photos and videos that try to capture a larger total experience and story.

With lockdowns and other restrictions in place to keep us safe, creating meaningful engagement has proven difficult. People have gradually become ‘Zoomed out’ with ‘COVID fatigue’ – the cultural symptom of a public health emergency, whether one falls ill or not. Most people today spend at least some of their working day behind a computer, and spending leisure time staring at a screen has become less appealing as time goes on.

If you were wary of the ‘new normal’ just as COVID-19 was starting to ramp up, the good news is that the bitter pill of change is getting somewhat easier to swallow, with the end of restrictions coming into view. As we all anticipate bigger and better things coming in the Canadian agri-food industry, COVID-19 has shown us new ways of flourishing under less-than-ideal circumstances.

Pork Commentary, August 3rd, 2021 Jim Long, President-CEO, Genesus Inc.

This past week U.S. slaughter numbers came in 210,000 head less than a year ago. The fourth week in a row that U.S. slaughter has been considerably lower year over year. This past week, down 9% year over year, in the month of July down close to the 9%.

The U.S.D.A. projected in the Hogs and Pigs Report an increase of 2% year over year in the 180 lb. plus and 120 lb. plus categories. Hog weights have not increased in July staying in the 278 lb. liveweight range. Appears to us U.S.D.A. June 1 Hogs and Pigs Report has overstated inventory which of course has hurt prices for producers.

What’s the saying about most fearful words in the English language? “We are here from the Government to help you.”

Other Observations

Packer-owned hogs which are significant numbers (Thursday, 163,000 per day) have dropped big time in weight the last few weeks; in May running in the 290s, last Thursday averaged 277.19 lbs. Tells us Packers need to pull their own hogs to keep plants running and meet commitments to supply retail, foodservice, and export agreements. We are heading into the fall with a market hog inventory very current.

Mexico

U.S. Pork Export Sales last week were 38,500 metric tonnes. A good number with Mexico leading the way up 28% year to date. Mexico last week bought 24,000 tonnes higher than any week ever bought by China.

Europe

Europe is expecting the economic effects of recent decreased pork exports to China. Feeder pigs of 30 kg. (66 lbs.) are currently selling for average price of about 250 DKK ($40 U.S.), well below cost of production.

In Spain, hog price has declined from a record 1.55 Eur/kg. (84ȼ lb.) on June 10 to 1.29 Eur/kg. (70ȼ lb.) July 29. Much of the decline is related to the decrease in China imports and lots of pork throughout Europe.

We expect to see sow herd liquidation to continue in parts of Europe as hog prices relative to feed prices are putting many producers below cost of production.

Why bellies are nearly double the price of loins?

You ever ask the question why bellies are nearly double the price of loins? Consumers vote with their money. Last Friday U.S. Pork Cut-out Bellies $2.22 lb., Loins $1.13 lb. Our bet, the reason Bellies (Bacon) has a better taste. It’s not because it’s leaner.

If Loins brought the same price as bellies, the overall carcass value would go up by about $50. Seems like real money and a good reason to figure out how to make better tasting loins. We need to stop chasing pennies on the alter of costs when there are dollars in the upside of better-tasting product. We need to stop thinking like farmers and more like marketers.

Consumers paying way more for Beef. Why? Taste! The money can be got in the market with a better product. It is already.

Good news for producers waiting to get rid of some old sows.

Big Sows 90ȼ lb. Never been a better time to sell old sows and buy some gilts and have money left over.

NPPC still missing in action on CFAP 1 top-up.

Grains and cattle got their top-up in billions of dollars. Where is NPPC? Executives too busy cashing their big fat paycheques. Why do they care it’s just the farmers?

Need new dynamic blood to drive NPPC forward, having twenty years of flat line per capita pork consumption is no sign of success. Any other group would have been gone long ago with such mediocre results. The worst of it, they spend the NPPC dollars to tell us how good they do. It’s a Washington elite mindset. Sometimes you must drain the swamp.

Last week readers contacted us about what to do on CFAP 1. We answered – Call your Senators and Congressman and demand the commitment of CFAP 1 top-up be honored.

Pork Commentary, July 26th, 2021 Jim Long, President-CEO, Genesus Inc

Some Observations:

Weighted Average National lean price stays strong at $1.07 a lb.

U.S. Pork cut-outs last Friday closed at $1.22 indicating strong demand.

Hog slaughter, surprise surprise, seems to be running lower than USDA projected, this past week about 240,000 head lower than a year ago (-10%).

Weights do not seem to be increasing despite significantly lower slaughter numbers in July. Running at 278 lbs., still down 5 lbs. from last year.

Cash early wean pigs at $40 are a reflection of lower supply and good demand. Last year at the same time were $8. The 5-year average this time is $20. Historically, cash early wean prices bottom in August, then begins to increase.

Cull sow price has jumped significantly to 90¢ lb. for heavy sows. Appears to be good demand for sausage products pushing up sow prices. Maybe sow slaughter slowed down but seems confusing as depops for PRRS continues. Maybe the continued increase in sow mortality (due to prolapses) and zero value sows is eroding ongoing sow cull supply. Dead sows and shot sows don’t go into pork supply.

African Swine Fever

Germany has had its first break of ASF involving commercial pigs. There have been over 1,000 instances in wild boars. The issue continues to impact German swine market by cutting export opportunities. German producers are receiving about $50 less than Spanish producers. There appears to be an ongoing reduction in Germany.

China reported 337.42 million hogs slaughtered in first six months of this year. Up 34.4% from the corresponding period a year earlier. The average weekly slaughter would have been 13 million head this year. The big question to us is, how much of the extra slaughter was light pigs or decreased slaughter weight?

Zhengbang, Muyuan, and Wens combined 5.6 million sows, according to World Mega Producer Report, announced they have dropped slaughter weights from 140 kg (310 lbs.) to 120 kg (264 lbs.) a decrease of 20 kg or 44 lbs. That’s about 3 weeks of growth. They probably dropped the weight due to high feed prices, ASF, and hog prices that have dropped significantly. If this was a trend over the whole industry that could have pulled ahead 40 million hogs?

Statistics we have seen had 18% of all hogs under 200 lbs. (90 kg) going to market in China. That too would have contributed to high slaughter in first half of year.

ASF is still a big challenge in China. One of the World Mega Producers recently announced they had lost 100,000 sows to ASF. Another one was aware of eliminated 80,000 sows. Another 30,000 sows farm lost 20,000. The truth, in the end, will be the market price. We expect an increase in China’s hog price will be coming in the next few weeks as supply drops from first half weekly numbers.

Where is CFAP 1 Payment?

NPPC seems to have no answer to the question “Where is CFAP 1 payment promise to Pig Producers?” Cattle got it; Crop Farmer got it? Pig Producers second-class citizens? Where is NPPC? Where are their wins? Why have they not asked producers to engage with Government, Senators, Congressmen? It’s a great time for change as the current Executives who can’t get it done are leaving. Great opportunity to clean house and get leadership that doesn’t believe pork per capita consumption that has flatlined for twenty years and has lost market share is Good! America wasn’t built on steady. The people who produce hogs every day deserve to get better results from executives pushing half a million a year in compensation. Good riddance, let’s hope the producers who are the directors of NPPC can find the right leaders to drive our industry forward. We have a great opportunity to grow our industry but we need leaders at NPPC that believe in going forward.

“I will go anywhere as long as it’s forward.” – David Livingston –

Pork Commentary, July 19th, 2021 Jim Long, President-CEO, Genesus Inc.

Last week we attended the National Pork Industry Conference (NPIC) in Wisconsin. About 900 attendees from the USA. A good cross-section of producers and industry. NPIC event was well organized and the Kalahari Resort did a good job with food and rooms.

What type of industry are we portraying?

Speakers from the NPIC did not address the status of further CFAP payments. Money was announced for euthanisation. The money announced falls far short of money (billions) already received by Cattle or Crops for the Coronavirus crisis. We continue to wonder about what the executives of National Pork Producers Council (NPPC) do for producers. They speak to issues but we have hard time seeing where they have wins for our industry. The good news, new executives are being hired, our hope for inspired leadership springs eternal.

Steve Meyer, Ag Economist, NPPC told us at the conference they take him to Washington to explain swine industry issues. Mr. Meyer, when he spoke at NPIC, showed a graph illustrating chicken and pork per capita consumption over the last twenty years. Chicken has almost doubled in consumption, pork stayed around 50 lbs. for the twenty years (flatlined). All things we already knew. What we found interesting is Mr. Meyer’s statement that it was probably good that pork had stayed at 50 lbs. for twenty years. He explained the merits of steady! Strange to us the logic that zero-growth per capita in pork is good. If that’s the story that’s taken to Washington by NPPC executives and surrogates, what type of industry are we portraying?

We believe if you aren’t moving forward you are retreating. America wasn’t built on steady. Americans are eating more total meat and poultry than any time in history. It’s reasonable, pork should aspire to be an ever-bigger piece of the protein pie. Let’s hope new leadership at NPPC can go on offense for the pork industry. We expect all would pitch in to grow our business.

PRRS 144 ripping through our industry

A big topic for every attendee at the conference was PRRS 144 ripping through our industry. Depopulations are ongoing as it appears hard to shut down. This is cutting pig production. Some farms at 40% pre-weaning mortality and another 40% in the nursery.

Further observations on record sow mortality and prolapse problems.

The Genetic company with the issue continues to blame nutrition, health etc. Some feed companies getting agitated for being blamed for what is a prolapse genetic issue.

Keeping a lid on expansion

From NPIC conversations, we believe few if any sow units or finisher barns will be built in 2021. The cost of building, high feed costs, labor issues, PRRS 144, etc. are all keeping a lid on any significant activity.

China

There was a Chinese speaker at NPIC, Jeffen Chen. His perspective was in line with the official numbers of China. Expansion and lots of pigs. There are lots of pigs but there might be some underlying issues. Let’s look at swine companies in China publicly traded. Below are some of the latest financial and production results.

First-half earnings forecast for public listed swine companies in 2021

Company

RMB million

U.S. Dollars million

Muyuan

9400-10200

1450-1571

Profit

Tecon

220-260

34-41

Profit

TRS

170-230

26-35

Profit

New Golden Dragon

30-40

5-6

Profit

ZhengHong Technology

90-100

14-15

Loss

Techbank

550-650

85-100

Loss

Zhengbang

1200-1450

185-223

Loss

Wens

2260-2560

348-394

Loss

New Hope

2950-3450

455-532

Loss

Pig Production Profit (RMB per head)

According to Xinmu.com, in 2022 Muyuan, Zhengbang, Techbank dropped their slaughter weights from 140 kg (308 lbs.) to 120 kg (264 lbs.) – a decrease of about 44 lbs. That’s a way to obviously pull hog numbers up short term.

If you study the different numbers it’s easy to see how China can be confusing. A range from one company to another of Big Profit to Big Loss. The spread is extraordinary. The other thing to consider, for much of the 6 months January – June, hog prices were all better than they are currently. We calculate that the average price Jan – June was 26.16 RMB kg ($1.83 U.S. liveweight) currently they are 15.90 RMB kg ($1.11 U.S. liveweight a lb.).

Point is things have got worse than these 6 months income statements reflect (a drop of $150 per head from average). The other 7 public swine companies are between Muyuan and New Hope; half showing profit, half showing losses. These are all public companies. We still expect China’s hog price has bottomed the loss from ASF in the third wave. We expect as China’s supply decreases from third wave prices will rebound.

Editor’s note: Steve Dziver is an agricultural commodity market analyst who owns and operates Commodity Professionals Inc., based in Winnipeg. He can be contacted at steve@commodityedge.ca.

Forward contracting is a bit like fortune telling, minus the crystal ball. Basis calculation is the difference between lean hog futures and a specific cash price.

Have you ever opened an email on forward contracting or checked hog prices from a packer’s publication and wondered, where did those prices come from? Or have you noticed a change in lean hog futures that did not match what happened in forward prices reported by a packer on the same day?

If so, you could probably benefit from an exploration of the mechanics used in creating forward contract prices for market hogs. While analyzing the market value and direction is the goal of forecasting, to understand how this is done, we must examine how Canadian forward contract prices are made in the first place.

Cash versus futures: today versus tomorrow

In simple terms, Canadian forward contract prices are calculated using a similar method as weekly cash, except that instead of using a specific regional cash price to start from, like the U.S. Department of Agriculture’s (USDA) LM_HG201 report, every forward contract price, regardless of packer or contract, must begin from the former Chicago Mercantile Exchange’s (now CME Group) lean hog futures. The lean hog futures then must be adjusted to represent the specific cash price of the region or packer, with characteristics such as ‘like terms’ of the cash price being used by a packer and also the correct ‘timing.’

Weekly Cash Calculation = USDA cash hog report [multiplied by] Packer Factor [multiplied by] Exchange Rate [equals] the price in Canadian dollars (CAD) per kilogram (kg)

The necessary adjustment shown above is known as ‘basis’ and can be defined as the difference between lean hog futures and a specific cash price. From that point, there are endless basis calculations that can be made on a given day, let alone per week. If, for example, there are 50 different cash prices that can be derived from all the USDA hog and pork reports, then, by default, there will be 50 basis numbers reported for that day.

Basis achieves two major adjustments: 1) altering lean hog futures to be like a specific cash price and 2) changing the value of the lean hog futures relative to when it is being used during the allotted coverage period.

There are only eight lean hog futures to cover 52 weeks, meaning some lean hog contracts are used to cover as many as eight or nine weeks in the year. To better understand lean hog futures, producers who use forward contracting programs should understand that lean hog futures of any trading month are the market’s best guess of cash on one day – the day that contract expires.

Because lean hog futures have a cash settlement, an expiring lean hog contract must match the two-day settlement CME lean hog index (LM_HG201) on the day of expiry. What that means is, as futures trade up and down throughout the course of a year, the contract value is based on a prediction of how the market will behave at that point, based on the information and historical trends at present.

For example, December 2021 lean hogs trade at a different value nearly every day and recently have been as high as U.S. dollars (USD) $89.55 per 100 pounds (cwt) on June 10 and as low as USD $74.12/cwt on June 24. Neither of those prices mean anything concrete, other than representing the market’s best guess of what cash is going to be on the day the December 2021 contract expires – somewhere around December 14.

Every closing price and every daily change between the day a contract starts trading to the day it expires is just a bunch of guesses. Opportunities arise when the market moves a contract much higher than where it eventually expires, giving producers a chance to hedge something better than cash.

Conversely, when the market moves the lean hog futures guess lower than what it will expire at, producers may find their returns to be worse than the cash value, meaning there is opportunity for packers to take advantage of lower carcass or cutout values, depending on how their contracts are formulated.

If you would like more information, Alberta Pork’s website (albertapork.com) includes further explanation on weekly cash calculations, according to individual packers’ contracts.

Basis trends come from historical observations

As anyone following the market would expect, there are trends in basis heading into expiry. Although the trends in futures may not be known, basis often follows patterns during certain times of the year. The easiest week to predict lean hog basis is during the week of expiry, as the market knows it must merge to near zero, which means that basis tightens. However, during all weeks before that – which could be as many as eight or nine weeks in the case of February, April, October and December (which all cover two months) – price adjustments can be significant.

Even if two cash prices use the same report but use different values from that report, the basis levels will be different. In the LM_HG217 report – which now summarizes multiple USDA cash regions, such as the LM_HG203 (National), the LM_HG206 (Iowa/Minnesota), the LM_HG212 (Western Cornbelt) and the LM_HG210 (Eastern Cornbelt) – each will potentially have a slightly different value, resulting in a slightly different basis when calculated against the CME futures.

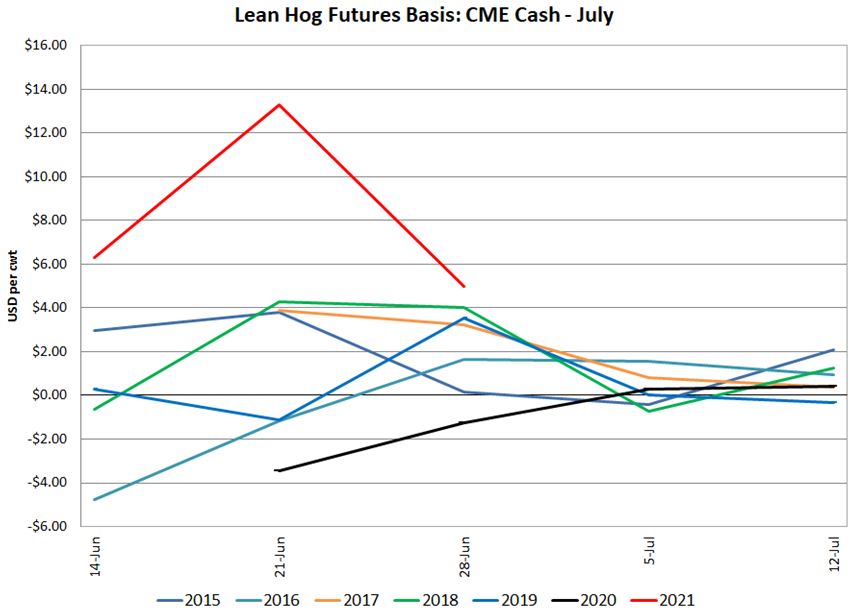

The LM_HG217 daily report provides a value for each independent market on a given day. In the following example, prices are for June 30, 2021. Since the second half of June and the first half of July rely on the July lean hog futures to provide price estimates, basis is calculated against the July lean hog futures using these cash values. The futures used for specific weeks will be explained further on.

The close of July lean hog futures on June 30, 2021 (the same day the cash values were reported) was USD $107.47/cwt. The daily basis for each of these three cash markets are, by default:

$113.02 [subtracted by] $107.47 [equals] $5.55 for the LM_HG203 report

$114.14 [subtracted by] $107.47 [equals] $6.54 for the LM_HG206 report

$114.42 [subtracted by] $107.47 [equals] $6.95 for the LM_HG212 report

Figure 1

Figure 1 is an example of weekly basis (LM_HG201 report) for the period of June 15 to July 15, measured against the July lean hog futures for the last five years. As is quite noticeable, this year, basis has been extremely positive, meaning cash was considerably higher than the July futures but is narrowing (or coming down, closer to zero, towards contract expiry).

The basis numbers reported in Figure 1 are sometimes referred to as inverted basis, because they are positive, meaning the cash market is higher than futures during this time. An inverted basis can indicate a downward-trending cash market, as futures are anticipating lower cash values when expiry is scheduled to occur. The easiest way to explain inverted basis is by looking at production weeks in late August and early September.

Cash markets in late August are typically coming off the summer highs, and when compared to October lean hog futures, cash is typically higher. Since August lean hog futures have expired, and October is the next contract to use, inverted basis values are almost always reported. Inverted basis does not necessarily represent a better marketing opportunity for producers, but rather, that cash value is higher than the comparable futures for that week. Depending on the fixed basis that a packer has applied to a specific marketing week, forward contracting could still be a better option to maximize returns.

If the basis calculation previously explained was completed five times – once for each day of the week – you would then have a weekly basis number for that specific week in 2021 for each of those cash-reported regions. There would then be the same calculation for 2020 using cash and futures for that year and in 2019, 2018 and so on. Weekly basis can be calculated in history for decades, as far back as futures and cash have been reported.

Basis is based on what?

Basis is the result of history. The market does not know what basis is, until it happens. Daily basis is known at the end of a trading day, and weekly basis is known at the end of a trading week. Since hogs are traditionally shipped weekly, and forward contract prices are offered weekly, most basis calculations are done weekly using a five-day average. As a result, there are 52 weekly basis values reported per cash price – one for every week of the year.

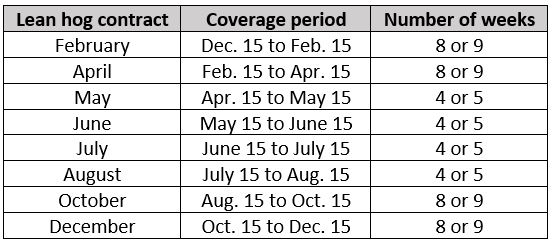

The weekly basis is then applied to a certain lean hog futures contract, making up the forward contracting price for that specific week. A different weekly basis would be applied to the next week but using the same lean hog futures to make up the forward contract price for the following week. That is why you do not commonly see forward contract prices the same for several weeks in a row; it is because packers have applied a different basis for each week. There are commonly reported weeks that have the same value, which means the packer has decided to use the same basis value over those two weeks. Figure 2 illustrates the usual period covered by each lean hog futures contract and the number of weeks it can be used.

Figure 2

The dates in Figure 2 are only estimates and can change from year to year. The reason a lean hog futures contract only covers to approximately the 15th day of the month is because every lean hog futures contract expires on the 10th trading day of the month. For example, July lean hogs will expire on the 10th trading day of July 2021, excluding holidays, which usually means around the 15th of the month. Once a contract expires, it no longer trades, and the next contract must be used to estimate the cash price for the next contract. That is why all contracts cover the second half of the previous expiry month, until the first half of their own expiry month.

Because basis is not known for the coming year, packers must now estimate what basis is going to be in the weeks ahead. Packer basis will usually use multi-year historical basis values – either three- or five-year averages – to predict where the basis could be in the year ahead, allowing them to then provide a fixed price, which producers can use to contract pig production.

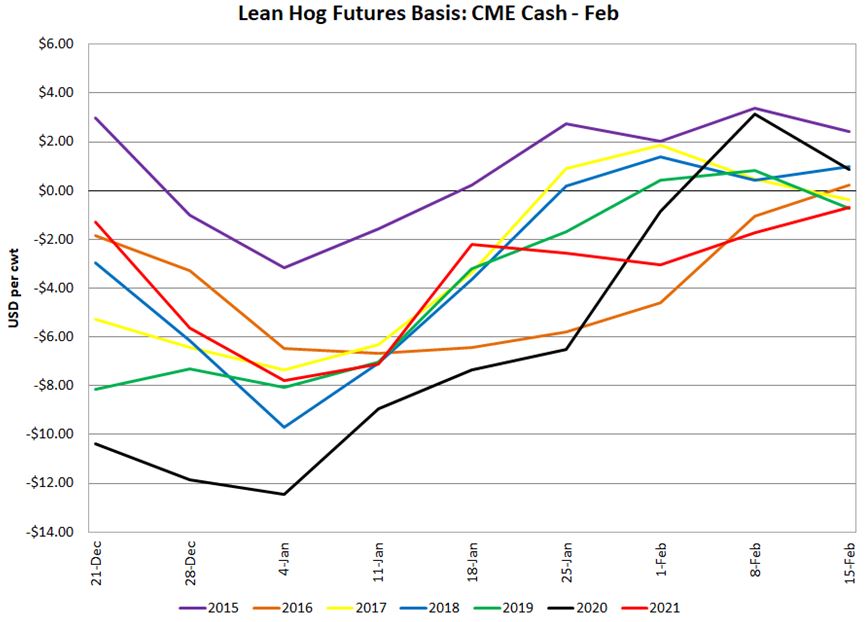

Basis is usually calculated as cash minus futures, so when the futures are higher than the cash, the basis becomes a negative number. In Figure 1, June cash happened to be higher than July futures, so basis was positive.

Figure 3

Figure 3 illustrates the opposite of Figure 1. Historical basis for the February lean hog futures against the CME cash (LM_HG201) is commonly negative. The reason for the negative basis is that a higher market is usually anticipated in the middle of February compared to the lower cash weeks of late December and the beginning of each calendar year. Negative basis simply implies cash is usually lower during a specific period (in this case, one week) compared to the next futures month. February lean hog futures cover eight or nine weeks of production, which begins before the contract expires (in this case, December). Similar to the inverted basis shown in the July contract in Figure 1, basis in both cases narrows toward zero at or near expiry.

Fixed forward contracting equals calculated risk

Once research is completed by a packer on historical basis, it allows them to make the appropriate adjustment to the futures, to offer a price to the producer who wants to contract. Packers will traditionally use a multi-year average with some protection to be certain that the price they have offered is in line with the adjustment that is expected for the weeks prior to expiry.

Packers do not always get basis correct, and in many cases, they have offered a price that was too high, or in other cases, too low compared to cash during that week. Lean hog futures trade up and down, which provides coverage to both the producer and the packer. There is little risk to either participant when considering futures alone; however, when considering basis, there is risk.

The basis risk lies entirely with the packer in the case of a fixed forward contracting price, because the packer is providing a price to the producer that will not change. A similar approach to setting basis and assuming basis risk applies to marketing agencies that provide fixed pricing forward contracts. For that reason, the risk of providing forward contracting is typically covered by taking a premium over basis to cover unforeseen results.

Producers who are using fixed forward contracting for price protection should have confidence that the prices they are receiving are based on historical average basis applied to ever-changing lean hog futures with some additional protection basis, which allows the administrator of the program to run and offer such contracts.

Editor’s note: Shawn Halter is Manager, Industry Development & Analysis at Sask Pork. He can be contacted at shalter@saskpork.com. Bijon Brown is the Production Economist for Alberta Pork. He can be contacted at bijon.brown@albertapork.com.

Pigs raised in frigid climates require shelter. Without additional heat, animal welfare suffers. The image of this barn near Shackleton, Saskatchewan – about 275 kilometres southwest of Saskatoon – is worth a thousand words.

Flash back to early February: the annual polar vortex had just descended upon the prairies, shrouding much of the landscape in a blanket of extremely cold air approaching wind chills of minus-50 degrees Celsius in some cases. Just the thought of those temperatures is enough to chill any person – or animal – to the bone.

Western Canada’s millions of hogs are thankfully able to brace for those potentially lethal temperatures by using barns, heated with energy sources derived from fossil fuels. Few, if any, other practical options exist, as alternative heating systems and non-petroleum fuels are virtually unobtainable, highly cost-prohibitive or simply ineffective.

Despite this overwhelming reality, the carbon tax has hammered at pork producer profitability for several years now. Just how much? Data from the prairie provinces is being evaluated to weigh the burden on hog farmers, while other sectors have been spared much of the pain. As carbon pricing in Canada seems to have become a political inevitability of late, its existence has raised the cost of doing business, and hog barn operators – without readily available alternatives at their disposal – are left footing the bill.

The Government of Canada’s price on carbon, in principle, is designed to encourage consumers to consider the environmental degradation caused by their day-to-day carbon emissions, resulting from gasoline and diesel for transportation, natural gas and coal for power generation and heating, or even propane for firing up barbecues.

The carbon tax is intended to reduce consumption and spur investment into alternative forms of energy. But how can petroleum product use go by the wayside when these products remain vital for survival in our climate and necessary for figuratively and literally ’putting food on the table?’ At the moment, it is unfeasible.

Mapping the on-farm carbon landscape

Comparing the natural gas and electricity usage levels for four types of hog operations

Twenty pork producers in Alberta and seven in Saskatchewan were recently surveyed to estimate the impact of the carbon tax on their farms. The survey asked producers with metered barns to share the usage for electricity and heating, along with any propane usage and the distance traveled to market hogs, during the 2020 calendar year.

While there are other sources of carbon emissions that can be linked to hog production – such as feed mill operations or off-farm feed purchases that require pick-up or delivery – and since hog market destinations differ from one farm to the next, only the fuel cost to transport hogs to market is captured in that part of the overall estimation.

In Alberta, usage varied greatly depending on the farm type. For example, farrow-to-finish operations used substantially more heating fuel than grow-to-finish, farrow-to-wean and nursery operations. On the other hand, farrow-to-wean operations used considerably more electricity than the other previously noted types.

Breaking down carbon tax costs for hog farmers

Carbon tax coefficients by product and cost per hog marketed over the coming decade

When comparing Alberta and Saskatchewan, separate coefficients are used for electricity, as the provinces’ electricity markets are different. Provincially owned SaskPower sources electricity from independent producers and then retails it to end-users, while the electricity market in Alberta consists of privately owned wholesale buyers (energy suppliers like ATCO, Enmax or Fortis) and producers of electricity interacting by bidding on the price and quantity of electricity each hour of the day. Where supply meets demand, the market clears, and the wholesale price of electricity is realized. Retailers then sell electricity to end-users, including farmers. This disparity between the provinces makes it difficult to track the carbon composition of electricity at any point in time, as successful sales to the grid may consist of electricity from fully renewable sources, fully fossil-fuel-generated sources or a blend of the two.

It is indicated from the estimates that the carbon tax on electricity in 2020 ranged between $0.19 and $0.48 per marketed hog. For natural gas, the carbon tax was between $0.38 and $0.47 per marketed hog. The carbon tax on propane was around $0.10, while the carbon tax on diesel for transport vehicles was between $0.04 and $0.12 per marketed hog.

Overall, the carbon tax for the survey respondents, on average, was between $0.79 and $1 last year. Based on data from Commodity Professionals Inc., it is estimated that producers in western Canada lost about $12 per hog in 2020, not including the carbon tax. Factoring in the carbon tax, that added expense served to drive another nail into the coffin of some operations, making them financial unviable, and even forcing some producers of varying size to go out of business.

In the coming decade, the price on carbon is expected to jump to $170 per tonne of CO2 equivalent. If consumption patterns remain the same, then the carbon cost would jump to between $4.50 and $5.62 per marketed hog. Placed in context of the most recent cost of production study conducted by Alberta Pork for the 2019 calendar year, heating, electricity and transportation costs amounted to $7.63 per marketed hog; this represented only five per cent of operating costs. Nevertheless, producers who volunteered their information for the cost of production study experienced an average loss of $5.30 per marketed hog.

In 2030, if everything else is held constant and carbon taxes amount to $5.62 per marketed hog, then losses would balloon to almost $11 per marketed hog. That may be a tough pill to swallow for some producers, especially when, over the past five years, they have experienced double-digit losses on most hogs marketed, only now beginning to recover as prices experience a summertime boost.

Clearly, a carbon tax is not in the interest of hog farmers, nor is the impact on the hog sector proportional to other agricultural commodities, which may have fared better over the same period and into the future.

Not all commodities are treated the same

Greenhouse operators in Canada are eligible for carbon tax exemptions, which has helped them remain competitive with international fruit and vegetable growers whose products also end up in Canadian grocery stores.

Canadian consumers value choice. Even in the dead of winter, product offerings at the retail level remain consistent, even if somewhat seasonal. This includes items like fresh produce, dry goods and meats that are imported from parts of the world with fairer climates or other production advantages.

Some carbon-intensive agricultural sectors in Canada are eligible to recuperate carbon tax expenses, but livestock producers have not yet been afforded the same luxury. In the Government of Canada’s 2021 budget, $100 million was set aside for producers to help offset rising costs due to the carbon tax. However, the details on which types of farms and activities qualify are still to be determined and can be expected this fall, according to the government.

On many farms, the current carbon tax increased costs and decreased farmers’ ability to be more productive and proactive by bringing more jobs to rural communities. On top of the current pain, this tax is set to increase five-fold over the next decade, exacerbating the problem.

When it comes to imported goods, such products are not subject to the same standard of taxation, despite the comparatively large carbon footprint associated with international trade. And because no carbon tax is levied against these imported products, Canadian farmers are invariably harmed in the process, while foreign exporters are not. Easily overlooked by the consumer, not so easily overcome by the domestic producer.

And, still, a much bigger question remains: how does any part of this situation promote lower carbon emissions? Essentially, for livestock producers, it does not.

While taxation appears to be a punitive measure against producers, some incentives do exist on the provincial level to encourage reduced fossil fuel consumption, such as carbon credits and other funding for projects that seek to reduce carbon intensity. Federally, a recent proposal to offer a credit-based program is also taking shape, but some farm groups, such as the Ontario Federation of Agriculture (OFA), worry that criteria for such a program may not recognize much of the progress that has already been made.

“Farmers have been doing a lot of good environmental work for a number of years. This didn’t just happen overnight,” said Drew Spoelstra, Vice President, OFA. “We’ve been doing things like following no-tilling and best management practices for a generation almost.”

Any solutions that may be forthcoming are desperately needed – and needed promptly – for the sustainability of many farm businesses and to defend food security for Canadians.

Political support could be on the horizon

In February 2020, Phillip Lawrence, Member of Parliament for Northumberland-Peterborough South (Ontario), introduced Bill C-206 in the House of Commons, an amendment to the Greenhouse Gas Pollution Pricing Act, which would extend the existing carbon tax exemption on farm gasoline and diesel to include natural gas and propane. The bill passed third reading and adoption in June 2021.

“Our farmers are struggling out there. They are now facing multiple blockades in addition to pricing instability and trade disruptions. The pressures on our farmers today are innumerable,” said Lawrence. “One of the things I heard when I was travelling my riding, from farmers and non-farmers, is that the carbon tax is impacting the way they operate their businesses. In fact, the carbon tax is taking away up to 12 per cent of their net income, so this is having a significant impact.”

Canada’s provincial and national pork producer organizations have previously called upon the Government of Canada to create a carbon tax exemption. Shortly following the introduction of Bill C-206, Rick Bergmann, Chair, Canadian Pork Council (CPC) sent a letter to Marie-Claude Bibeau, Minister, Agriculture and Agri-Food Canada (AAFC) urging her government’s support for such an exemption, citing economic impact studies generated by Manitoba Pork in 2019.

“To efficiently produce pork and manage the welfare of their animals, pork producers use natural gas or propane to heat their barns. There are no other practical alternatives,” the letter reads. “It is projected that, by 2022, fuel costs will increase by 150 per cent and cost pork producers $10 million per year. The carbon tax costs faced by producers cannot be recouped from the marketplace, as we face daily competition from American pork imports.”

In addition to alleviating the pain caused by the carbon tax, governments at all levels must consider their role in establishing the relevant legal framework to facilitate the development and expansion of infrastructure for the adoption of low- or no-carbon technologies. Such investment should also prioritize research and development of alternative energy, providing a clear pathway for making a smooth transition. Canada is a leader in innovation, but our privileged position depends on governments to play a large supporting role by attracting private investment, paving the way for economic growth.

Canadian power supply composition is changing, albeit slowly

Comparing power supply composition in Alberta, Saskatchewan and Ontario

If Canadians are permanently saddled with a price on carbon – which appears increasingly likely as time goes on – what kinds of solutions are available? Most directly and obviously, innovation in the area of power supply composition.

Canadian provinces have largely built their energy infrastructure around the natural resources available. This means that, with Niagara Falls in Ontario, hydroelectricity factors greatly in energy consumption, while in the prairie provinces, which are endowed with fossil fuels, carbon-emitting energy is featured disproportionately more.

There have been considerable strides to shift the carbon composition of electricity generation. In Saskatchewan, the composition of the electricity grid declined from 84 per cent coal and natural gas in 2018 to 72 per cent in 2020. In Alberta, the carbon-intensive share declined from 92 per cent in 2018 to 81 per cent in 2020.

There has been little change in the heating and transportation fuels over the same period. This may be partly due to infrastructural and regulatory policies that fail to facilitate meaningful change. Many farms have already made the transition from coal boilers for heating to natural gas and blended fuels with ethanol or biodiesel under policies that preceded carbon pricing.

One of the potentially viable alternatives that is becoming more and more popular is hydrogen. Hydrogen can be used for electricity, heating and as a transportation fuel. It can be produced using natural gas or renewable electricity. The major constraint to making considerable change is the lack of infrastructure support. In April 2021, the Edmonton region was identified as Canada’s first hydrogen hub. This new approach is expected to help to bring down the price of hydrogen by developing infrastructure to expand the use of hydrogen as fuel. While this recent shift away from fossil fuel over-reliance should be praised, it seems as if the cart was put before the horse. For any alternative to be fully useful, infrastructure must be widely developed and implemented prior to the use of carbon pricing as an incentive to transition to the cleaner alternative. Currently, pipeline and service station infrastructure are some of the greatest challenges to seeing hydrogen adopted in the mainstream.

Significant investment will no doubt be required to either bypass or replace existing natural gas infrastructure. In the U.K., as an example, the cost for getting all homes hydrogen-ready is estimated to be around £140 billion (or CAD $240 billion). Clearly, if the cost is so much to cover a land mass the size of the U.K., it may be significantly more for Canada. Such an investment would require both public and private partnerships, as well as clear transition targets. For instance, the U.K. is working towards having all boilers sold for home heating to be hydrogen-ready. Many home boilers currently operate on natural gas, but with changes to a few parts, by 2025, units can run entirely on hydrogen while costing no more than £100 (or CAD $170) to upgrade. Such a model sets a precedent for how to possibly handle a workable transition from natural gas to hydrogen.

In addition to power generation, the transportation industry must also be cast into the spotlight as the largest contributor, proportionally, to total carbon emissions. Within this industry, heavy-duty freight is the second-largest carbon emitting sector in the world, yet carbon-free alternatives are not scheduled to come online until after 2024. Furthermore, the cost of such trucks is predicted to be around USD $250,000 (or CAD $300,000), which would certainly be outside the range of affordability for most hog farmers in Canada.

Placing a price on carbon without providing clear leadership or opportunities to make the transition to alternatives effectively places a tax on productivity and creates a competitive disadvantage for Canadian hog farmers. Foreign suppliers in the pork sector and elsewhere in agri-food have recognized our impediment and exploited it, as a result.

The European Union (E.U.) will, by the end of 2021, institute a carbon border adjustment mechanism to address loss of competitiveness due to carbon pricing. The mechanism will adjust the price of all E.U. imports for the carbon emitted in its production process, thereby leveling the domestic playing field. Canada has yet to propose something similar, but such a mechanism is essential to have in place before carbon pricing. Unlike the E.U., the Government of Canada’s decision not to be prudent in this area will negatively impact Canadian production in our own domestic market.

However, Canada is a net exporter of many commodities, including hogs and pork. This means that, while something like a carbon border adjustment mechanism would strike a better balance between foreign and domestic products in Canada, it will do little to improve our standing in the international marketplace. That is bad news for pork producers. What is needed is a review of agreements like the Canada-United States-Mexico Agreement (CUSMA), Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) and the Comprehensive Economic and Trade Agreement (CETA) to ensure that any carbon border adjustment mechanism offers a fair deal for Canada in North American, European and Asian markets.

The future of fossil fuels in farming

This combined heat and power unit, installed at a farm near Bashaw, Alberta – about 150 kilometres southeast of Edmonton – is one example of Canadian pork sector energy innovation, but it comes with a large capital cost.

For fossil fuel alternatives to be taken seriously, no individual industry – and certainly not agriculture – should be singled out and demonized. Even the most die-hard environmental advocate likely does not hunt and forage for his or her own food, which almost definitely arrived through means that are reliant on fossil fuels.